Article ID: PD2602201009

Views: 240AI and Automation and Hassle-Free Bookkeeping: Testing Mediating Effect of User Acceptance and Moderating Impact of Digital Trust in the UK SME Retail and Service Sectors

PDF

PDF

⬇ Downloads: 9

1Department of Business Administration, Jubail Industrial College, Jubail, Kingdom of Saudi Arabia

Received: 27 March, 2026

Accepted: 29 June, 2026

Revised: 08 June, 2026

Published: 10 July, 2026

Abstract:

Introduction: This study examined the impact of artificial intelligence (AI) and automation on hassle-free bookkeeping among small and medium-sized enterprises (SMEs) in the UK retail and service industries. User acceptance was a mediating variable, and digital trust was a moderating variable based on a Technology Acceptance Model (TAM)-inspired model.

Methodology: The study adopted quantitative cross-sectional research design and data was collected through online questionnaire from the owners and employees of SMEs engaged in financial and operational activities. The data of 410 respondents were then analysed in SmartPLS, 4.1 using Partial Least Squares Structural Equation Modelling (PLS-SEM). Demographic analysis, measurement models including discriminant validity, path analysis, and model explanatory power using R-squared were used to test the study hypotheses.

Results: The findings show there is a positive and significant effect of AI and automation on hassle-free bookkeeping (β = 0.386, t = 6.347, p = 0.001). Additionally, the indirect influence of AI and automation on hassle-free bookkeeping had an indirect impact, mediated by user acceptance (β = 0.117, p < 0.05), which means that user acceptance partially mediated the relationship. Moreover, AI and automation and user acceptance were also moderated by digital trust (β = 0.117, t = 2.060 p = 0.040), meaning that high digital trust would lead to high acceptance.

Conclusion: The research has practical implications to UK SMEs and policymakers as it recommends the importance of trust-building, training based on user considerations, and facilitative policies on digitalisation in enhancing the adoption of AI-based bookkeeping.

Keywords: Hassle-free bookkeeping, AI and automation, user acceptance, digital trust, retail and service sector, UK.

1. INTRODUCTION

In every industry, Artificial Intelligence (AI) and automation are transforming the way business activities are performed, drastically changing conventional work processes. AI is a term used to describe a subfield of computer science that uses advanced analytical and logic-informed solutions, including machine learning, to process events, make automated decisions, and act in ways that historically necessitated an act of human intelligence (Stryker & Kavlakoglu, 2024). Automation is the application of technology to carry out pre-set, rule-based operations with minimal human interaction, thereby minimising repetitive human workload (Restrepo, 2024). These technologies have grown exponentially over the last ten years and have been applied in business functions such as accounting and finance.

For the AI market, it is predicted that it can grow exponentially as corporations persist with digital transformation plans and is projected to reach up to $4.8 trillion across the globe by 2033 (UN Trade and Development, 2025). Moreover, the accounting AI market is projected to be $50.29 billion by 2030, with automated bookkeeping software contributing to most of these increments (Prarthanna & Vadivel, 2025). AI and automation tools can be used to significantly streamline complicated business operations and increase operational efficiency in both the service and retail sectors by making it possible to handle real-time data processing, reduce errors, predictively insightful, and intelligent to perform various tasks (Dalsaniya & Patel, 2022; Kitsantas et al., 2024). Moreover, a synthesis of various industry reports revealed that AI-based automation can reduce 90% of manual data entry errors and speed up the transaction process by 50% in accounting (Eziefule, 2022). Taken together, these trends highlight the revolutionary role of AI and automation in contemporary business activities and the technological context of examining their effects on bookkeeping practices.

Theoretically, to comprehend the impact of AI and automation on bookkeeping results, it is necessary to base studies on technology acceptance and user behaviour models. The Technology Acceptance Model (TAM) assumes that perceptions of usefulness and perceived ease of use affect users’ attitudes toward technology which in turn impacts their intentions and actual adoption habits (Mogaji et al., 2024). Within TAM, trust in technology and acceptance of the person are organisational and individual factors that determine whether technological innovations are adopted and put into effective use. Furthermore, similar dynamics have been studied in other countries through empirical research. As an illustration, a study on the retail industry investigated the impact of AI technologies on the productivity of firms in online stores and found that the adoption of AI had a significant effect on sales conversion and operational efficiency due to the decrease in friction in online processes (Fang et al., 2025). Similarly, empirical research in service-based small enterprises has shown that the automation of routine administrative operations can enhance operational efficiency and decision-making capacity, although it is not based in the UK (Peláez & Álvarez, 2025). These external results suggest preliminary evidence that AI and automation can influence bookkeeping performance and show that studies need to be localised to consider specific socioeconomic and regulatory factors.

