Article ID: PD2602201011

Views: 263The Influence of Financial Distress, Firm Life Cycle, and Capital Adequacy Ratio on Financial Performance with Non-Performing Loans as a Mediating Variable in Indonesian Banks

PDF

PDF

⬇ Downloads: 9

Financial distress can affect the ROI of different companies and reduce profitability and the efficiency of asset utilisation (Wu, Shao, et al., 2020). The reduction of financial distress, as explained by (Tan, 2012), enhances the profitability of firms in Turkey by increasing their financial performance and reducing regulatory uncertainty, which is detrimental to revenue. The decrease in ROA is attributable to increased financial distress, which, in turn, indicates declining efficiency in asset utilisation and profitability. (Zehri & Ben Mbarek, 2016) analyse the Asian banking sector and find that financial distress has a smaller effect on asset profitability in Islamic banks than in conventional banks, and that there is no significant correlation between the two variables under examination.

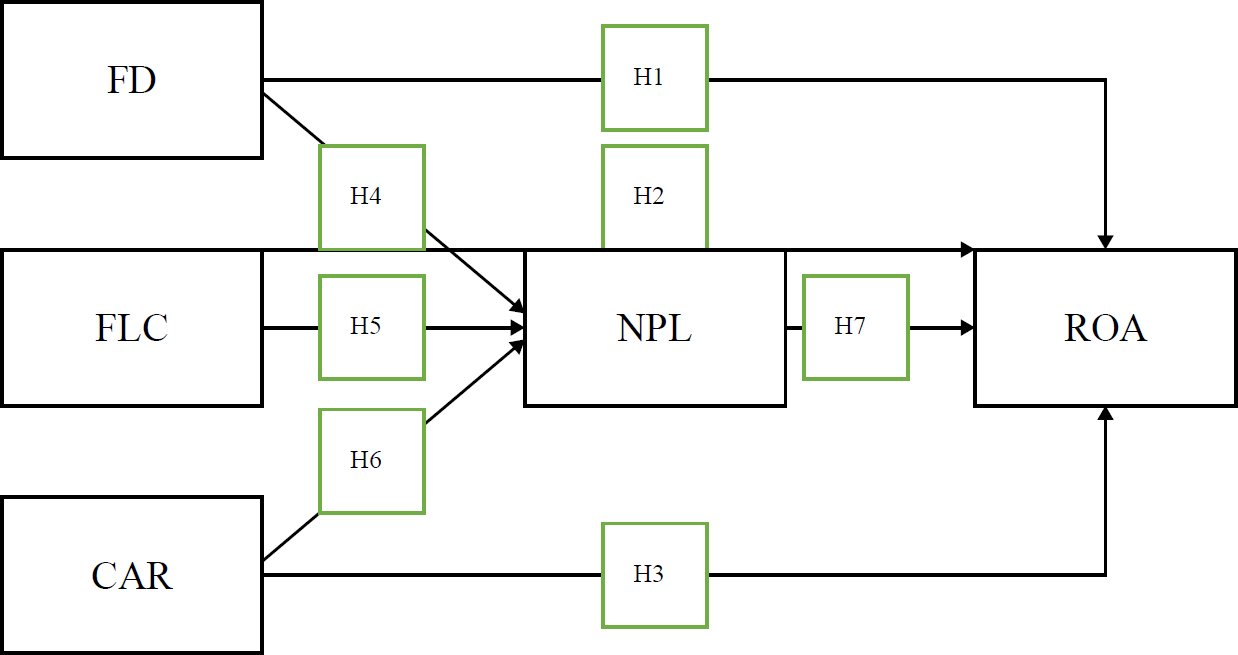

H1: ROA is negatively impacted by financial distress.

According to (Ahmed, 2020), the business life cycle does not allow for the strategic placement of corporate resources across its stages to promote investment efficiency. It has been found that companies in the growth and maturity stages exhibit greater investment efficiency and financial performance, with higher ROA, compared to other companies in the remaining stages. The relationship between RETA and ROA, especially at the maturity stage, is quite satisfactory because the companies have been able to use their assets to generate profits. Nevertheless, the connection between the life cycle and the firm’s financial performance is complex and involves many variables and factors, including firm size, risk management, and economic conditions (Haiyan et al., 2021; Khuong et al., 2022; Zhang & Xu, 2021). The impact of a company’s life cycle on its banking performance also depends on the stage of the life cycle the company is in, with the relationships to the growth, maturity, and decline stages differing (Ramzan & Lau, 2023).

