PDF

PDF

DE = Debt to Equity Ratio

CCC = Climate Change Commitment

ROE = Return on Equity

ROA = Return on Assets

DY = Dividend Yield

FS = Firm Size

MCAP = Market Capitalisation

II = Institutional Investors

II*CCC = Interaction term for Institutional Investors and Climate Change Commitment

CR = Coverage Ratio

DR = Debt Ratio

i = Panel ID

t = time period

µ = Error term

4. RESULTS AND DISCUSSION

4.1. Descriptive Statistics

Table 2 shows descriptive statistics providing information about the variables’ central tendency, dispersion, and spread in the dataset Institutional ownership possesses a low mean (0.230 or 23%) and standard deviation (0.020 or 2%), reflecting uniformity in ownership percentages across companies. CCC possesses a mean of 0.789, reflecting that around 79% of companies report climate commitments. Financial ratios are highly variable. The debt-to-equity and interest coverage ratios have high standard deviations (312.95% and 484.46 times, respectively) and extreme maximum values, reflecting strong outliers and extensive variation in capital structures and interest payment ability. Market capitalisation is highly dispersed, indicating significant differences in firm size. Similarly, ROA and ROE vary extensively, with certain firms having significant losses. Dividend yield and firm size also indicate vast variability, suggesting the presence of a highly diversified sample of firms.

Table 2. Descriptive statistics.

| Variables | Obs | Mean | Std. Dev. | Min | Max |

| II (%) | 2,250 | 0.230 | 0.020 | 0.160 | 0.295 |

| CCC | 2,250 | 0.789 | 0.408 | 0.000 | 1.000 |

| DE (%) | 2,250 | 77.863 | 312.952 | 0.000 | 7753.330 |

| CR (Times) | 2,250 | 61.255 | 484.461 | -5848.560 | 9048.000 |

| DR (%) | 2,250 | 14.511 | 20.053 | -10.584 | 118.330 |

| MCAP ($billion) | 2,250 | 98,164 | 260,440 | -10,533 | 3,900,000 |

| ROA (%) | 2,250 | 6.485 | 8.713 | -88.240 | 49.180 |

| ROE (%) | 2,250 | 37.142 | 438.819 | -437.870 | 18555.200 |

| DY (Times) | 2,250 | 2.327 | 13.385 | 0.000 | 627.140 |

| FS | 2,250 | 9.349 | 3.375 | 1.018 | 15.203 |

4.2. Correlation Analysis

Table 3 below provides the correlation analysis between the variables. Institutional ownership has weak associations with every variable, meaning minimal direct correlation, although it positively correlates with the interest coverage ratio at 0.0315. CCC is negatively related to debt-to-equity ratio (-0.1020) and debt ratio (-0.2313), implying that companies committed to climate policies have lower leverage. It also exhibits a moderate negative correlation with company size (-0.2998), suggesting that smaller companies are likely to make climate commitments public. The debt-to-equity ratio is moderately positively correlated with the debt ratio (0.3493) and ROE (0.1458), suggesting that more leveraged companies can earn higher returns on equity but assume greater risk. Interest coverage ratio is positively correlated with ROA (0.1303), which indicates that successful companies find it less challenging to meet interest expenses. Market capitalisation is positively associated with firm size (0.2803) and ROA (0.2868), as more profitable firms tend to have higher market value. ROA and ROE have a positive association (0.1080), reflecting some stability in profitability measures.

Table 3. Correlation analysis.

| II | CCC | DE | CR | DR | MCAP | ROA | ROE | DY | FS | |

| II | 1 | |||||||||

| CCC | 0.011 | 1 | ||||||||

| DE | 0.020 | -0.102** | 1 | |||||||

| CR | 0.032 | 0.033 | -0.027 | 1 | ||||||

| DR | 0.019 | -0.231** | 0.349** | -0.077** | 1 | |||||

| MCAP | 0.017 | -0.206** | 0.062** | -0.002 | 0.157** | 1 | ||||

| ROA | 0.023 | -0.041** | 0.047** | 0.130** | 0.173** | 0.287** | 1 | |||

| ROE | 0.004 | -0.059** | 0.146** | 0.002 | 0.099** | 0.040 | 0.108** | 1 | ||

| DY | 0.022 | 0.029 | 0.015 | -0.001 | 0.011 | 0.005 | -0.018 | -0.002 | 1 | |

| FS | 0.027 | -0.300** | 0.131** | -0.064** | 0.306** | 0.280** | -0.058** | 0.021 | 0.021 | 1 |

Note: ** indicates significance at 5% level

4.3. Data Analysis

Table 4 below shows the variables’ normality. The Shapiro-Wilk test is used to evaluate the normality. It shows that the variables are not generally distributed except for the institutional investors, which indicates a normal distribution.