Small and medium-sized enterprises (SMEs) are the core of the UK economy, as they represent more than 99.8% of the total number of businesses in the country, which is imperative to the national economic performance and employment (GOV.UK, 2025). Although these companies are economically significant, they usually face manual and time-consuming challenges, especially in administrative areas such as bookkeeping and financial reporting (Brooks, 2023). Manual bookkeeping systems are labour-intensive, subject to human error, and distract management focus on the main entrepreneurial operations, which form operational bottlenecks and have the potential to restrict growth and competitiveness (Stevens, 2024). The adoption of technology in UK SMEs is not evenly distributed, with a significant number of SMEs still lacking the use of basic digital tools and well-organised plans to implement advanced technologies in their operations. The main obstacles are inaccessibility to finance to invest in technology, inadequate technical capabilities of small teams, and scepticism about the gains of digital innovation (GOV.UK, 2025). These restrictions do not just reduce the productivity but also increase the digital divide between companies who are technologically ready, and those who are trailing behind. Thus, the presence of large barriers to technological change and resource constraints characterizes the SME environment, given the potential of technological change is immense.

Therefore, the research aims to examine the role of AI and automation in supporting hassle-free bookkeeping in SMEs, in the UK retail and service industry, the mediating role of user acceptance, and the moderating role of digital trust. The current research adds to the theory by developing a TAM-inspired model within the SME environment, which is characterized by scarce resources and the variability of technological readiness. Methodologically, it pays attention to research gaps existing in the existing literature through introducing some insidious constructs, including digital trust, that demonstrate how much users are confident in the accuracy of technology, data safety, and ethical processing of financial data as a component of the acceptance and use model. In practice, the study is useful to SME owners, technology providers, and policymakers who would wish to make businesses more resilient, efficient in managing their bookkeeping operations, and use more digital in the future.

This paper gives a thorough description of the theoretical framework underpinning this study in the latter sections, followed by the generation of hypotheses based on the existing literature. The methodology section provides every step that has been taken to complete this study. The results and discussion are presented in the designated sections, followed by the conclusion, addressing the key findings, future directions, and limitations of this study.

2. LITERATURE REVIEW

2.1. Theoretical Framework

In this study, the theoretical approach used was TAM. TAM was initially theorised by Davis, and it describes the ways users become acquainted with and adopt new technologies, where the behavioural intention toward technology adoption is determined by perceived usefulness (PU) and perceived ease of use (PEOU) (Mogaji et al., 2024). Here, PU is having belief in a system that it improves job performance and makes a person or work better or more efficient, whereas PEOU is the belief that the system is effortless such as it is easy to learn and understand. User acceptance is dependent on these constructs, hence affecting actual use.

Empirical research has recently been applied to assess elements such as technology adoption in the SME context across industries. To illustrate this, a survey on sustainable technology adoption of SMEs in service (beauty, health, and wellness) industries found PEOU and social influence to be significant predictors of technology adoption, which endorses the relevance of TAM in service-based small firms (Qing et al., 2025). Likewise, a Lebanese study examined the long-term TAM in the adoption of accounting information systems (AIS) by SMEs (Dallal & Sankari, 2025). PEU, trust, and security were found to positively influence the acceptance and use of AIS, indicating that TAM can be used in financial technology applications in bookkeeping activities. Furthermore, the TAMs main constructs, PU, and PEOU, have been found to spur adoption intentions and performance outcomes in retail and business settings (Ojeka-John et al., 2025). Taken together such studies show the applicability of the TAM in the study of the role of individual and organisational perceptions in shaping technology adoption behaviours within retail and service SME settings, which provides a solid theoretical basis to the current research.

2.2. Key Constructs

Bookkeeping is the process by which financial transactions of a business are systematically captured, organised and tracked. Adequate bookkeeping can ensure effective reporting, minimize errors and enable companies to observe the flow of money and their profitability. This is especially necessary for SMEs, which usually have narrow margins and limited resources (Adela et al., 2024). In the context of this study, hassle-free bookkeeping refers to AI- and automation-enabled streamlined financial recording processes that improve accuracy, save time, and reduce administrative burdens.