H2: RETA, as a measure of Firm Life Cycle, positively impacts ROA during the maturity stage.

Banks with higher CAR values are considered more stable in the event of losses, as they have a stronger capital base that reduces their reliance on external financing (Dao & Nguyen, 2020). The empirical data show a strong positive correlation between CAR and bank profitability, such that higher CAR is associated with higher profitability (Nam et al., 2022; Wang et al., 2023). CAR positively influences the bank’s profitability.

H3: Capital adequacy ratio positively affects ROA.

Financial distress further increased banks’ rigidity in loan management; however, it also increased the costs associated with the recognition of credit losses, worsening the financial situation of the bank itself (Oliveira & Raposo, 2020). Financial distress is a sort of domino effect: the more banks are burdened with financial load, the greater the likelihood that the NPL ratio will increase. The rise in NPLs is more likely to affect the financial health of banks in a poorly operational state, ultimately undermining their stability and profitability. Their strong relationship is that, in periods of liquidity stress resulting from stress testing in financial markets, banks’ inability to address non-performing loans will be exacerbated (Arnould et al., 2017; Foglia, 2022).

H4: Financial distress is positively associated with NPLs.

The stage of the life cycles the bank is operating in affects NPLs, depending on the various practices for dealing with credit risk (Ahmed et al., 2020). The newer banks have been more aggressive in lending, thereby increasing the probability of NPLs. Conversely, older banks tend to be more conservative, and their risk management processes are more developed, which increases credit quality (Abu Amin et al., 2023; Campanella et al., 2020).

H5: There is a negative influence of the firm life cycle on NPLs.

Previous studies indicate that raising the Capital Adequacy Ratio (CAR) is a significant variable that can alleviate the risk of Non-Performing Loans (NPLs), thereby enhancing banks’ capacity to absorb losses and better manage prudential risk. Banks that are well-capitalised are more likely to survive credit shocks and asset quality shocks, as pointed out by (Buyuksalvarci & Abdioglu, 2011). However, it is stated that excessive capital buffers may reduce banks’ ability to lend and to make optimal use of assets, thereby decreasing profitability (Padmadisastra & Nurhayati, 2023). The results of this study indicate that it is important to balance capital management so that sufficient capitalisation will minimise credit risk without adversely affecting banks’ income-generating capacity. Consequently, according to the prudential banking theory, this paper introduces a negative correlation hypothesis between the Capital Adequacy Ratio and the Non-Performing Loans.

H6: There is a negative influence of CAR on NPLs.

High NPLs can negatively affect banks’ profitability, as measured by ROA, since they necessitate greater provisioning for poor credit recovery, ultimately undermining financial performance (Awaluddin et al., 2023; Jolevski, 2015; Wahyuni et al., 2023). The adverse effects of an increase in Non-Performing Loans (NPLs) on Return on Assets (ROA) include a decrease in interest revenue, an increase in loan loss coverage and a reduction in asset productivity. Consequently, banks with high NPL ratios will be less profitable.

H7: NPLs negatively impact ROA.

2. METHODOLOGY

This is a quantitative study that uses secondary data collected from Capital IQ and the official websites of the selected banks. The study sample comprises commercial banks listed on the Indonesia Stock Exchange, with a sample size of 37 banks. The sample is selected based on criteria, including full disclosure of financial data from 2010 to 2023 and disclosure of IT-related costs. The sampling method will ensure that data from complete and digitally active banks are selected, and this will be within the scope of the research analysis.

2.1. Variables and Measurements

Operationalization of each of the variables to be used in this study are mentioned in Table 1.