Table 4. Normality testing.

| Variables | Obs | W | V | Z |

| II | 2,250 | 0.999 | 0.775 | -0.650 |

| CCC | 2,250 | 0.998 | 2.534 | 2.375*** |

| DE | 2,250 | 0.193 | 1065.607 | 17.809*** |

| CR | 2,250 | 0.105 | 1181.376 | 18.073*** |

| DR | 2,250 | 0.759 | 318.757 | 14.726*** |

| ROA | 2,250 | 0.826 | 230.157 | 13.894*** |

| ROE | 2,250 | 0.034 | 1275.596 | 18.269*** |

| DY | 2,250 | 0.048 | 1256.378 | 18.230*** |

| FS | 2,250 | 0.860 | 184.361 | 13.327*** |

| MCAP | 2,250 | 0.837 | 214.802 | 13.718*** |

Note: ***: showing significance at 1%

Table 5 shows the analysis of the heteroscedasticity and autocorrelation for the models. The table confirms the presence of heteroscedasticity for all three models and autocorrelation for the debt and interest coverage ratios. It also affirms the absence of endogeneity issues in the dataset for any model.

Table 5. Diagnostic test.

| Model 1: Debt to Equity | Model 2: Debt Ratio | Model 3: Interest Coverage Ratio | |

| Heteroscedasticity | 2860000000*** | 40381767*** | 1280000000*** |

| Auto-correlation | 0.175 | 164.245*** | 9.297*** |

| Endogeneity | 2.099 | 2.322 | 2.119 |

Note: *** indicates significance at 1%, ** indicates significance at 5%, * indicates significance at 10%

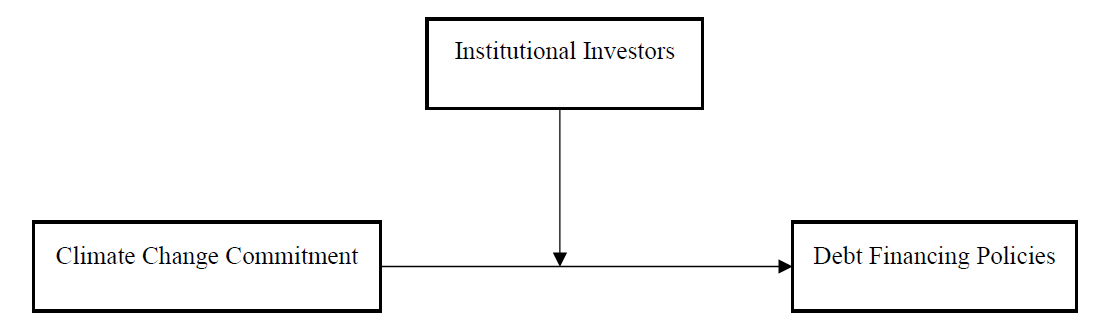

Table 6 shows the regression analysis. In Model 1, CCC has a strong positive influence on the debt-to-equity ratio (β = 59.681, p = 0.000), meaning that greater CCC is related to greater leverage. Model 2 indicates no significant effect on interest coverage (β = -0.983, p = 0.139), implying no substantial short-term liquidity consequence. Model 3 indicates that CCC is positively and significantly correlated with debt ratio (β = 14.287, p = 0.000). The findings show that CCC impacts the debt-to-equity and debt ratios significantly and positively. However, it does not have any significant impact on the interest coverage ratio. Overall, the findings indicate that CCC positively and significantly influences the debt financing policies. The findings of the study support the previous research findings. The study of (Lemma et al., 2021; and Palea & Drogo, 2020) have a positive and significant impact on debt financing. However, the study findings are negated by the study of (Zhao et al., 2024), which indicated a negative impact of CCC and debt financing. The difference in the findings is due to the consideration of the country, where Chinese firms have different climate commitments and are not as widely involved in these practices as firms from the S&P 500. In Model 1, institutional investors significantly moderate this influence (B = -262.397, p = 0.000), implying that institutional investor presence moderates the dependence on debt in more committed firms. For model 2, institutional investors do not have a significant and moderating impact on the interest coverage ratio (B = 1.098, P = 0.707). For model 3, institutional investors have a significant moderating impact (B = -62.754, P-value = 0.000) on the debt ratio. The study has established a significant moderating effect of institutional ownership on the relationship between CCC and debt financing. The empirical studies in this context have been limited. However, this empirical study confirms that the agency theory explains this moderating role. Agency theory underlines that institutional investors are effective monitors, aligning managerial behaviour with stakeholder interests. The empirical result underpins literature arguing that institutional investors increase the credibility of CCC by upholding transparency and risk management (Paseda & Okanya, 2020; Zhao et al., 2021). Their presence diminishes perceived credit risk, allowing for improved financing terms, hence filling the gap between environmental responsibility and financial strategy.