In addition, user acceptance is the level at which individuals are ready to use a new technology to perform tasks (Wisdom Library, 2024). When it comes to AI and automation, user acceptance decides whether employees or managers would use these tools to bookkeep. This is significant because successful utilisation, productivity increase, and return on investment in technologies are achieved with high acceptance (Saira et al., 2025). However, when user acceptance is weak, even the most sophisticated tools are not used properly, which leads to the continued presence of manual work, low efficiency, and organisational resistance to change. Digital trust refers to the trust that users have in the reliable functioning, security, and ethical operations of digital systems (World Economic Forum, 2024). It affects how users are willing to share their data, assign some tasks to automated systems, and use technology to perform important business activities (Pietrzak & Takala, 2021). Digital trust is essential because it minimises risk perception and promotes the wider use of technologies. A lack of digital trust can make users fear data loss, information misuse, or algorithm failures, which can make them hesitate to use digital tools or even reject them altogether (Hasija & Esper, 2022). These constructs, combined, influence the successful adoption of AI and automation within the booking systems of SMEs, as well as their final performance. Having a clear picture of every construct assists in explaining the nature of technology behaviour and informs how to advance the digital transformation of business settings.

2.3. Hypothesis Development

(Abidemi, 2024) conducted a study to examine the impact of automation technologies on streamlining business processes and improving business performance among SMEs across different industries, such as retail and services. It was found that those SMEs that adopted automation tools reported a major shift of up to 30% in operational efficiency, a significant 25% reduction in operational errors, and increased productivity, specifically in automated operations like data entry, inventory management, and bookkeeping (Abidemi, 2024). The strength of this study is that it uses sector-specific data, which proves the possibility to document the improvement in performance with the implementation of automation in the real SMEs. The findings offer practical evidence that automation reduces the occurrence of repetitive bookkeeping processes and enhances overall productivity of the businesses. However, a weakness is that it only demonstrates efficiency improvements, but does not directly indicate a bookkeeping-specific effect, and does not directly study retail or service SMEs or account for variation in firm size and technology sophistication, which may limit external validity.

Expanding on these results, the effect of AI adoption in accounting has been also researched to present a complement of the automation-oriented studies. To illustrate, an empirical study on the impact of the adoption of AI on accounting efficiency, data quality, and fraud detection in Lebanese firms showed that AI tools have a significant impact on financial data effectiveness and quality (Bou & Jabbour, 2024). This technology improves fraud detection in financial records and has a positive impact on work activities and skill requirements among accounting teams. The theoretical merit of this study is that AI can be quantitatively supported to improve efficiency and data reliability, which are essential elements of hassle-free bookkeeping, based on a sufficiently large sample of accounting practitioners. However, its major limitation is that it addressed a specific country setting (Lebanon) and not the UK or other industry settings beyond retail and services, which may restrict the external validity of the findings to UK SMEs.

Extending the geographic and contextual scope, (Elom & Atah .2025) conducted a study of SMEs in Cross River State (Nigeria). They studied the effect of computerised accounting systems, such as automation in recording transactions, generating financial reports, and tracking income and expenses on financial performance. It was discovered that automatic recording of transactions and income/expense tracking had a significant and positive influence on financial performance, that is, it enhanced the accuracy and speed of financial data processing. The study is robust as it concentrates on the features of an automated financial system directly correlated with the results of bookkeeping and uses statistical analysis to prove any impact. However, its weakness is that it is geographically located outside the UK and uses cross-sectional survey data, which restricts the ability to cause and generalise. Together, these studies give convergent information that AI and automation technologies can enhance performance of operations, efficiency in accounting and financial data quality processing in small and medium enterprises. Thus, this study proposes Hypothesis 1:

H1: AI and automation have a significantly positive impact on hassle-free bookkeeping among small and medium-sized enterprises in the UK retail and service sectors.

(Relifra et al., 2025) applied an integrated TAM-UTAUT model to conduct an empirical study examining the impact of AI adoption determinants on functional business performance among micro-, small-, and medium-sized enterprises (MSMEs). In particular, it was discovered that behavioural intention (a key user acceptance measure) was a significant mediator between the determinants of AI adoption (e.g., performance expectancy and ease of use) and business performance outcomes (including in areas such as financial operations and operational processes). Behavioural intention reported a substantial variance in functional performance, and user acceptance was observed to be the factor that facilitates adoption drivers in affecting business outcomes in SMEs. This experiment provides the first direct correlation between user acceptance and performance results, which uniquely empowers mediation pathways. However, it is placed in a developing economy and does not specifically look at bookkeeping but at general performance.