Table 1. Measurement of variables.

| Variables | Measurement | Source |

| ROA | (Wang et al., 2024) | |

| Financial distress = Probability Default | PD = N(−d2)

| (Blanco-Oliver, 2021; Manurung, 2023; Merton, 1974) |

| Firm life cycle = RETA | (Abu Amin et al., 2023; Habib & Hasan, 2019) | |

| CAR | | BI regulation No. 15/12/PBI/2013 |

| NPL | NPL Ratio | (Fell et al., 2021) |

Source: (Simatupang, 2024).

Using purposive sampling, 37 banks were selected for inclusion in this study, as presented in Table 2.

Table 2. Criteria for research samples.

| Commercial Banks Registered on the IDX | Bank |

| Without comprehensive financial reports spanning | (10) bank |

| Total Sample | 37 bank |

Source: (Simatupang, 2024).

3. RESULTS & ANALYSIS

This study uses panel data regression in establishing the impact of financial distress, life cycle, and the capital adequacy ratio on financial performance of banks in terms of Return on Assets (ROA). Non-performing loans (NPLs) serve as the basis for analysis. The sample includes a complete range of annual financial data for 2010-2023 for Indonesian commercial banks listed on the Indonesian Stock Exchange. In the present research, a three-step regression model, as described by Baron and Kenny, is used to examine the mediating effect of NPL and a formal test of mediation complements it:

The three steps given below provide a clear and concise view of Baron and Kenny’s approach to testing the mediation effect. There is a minor paraphrasing that is required, and it goes as follows:

Step 1: Direct Effect

Test the direct relationship of FD, RETA and CAR with the dependent variable (ROA).

Step 2: Effect on Mediator

Find out how independent variables (FD, RETA and CAR) influence the performance of the mediator (NPL)?

Step 3: Mediation Effect

The mediator (NPL) will influence the dependent variable (ROA), holding the independent variables (FD, RETA and CAR) constant.

These are the systematic steps; hence, they allow measurement of the NPL mediation role with respect to ROA and the independent variables. Through bootstrapping, we can identify the direct and indirect effects and confirm that NPL is a very important mediator among FD/RETA, CAR and ROA.

The analytical processes of the three alternative estimation models are compared (Table 3). As the entire models are employed in the analysis process, the approach to the study of the research is holistic and methodologically appropriate:

1. The Chow Test

Whether the Fixed Effects Model is superior to the Modelling of Common Effects.

2. The Hausman Test

The Hausman test is used to decide whether to use a fixed-effects model or a random-effects model. A low p-value (less than 0.05) means that the fixed effects model is more suitable and non-significant p-value means that the random effects model is the most suitable one.

3. Lagrange Multiplier (LM) Test

The LM test is used to compare the Random Effects Model with the Common Effects Model when the Chow and Hausman tests yield different model specifications. The Random Effects Model is adopted when the p-value is below 0.05. Otherwise, the Common Effects Model is held.

Table 3. Selection of the panel data model.

| Model Testing | P-Value | Comman Effect | Fixed Effect | Random Effect |

| ROA as the outcome variable | ||||

| Chow Test | 0.1941 | ✔️ | – | – |

| Hausman Test | 0.6752 | – | – | ✔️ |

| LM Test | 0.5492 | – | – | ✔️ |

| NPL as a dependent variable | ||||

| Chow Test | 0.0375 | – | ✔️ | – |

| Hausman Test | 0.0256 | – | ✔️ | – |

| LM Test | Given the Chow Test’s results indicating the inadequacy of the Common Effects Model (CEM), and having already applied the Hausman Test to choose between the Fixed Effects Model (FEM) and Random Effects Model (REM), further model selection is unnecessary | |||

Source: (Simatupang, 2024).