Table 6. Feasible GLS regression.

| Model 1: Debt to Equity | Model 2: Interest Coverage Ratio | Model 3: Debt Ratio | |

| Coefficient | Coefficient | Coefficient | |

| CCC | 59.681*** | -0.983 | 14.287*** |

| ROE | 0.051*** | 0.000 | 0.001*** |

| ROA | -0.126*** | 0.524*** | -0.002*** |

| DY | 0.036*** | 0.001 | 0.029*** |

| FS | -0.003 | -0.122*** | -0.018*** |

| MCAP | -0.013 | 0.462*** | 0.021*** |

| II | 262.002*** | -0.763 | 62.814*** |

| CCC*II | -262.397*** | 1.098 | -62.754*** |

| MCAP Group | |||

| Lower Mid-cap | -58.816*** | 1.726*** | -14.027*** |

| Mega-cap | -25.189*** | -1.203*** | 3.023*** |

| Upper Mid Cap | -58.385*** | 0.221 | -14.019*** |

| Small Cap | -58.821*** | 1.982*** | -14.166*** |

Abbreviations: CCC = Climate Change Commitment, ROE = Return on Equity, ROA = Return on Assets, DY = Dividend Yield, FS = Firm Size, MCAP = Market Capitalisation, II = Institutional Investors, CCC*II = Interaction Term of Climate Change Commitment and Institutional Investors.

Note: *** indicates significance at 1%, ** indicates significance at 5%, * indicates significance at 10%

Among control variables, ROE (β = 0.051, p = 0.000) and DY (β = 0.036, p = 0.000) are positive on leverage, whereas ROA is negative (β = -0.126, p = 0.000). All lower-mid, upper-mid, and small-cap companies have significantly lower debt-to-equity ratios than their large-cap counterparts. In Model 2, ROA is positively correlated (β = 0.524, p = 0.000), and FS and mega-cap status are inversely related to interest coverage. MCAP and DY are positively correlated with liquidity capacity. In Model 3, ROE, DY, and MCAP correlate positively with debt ratio, while ROA and FS correlate negatively. Smaller market cap groups uniformly have lower debt ratios than mega-cap companies. The findings indicate that while CCC is generally linked with higher leverage, institutional investors moderate this relationship. Control variables such as profitability, dividend policy and firm size also play a critical role in explaining debt structure variations across firms and market capitalisation tiers.

POLICY IMPLICATIONS

The results have significant implications for policymakers, firms, and investors. Regulatory authorities in the S&P 500 should promote or require climate-related disclosures, as CCC can impact financial decision-making, especially if backed by robust institutional controls. Raising the standards for transparency can enhance market discipline and investor confidence. Second, companies listed in the S&P 500 ought to appreciate the strategic importance of engaging institutional investors since their monitoring function increases the credibility of sustainability promises and can lead to better debt financing terms. Institutional investors also serve as a bridge between environmental accountability and financial sustainability, strengthening trust among creditors. Third, institutional investors that have invested in the S&P 500 can be designed to reward or incentivise them to include ESG considerations in their investment decisions, aligning all financial systems with sustainability objectives. Overall, the research endorses a more integrated policy approach where corporate finance and ESG commitments are not considered independently but as complementary factors for reaching long-term value and sustainability.

CONCLUSION AND RECOMMENDATIONS

This research aimed to explore the effect of CCC on S&P 500 companies’ debt policies and test the moderating influence of institutional ownership. Findings demonstrate that CCC tends to be linked with greater leverage, whereas institutional investors heavily moderate such a relationship by diminishing debt reliance in highly committed companies. Profitability, dividend policy, firm size, and market capitalisation also shape debt structures. These agency-theory-based findings underscore institutional investors as effective monitors, improving CCC credibility and reducing perceived credit risk. The implications of this study are two-fold: managers need to engage actively with institutional investors to improve governance and signal commitment to sustainability, and policymakers need to encourage mandatory climate disclosures and ESG integration into investment processes. Financial institutions need to include institutional ownership as a mitigating risk factor while evaluating the creditworthiness of climate-aware companies. Such harmonisation can enhance financing conditions and facilitate sustainable business strategies.

LIMITATIONS AND FUTURE DIRECTION

Although this research offers a helpful understanding of the role of institutional ownership in moderating the relationship between CCC and debt financing, it has certain limitations. For instance, employing a dummy variable as a proxy for CCC might simplify the complexity of climate policies and their intensity. Future research can implement more subtle measures, including climate performance scores or emission reduction targets. Second, the empirical analysis covers only a specific period and market situation, which could influence the applicability of the results across different nations or industries. Third, although the study controls for key financial factors, it does not explicitly address macroeconomic or policy factors that can influence both CCC and financing choices. Furthermore, research should investigate longitudinal designs to determine causal relationships over time and examine industry-specific dynamics. In addition, qualitative research might provide a richer understanding of how institutional investors shape sustainability practices beyond quantitative surveillance.

AUTHOR’S CONTRIBUTION

W.R. has contributed to conceptualisation, idea generation, problem statement, methodology, results analysis, results interpretation, writing – original draft.

CONSENT FOR PUBLICATION

Not applicable.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available at a reasonable request by contacting the corresponding author [W.R.].

FUNDING

None.

CONFLICT OF INTEREST

The authors declare that there is no conflict of interest regarding the publication of this article.

ACKNOWLEDGEMENTS

Declared none.