Based on this understanding of user acceptance as a mediator, further studies have examined the operation of these constructs in specific accounting technologies. A study centred on SMEs in Denpasar examined the implementation of cloud accounting systems (automation tools), which are closely linked to AI bookkeeping (Putri et al., 2025). The researchers concluded that perceived ease of use and perceived usefulness were important in increasing the system’s effectiveness, and the system’s performance mediated the correlation between user perceptions and the firm’s performance. This is congruent with the fact that user acceptance (measured by perceived usefulness and ease of use) determines the translation of technology into results. Its strength lies in providing first-hand evidence in the SME accounting setting, explaining how the factors of acceptance can be used to translate technology features into performance. However, it is limited, as although relatable, it concentrates on cloud accounting as opposed to specific AI/automation tools and is located geographically outside of the UK.

In addition to the evidence from cloud accounting systems, the literature has further studied how SME technology adoption (AI) unfolds over time and provides insights into broader patterns of system use. A long-term study of the TAM regarding the adoption of Accounting Information Systems (AIS) in Lebanon concluded that perceived usefulness and trust positively impact AIS adoption, and acceptance constructs are also related to actual usage (Dallal & Sankari, 2025). Although this study did not test a complete mediation model involving performance outcomes, it affirmed that acceptance factors are mediators in the relationship between system characteristics and technology adoption behaviour. Strength: It expands TAM using variables applicable to accounting systems and is conceptually consistent with user acceptance in bookkeeping situations. Thus, this study proposes Hypothesis 2:

H2: User acceptance mediates the relationship between AI and automation and hassle-free bookkeeping among SMEs in the UK retail and service sectors.

One study that investigated the acceptance of AI service robots among customers in hospitality settings considered the interaction between trust and technology acceptance constructs in influencing the intention to adopt AI-enabled service automation (Chi et al., 2023). The results revealed that trust in AI is a strong predictor of the intention to use AI service robots, and higher trust levels are correlated with the acceptance of AI tools in service delivery. These findings support the idea that trust moderates the influence of perceptions of AI performance on user acceptance. The strength of this study is based on its service industry background and empirical consideration of trust as a structural influence that correlates with technology acceptance behavioural intentions in hospitality automation. Nevertheless, its greatest weakness is the lack of statistical testing of trust as a mediator between automation features and acceptance, and its sample was also limited to the consumer population and not to SME employees, which limits its generalisability to the organisational setting.

Extending the conceptual role of trust in user acceptance, research has also explored its influence specifically within SMEs, providing a more organizationally relevant perspective. For example, (Subhani et al., 2023) researched the impact of trust in technology on the adoption behaviour of SMEs in the ERP adoption setting. The researchers discovered that trust played a bigger role in enhancing the connection between the effort-related facets of technology (such as effort expectancy and task technology fit) and actual adoption behaviours. This is indicative of the fact that the higher the level of trust in systems, the greater the positive influence of technology’s characteristics on adoption. This provides conceptual evidence that trust is a moderator in technology acceptance models. The merit of this study is its SME focus and moderation analysis, which is consistent with the concept that trust improves the technology acceptance relationship. Nonetheless, its shortcoming is its particular concentration on ERP systems and not on AI/automation bookkeeping aids and geographic locations beyond the UK, which makes it less directly applicable.

Complementing this study, recent research has integrated trust with other key TAM constructs in SMEs to capture its role in AI adoption more comprehensively. (Popa et al., 2025) conducted a PLS-SEM study on the drivers of AI adoption among SMEs and included factors such as AI knowledge, perceived usefulness, ease of use, and trust in a comprehensive TAM. The results indicate that AI system trust has a strong positive impact on the behavioural intention to use AI tools, and that transparency and personalised experiences are significant determinants of trust that play a central role in the intention to use AI by users. Although the moderating effect was not directly tested in the study, it proved that trust positively influences users’ perceptions of AI benefits and usability, which means that the relationship between technology attributes (e.g., perceived usefulness) and acceptance results can be intensified by increasing trust. Thus, this study proposes Hypothesis 3:

H3: Digital trust positively moderates the relationship between AI and automation and User Acceptance, such that the relationship is stronger when digital trust is high.