3.1. Empirical Models

Model 1: ROA_it = α + β1 PD_it + β2 RETA_it + β3 CAR_it + €_it

Model 2: NPL_it = α + β1 PD_it + β2 RETA_it + β3 CAR_it + €_it

Model 3: ROA_it = α + β1 PD_it + β2 RETA_it + β3 CAR_it + β4 NPL_it + €_it

The models facilitate indirect and direct effects to be estimated and test them statistically. Formal mediation analysis will also ensure that the role of NPL is assessed not by patterns of significance but by statistical numbers. They should also revisit the previous empirical findings to place the findings into context. Using the example of the fact that, even though the previous research (Akbar et al., 2022; Zehri & Ben Mbarek, 2016) proves the existence of the strong correlation between financial distress and ROA, this study adds a certain twist to the situation by considering the mediating effect played by NPL that the previous literature was largely deficient in. Similarly, the extent to which RETA reduces NPLs and drives profitability growth is consistent with the findings of (Ahmed, 2020), except that the combined effect is established through statistical testing rather than by assumption. The non-significant CAR/NPL observed draws attention to potential issues in the bivariate analysis and indicates that further analysis of banking performance research is warranted (Padmadisastra & Nurhayati, 2023). To capture the impact of the COVID-19 pandemic, a dummy variable was included, and panel unit root tests were conducted to ensure that the variables were in a stationary state, which is a requirement for effective regression analysis (Im et al., 2023).

4. DISCUSSION

4.1. Data Model Selection

The Hausman test and the Lagrange Multiplier test indicated that the Random Effects Model was the most suitable for Model 1, and the diagnostic tests confirmed that the classical assumptions were met. Model 2, however, was best estimated by the FEM, which passed the tests of classical assumptions, thereby justifying its applicability in any subsequent interpretation.

4.2. Regression Modeling

4.2.1. ROA as a Dependent Variable

The panel EGLS regression model that incorporated cross-sectional random effects showed statistically significant negative effects of both Non-Performing Loans (NPL) and Financial Distress (FD) on Return on Assets (ROA), with p-values of 0.00 (Table 4). These significant values at the 1% level indicate that increases in NPL and FD are correlated with reductions in the bank’s profitability. Conversely, the Retained Earnings to Total Assets (RETA) ratio showed a strong positive correlation with ROA, with a correlation coefficient of 6.08 and high statistical significance. In addition, the Capital Adequacy Ratio (CAR) was identified as positively affecting ROA, with a coefficient of 0.17 and a p-value of 0.00, indicating that a high capital position would positively affect a bank’s financial performance.

Table 4. Variable dependent ROA regression results.

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 2.557620 | 0.226457 | 11.29409 | 0.0000 |

| NPL | -0.187229 | 0.020218 | -9.260600 | 0.0000 |

| FD | -2.164520 | 0.393882 | -5.495346 | 0.0000 |

| RETA | 6.088149 | 0.520847 | 11.68894 | 0.0000 |

| CAR | 0.177633 | 0.047805 | 3.715771 | 0.0002 |

Source: (Simatupang, 2024).

4.2.2. NPL as a Dependent Variable

The regression analysis in Table 5 indicates a significant association between the profitability of the banks in terms of the ratio of returns on assets and non-performing loans, which implicates that the more profitable the bank is, the less likely it is to default. The financial distress and capital adequacy ratios seem not to have a direct influence on the loan performance. The model accounts for only a small share of the variation in non-performing loans, with the remainder attributable to external factors. Nevertheless, the general model is not statistically insignificant, and there is no autocorrelation in the residuals. Such findings highlight the importance of profitability in managing loan risk and indicate that further studies are needed to identify other major causes of non-performing loans.

Table 5. Variable dependent NPL regression results.

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 3.912879 | 0.333661 | 11.72710 | 0.0000 |

| FD_1 | 0.230980 | 0.281966 | 0.819175 | 0.4131 |

| RETA | -8.041112 | 1.085433 | -7.408206 | 0.0000 |

| CAR_2 | 0.329831 | 0.289057 | 1.141057 | 0.2544 |

Source: (Simatupang, 2024).

4.3. Causality Analysis

4.3.1. Direct And Indirect Effect Analysis

Financial distress negatively influences ROA, and RETA positively influences ROA, both directly and indirectly through NPL. Also, CAR positively and directly affects ROA by 0.18, and its indirect effect by negative NPLs (-0.06), such that the overall effect is lesser (0.16), showing that despite the high capital, which might lead to a higher profitability, the effect might be minimised unless good credit management is also present. All in all, RETA was the most influential on the ROA growth, whereas FD contributed the most to reducing ROA, both directly and indirectly (Table 6).