2.4. Research Gap

Although recent literature has implemented TAM to explore SME technology adoption, some critical gaps remain. The literature supports the applicability of perceived usefulness and perceived ease of use to influence adoption in service, retail, and accounting cases (Dallal & Sankari, 2025; Ojeka-John et al., 2025; Qing et al., 2025). However, a large part of this research looks at general performance outcomes or larger accounting systems as opposed to bookkeeping-specific outcomes, such as hassle-free bookkeeping. In addition, existing research on AI and automation in the accounting field mostly focuses on developing economies (for example, Lebanon and Nigeria), which does not allow contextual generalisation to UK SMEs (Bou & Jabbour, 2024; Elom & Atah, 2025). Although user acceptance has been identified as an intervening variable in technology-performance correlations, very few studies have directly tested this variable in the context of AI-based bookkeeping. Despite trust being proven to affect technology acceptance, there is a lack of research on its moderating effect on TAM-based AI bookkeeping adoption in SMEs. This study fills these gaps by discussing AI-based bookkeeping in UK retail and service SMEs using a mediated and moderated TAM model.

2.5. Conceptual Framework

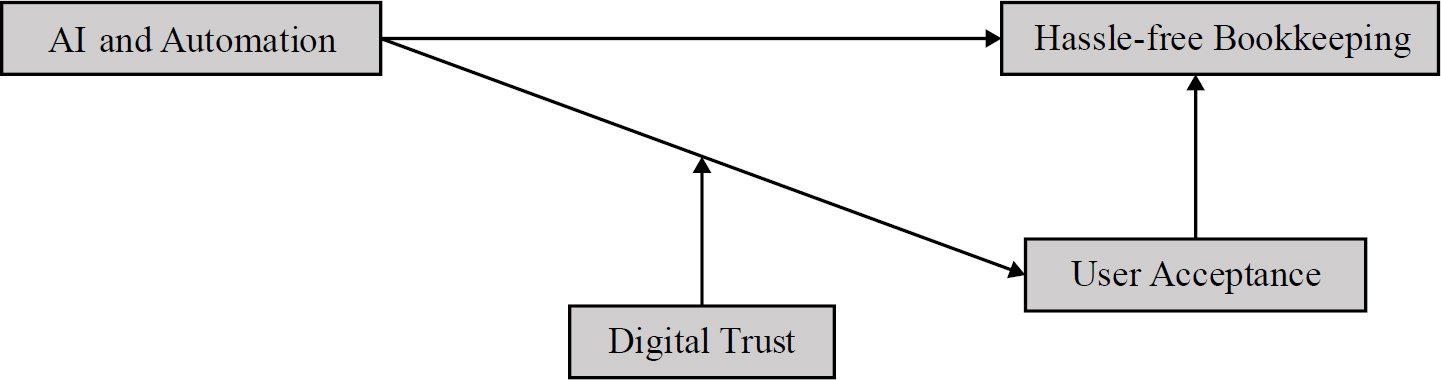

Fig. (1) presents a pictorial and concise view of the generated hypotheses, showing the conceptual framework for this study, which has not been studied simultaneously in a single study. Fig. (1) conceptualises that AI and automation are directly associated with hassle-free. Moreover, user acceptance mediates the relationship between AI and automation and hassle-free bookkeeping, where digital trust moderates this relationship.

Fig. (1). Conceptual framework.

3. METHODOLOGY

This study used a quantitative design, and a structured online questionnaire (close-end questions) was administered using Google Forms to collect data. The respondents were asked to state their degree of agreement with a series of statements on a five-point Likert scale, with 1 and 5 representing strongly disagree being (1) and strongly agree being (5). The rationale for selecting a quantitative design is that it provides objectively measured results for the relationship between variables using numerical data. This enabled robust statistical testing of the hypothesised effects across a large SME sample. Moreover, online questionnaires provide a cost- and time-efficient tool for collecting data.

The questionnaire was designed to comprise four major constructs to be measured through a multi-item scale based on previously tested and validated scales in the literature on technology adoption and accounting, adjusted to the UK SME context (Appendix A). The degree of intelligence was measured using AI and automation and the automated tools that were utilized in the bookkeeping process, including data entry, reconciliation, and reporting. The ease of use and perceived usefulness of AI-based bookkeeping systems were evaluated by user acceptance based on the TAM-inspired model. Digital trust was the degree of belief that respondents placed on the security of the information, stability of the system and intelligibility of AI technologies. Efficiency, accuracy, time-saving, and decreased manual workload were measured as hassle-free bookkeeping. All items were rated on a five-point Likert scale.

The sample was chosen through purposive sampling methodology, whereby only respondents with relevant experience were included. The population of interest was UK SME owners, finance managers, accountants, and operational staff in the service sector and retail, who were knowledgeable of or directly engaged in bookkeeping processes. This type of sampling ensured that the participants who had practical exposure to AI or automation tools and their responses were contextually valid. Invitations to participate in the surveys were sent via professional networking sites such as LinkedIn, SME associations, accounting forums, and groups with a specific industry to increase the number of targeted professionals. The rationale for selecting SMEs for this study is that in the UK, they constitute over 99.8% of businesses; however, they still face prominent challenges in adopting technology due to financial barriers, limited technical expertise, and digital scepticism (GOV.UK, 2025). However, participant recruitment through digital platforms risks the introduction of digital maturity bias, as only those with digital tool accessibility would have participated.

Moreover, considering non-response and incomplete surveys, 850 questionnaires were distributed, and 480 questionnaires were obtained, yielding a response rate of 56.5%. After screening the data for missing responses, straight-lining, and statistical outliers, 410 valid responses were analysed. G*Power’s power analysis was used to verify the sufficiency of the sample size. The minimum sample size, as per the guidelines, must be more than 100 for a medium effect size (0.15), significance level (0.05), and statistical power (= 0.80) (Kang, 2021). As the current study received 410 valid responses, the sample size was sufficiently large to perform PLS-SEM analysis, as it was well above the minimum required.

Although the representativeness of the population was limited due to the purposive sampling approach, the final sample size was sufficient for robust multivariate analysis and hypothesis testing within the study’s defined context.

The Harman single-factor test was used to evaluate the common method bias (CMB), which is suitable for self-reported and cross-sectional survey data. Principal component analysis (PCA) was performed to obtain an unrotated exploratory factor analysis, with all items of measurement inputted in a single operation. The findings indicated that the first unrotated measure explained 38.6% of the total variance, which is less than the widely accepted 50% mark, meaning that none of the constructs had a predominant influence on covariance (Katsekpor et al., 2025). A complete collinearity variance inflation factor (VIF) test was also conducted as well in order to enhance the diagnostic assessment, but all VIF values were lower than the recommended cut-off of 3.3, so the possibility of common method bias was not a major issue (Polas, 2025). Moreover, non-response bias was analysed by comparing early and late respondents through independent-sample t-tests on the major constructs (AI and automation, user acceptance, digital trust, and hassle-free bookkeeping). The findings indicated no statistically significant differences, meaning that non-response bias did not have a significant impact on the results.

Additionally, SmartPLS was used to analyse the data following the Partial Least Squares Structural Equation Modelling (PLS-SEM). The analysis was performed in two steps. In the first step, descriptive statistics and reliability tests, such as Cronbach’s alpha and composite reliability, were used to establish internal consistency. Second, the measurement model was evaluated to determine indicator reliability, convergent validity, and discriminant validity. The structural model was then analysed to test the proposed indirect and conditional relationships (mediation and moderation effects) using bootstrapped path coefficients, indirect effect testing for mediation, and interaction term analysis. The rationale for selecting PLS-SEM is that, first, predictive research commonly relies on PLS-SEM because it focuses more on estimating the strength of the relationships between variables (Dash & Paul, 2021). This study predicts the impact of AI and automation on hassle-free bookkeeping and user acceptance among UK SMEs. Second, PLS-SEM can be applied to complex models that involve many constructs with mediations and moderations (Sarstedt et al., 2020). In this case, it is possible to test the indirect effect of user acceptance and the moderating effect of digital trust. Third, PLS-SEM can withstand non-normal data and smaller and more exploratory samples that are typical of SME research (El Maalmi et al., 2021).

Ethics were strictly adhered to throughout the research process. Responses were voluntary, and the purpose of the study was explained to the respondents prior to completing the survey. Written informed consent was obtained electronically, and the participants were guaranteed anonymity and confidentiality. None of the personally identifiable information was gathered, and responses were used only on an academic basis. The right to drop out of the study without reprimand was granted. Any information was kept safely in password-protected files and processed according to UK data protection laws (GDPR). Institutional research was conducted in accordance with ethical guidelines.