Table 6. Direct, indirect, and total effects.

| Independent Variable | Direct Effect on ROA | Influence on NPL as a Mediator | Indirect Effect on ROA via NPL | Total Effect on ROA |

| FD | -2.16452 | 0.23098 | 0.043246 | -2.12127 |

| RETA | 0.688149 | -8.04111 | 1.505529 | 2.193678 |

| CAR | 0.177633 | 0.329831 | -0.06175 | 0.115879 |

Source: (Simatupang, 2024).

H1: Financial Distress negatively impacts ROA.

The findings show that financial distress has a significant negative impact on return on assets (ROA), as indicated by the coefficient (-2.16) and a probability of 0.00. This shows that Return on Assets (ROA) is very sensitive to the intensity of the financial distress. Financial distress refers to the condition that a company, such as a bank, is unable to meet its payments. This may be because profits have declined, debt has been accumulating, or it is suffering from a lack of liquidity. This situation may reduce a bank’s efficiency and profitability in the effective management of its assets (Shaukat & Affandi, 2015; Akbar et al., 2022; Zehri & Ben Mbarek, 2016). The financial distress affects both Islamic and traditional banks similarly in terms of their ROA, according to the data.

H2: The Firm Life Cycle has a positive impact on ROA.

The Retained Earnings to Total Assets (RETA) ratio of the company is highly sensitive to asset returns, depending on the company’s life stage (Muharam & Bandung, 2024). (Haiyan et al., 2021; Wang et al., 2020). As recent empirical studies have shown, financial performance is positively associated with higher retention of earnings. It is evident from the literature in this study that a company should depend on its life cycle stage to determine its Return on Assets (ROA). The findings are consistent with the available findings. The relationship between asset management and the revenue-generating capacity of companies at various stages in their life cycle is subject to the ROA of the same. First, the returns in companies are usually reduced by high investment and risk.

H3: CAR influences Return on Assets (ROA).

Regression analysis indicates a positive correlation between ROI and the Capital Adequacy Ratio (CAR). The coefficient (0.18) and the p-value (0.00) imply that the capital increase directly contributes to an increase in the profits of a bank. With sufficient capital, banks can respond to financial shocks, manage risks more effectively and lend more confidently (Nam et al., 2022; Wang et al., 2023). Financial strength also enables banks to be more flexible in how they conduct business and to earn more because they can make greater use of their assets. Research supporting this has consistently indicated that banks with high levels of capital are more likely to remain profitable in the long run and to meet new risks (Petria et al., 2015). A larger CAR, however, indicates that a company is more stable. Nonetheless, excess capital may also impede growth opportunities, which could be detrimental to profits if it fails to align with a sound risk-return strategy (Sharkas & Al-Sharkas, 2022; Al Mamun et al., 2022; Mir & Shah, 2022). Thus, the impact of CAR on ROA is determined by the fit of a given bank’s capital management with its other activities and investments.

H4: Financial distress has a positive influence on NPLs.

The probability of default Financial Distress (FD) does not have a significant effect on NPLs, as evidenced by the regression comparison between CF and NPS. The result contradicts the claim that FD does not significantly affect NPLs. This research refutes the traditional belief that financial hardship leads to loan defaults (Irwanto et al., 2024; Nufus et al., 2018; Wilevy & Kurniasih, 2021).

H5: The firm life cycle has a negative influence on NPLs.

The findings also suggest that Retained Earnings to Total Assets (RETA) affects Non-Performing Loans (NPLs) across various stages of the firm’s life cycle. According to (Abuhommous, 2023), older banks are less prone to credit risk than new banks because they have higher retained earnings, which help them increase internal financing capacity and improve their credit risk management.

H6: CAR has a negative influence on NPLs.

The regression indicates that the influence of Non-Performing Loans (NPLs) on the Capital Adequacy Ratio (CAR) is not significant, suggesting that other factors, such as credit risk management, macroeconomic conditions, or loan portfolio quality, may be more important.

H7: There is a negative influence of NPLs on ROA.

The management of credit risk is a significant source of profits for a bank, as research has shown that the exploitation of bad loans (NPLs) drastically reduces banks’ profitability, as indicated by Return on Assets (ROA).