4. RESULTS

4.1. Demographic Analysis

Table 1 shows the demographics of the 410 respondents selected as a sample of UK retail and service sector SMEs. The gender balance of the sample was relatively equal, although there was a minor tendency for men to dominate. The majority of the respondents are in the economically active years of 26 to 45 years, giving it high relevancy in managerial and operational decision-making. Most of the participants had a minimum of a bachelor’s degree which indicates sufficient educational exposure to technology-enabled systems. Moreover, the respondents are SME owners, finance managers, and operational staff, so the participants are directly involved in the decisions of bookkeeping and technology adoption, which reinforces the contextual validity of this study.

Table 1. Demographic analysis (Source: Author’s survey data and analysis, 2026).

| Demographic Variable | Category | Frequency (n) | Percentage (%) |

| Gender | Male | 226 | 55.1 |

| Female | 176 | 42.9 | |

| Prefer not to say | 8 | 2.0 | |

| Age Group | 18–25 years | 64 | 15.6 |

| 26–35 years | 168 | 41.0 | |

| 36–45 years | 112 | 27.3 | |

| 46–55 years | 52 | 12.7 | |

| Above 55 years | 14 | 3.4 | |

| Education Level | Secondary education | 32 | 7.8 |

| Diploma / Vocational | 68 | 16.6 | |

| Bachelor’s degree | 196 | 47.8 | |

| Master’s degree | 96 | 23.4 | |

| Doctorate / Professional qualification | 18 | 4.4 | |

| Job Role | SME Owner / Director | 92 | 22.4 |

| Finance Manager / Accountant | 118 | 28.8 | |

| Operations / Admin Staff | 84 | 20.5 | |

| IT / Systems Support | 46 | 11.2 | |

| Other | 70 | 17.1 |

4.2. Measurement Model

Table 2 presents the findings of the measurement model test based on confirmatory factor analysis. The factor loadings were all greater than the recommended value of 0.70, which indicates a high level of indicator reliability. The alpha and composite reliability (CR) values of all the estimated constructs exceeded 0.70, confirming internal consistency reliability. In addition, the average variance extracted (AVE) values were above the minimum level of 0.50, which proves that there is sufficient convergent validity. The findings are consistent with commonly recognised reliability and validity thresholds (Epebinu et al., 2023; Katsekpor et al., 2025) and affirm that the measurement items are an adequate fit to the corresponding latent constructs.

Table 2. Measurement model (Source: Author’s analysis using SmartPLS based on survey data, 2026).

| Latent Construct | Indicator | Factors Loading | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) |

| AI and Automation | AIA1 | 0.876*** | 0.853 | 0.911 | 0.77 |

| AIA2 | 0.903*** | ||||

| AIA3 | 0.858*** | ||||

| Digital Trust | DT | 0.913*** | 0.898 | 0.936 | 0.831 |

| DT2 | 0.927*** | ||||

| DT3 | 0.894*** | ||||

| Hassle-Free Bookkeeping | HFB1 | 0.782*** | 0.812 | 0.888 | 0.726 |

| HFB2 | 0.898** | ||||

| HFB3 | 0.872*** | ||||

| User Acceptance | UA1 | 0.896*** | 0.881 | 0.927 | 0.808 |

| UA2 | 0.926*** | ||||

| UA3 | 0.873*** |

Note: ***p < 0.001.

4.3. Discriminant Validity

Table 3 shows the results of discriminant validity based on the Heterotrait-Monotrait (HTMT) ratio. The values of all HTMT are significantly lower than the recommended value of 0.85, which shows that all constructs are empirically different. This implies that unique conceptual domains are represented in the model by AI and automation, digital trust, user acceptance and hassle-free bookkeeping. These results present overwhelming proof of discriminant validity, which is aligned with the best practices in PLS-SEM studies (Katsekpor et al., 2025) and suggest that there is no multicollinearity between constructs that can endanger the interpretability of the structural relationships.

Table 3. Discriminant validity (Source: Author’s analysis using SmartPLS based on survey data, 2026).

| – | AI and Automation | Digital Trust | Hassle-Free Bookkeeping |

| Digital Trust | 0.617*** | – | – |

| Hassle-Free Bookkeeping | 0.631*** | 0.473*** | – |

| User Acceptance | 0.717*** | 0.734*** | 0.560*** |

Note: ***p < 0.001.

4.4. Model Explanatory Power

Table 4 displays the coefficients of determination (R2) of the endogenous constructs. The proportion of the variance in hassle-free bookkeeping accounted for by AI and automation, user acceptance, and digital trust is 33.5%, meaning that they have moderate explanatory power. Similarly, AI and automation predicted 39.2% of the variance in user acceptance. The results indicate moderately high values of R2 (0.25-0.50), which are deemed moderate in accordance with the PLS-SEM guidelines, indicating that the model sufficiently accounts for highly important behavioural and outcome variables. These findings indicate that the theoretical framework can be predicted in the context of SME book-keeping.

Table 4. R-square (Source: Author’s analysis using SmartPLS based on survey data, 2026).

| – | R-Square | R-Square Adjusted |

| Hassle-Free Bookkeeping | 0.335 | 0.328 |

| User Acceptance | 0.392 | 0.390 |

4.5. Path Coefficient

Table 5 shows the structural path coefficients and hypothesis testing. These findings show that AI and automation have a positive and significant effect on hassle-free bookkeeping among UK SMEs working in the retail and service segments (β = 0.386, p = 0.001). There was also a significant and positive influence of user acceptance (β = 0.626, p < 0.001) on AI and automation and, in turn, hassle-free bookkeeping (β = 0.187, p < 0.01). The statistical significance of the effect of AI and automation on hassle-free bookkeeping through user acceptance was statistically significant (β = 0.117, p < 0.05), indicating partial mediation. Moreover, digital trust had a strong influence on user acceptance (β = 0.135, p < 0.05) and moderated the effect of AI and automation on user acceptance (β = 0.117, p < 0.05), which is more pronounced when the trust is high. H1 is upheld in the sense that AI and automation have a direct positive effect on hassle-free bookkeeping. H2 is proven by partial mediation with user acceptance, and H3 is proven correct because digital trust enhances the impact of AI and automation on user acceptance, emphasising its moderating role.

Table 5. Path coefficient (Source: Author’s analysis using SmartPLS based on the survey data, 2026).

| – | Path coefficient | T-statistics | P-values |

| Direct Effect | |||

| AI and Automation -> Hassle-Free Bookkeeping | 0.386*** | 6.347 | 0.001 |

| AI and Automation -> User Acceptance | 0.626*** | 19.224 | 0.001 |

| Digital Trust -> User Acceptance | 0.135** | 1.986 | 0.047 |

| Digital Trust x AI and Automation -> User Acceptance | 0.117** | 2.060 | 0.040 |

| User Acceptance -> Hassle-Free Bookkeeping | 0.187** | 2.567 | 0.010 |

| Indirect Effects | |||

| AI and Automation -> User Acceptance -> Hassle-Free Bookkeeping | 0.117** | 2.509 | 0.012 |

Note: p < 0.05 is presented with **, and p < 0.01 with ***

5. DISCUSSION

This study investigated how AI and automation affect hassle-free bookkeeping among SMEs in the UK retail and service industries, and the mediating effect of user acceptance and the moderating effect of digital trust. Through the model based on the TAM, the current study concluded on whether AI-enabled bookkeeping results in an improved operational outcome and how and under which conditions this improvement is realized. The empirical findings indicate that AI and automation play a positive role in hassle-free bookkeeping, the mediations of AI and automation are through user acceptance, and digital trust strengthens the relationship between AI and automation and user acceptance. Taken together, these findings offer subtle data on the technological and behavioural processes affecting the efficiency of bookkeeping among UK SMEs.

The findings revealed that AI and automation had a positive influence on hassle-free bookkeeping to some significant degree, which substantiates that technological tools have a direct positive effect on efficiency, accuracy, and reduced manual labour (β = 0.386, t = 6.347, p < 0.001). The result correlates with those of (Abidemi, 2024), who found that automation technologies introduced considerable improvements in operational efficiency and reduction of errors among SMEs in the retail and service sectors. Though the study by Abidemi did not directly isolate the results of bookkeeping, the present results add to this evidence, as they reveal that all these improvements in efficiency are directly translated into the benefits of bookkeeping. Similarly, the findings can be compared to those of (Bou & Jabbour, 2024), who developed that AI adoption improves the quality and effectiveness of accounting information. Although they applied the country of Lebanon, the fact that their results align with the existing results shows that AI-based innovations in financial data processing are not dependent on a situation. Moreover, (Elom & Atah, 2025) on computerised accounting systems support the argument that the automation of transaction recording and reporting increases the accuracy and speed of processing. Essentials of hassle-free book-keeping. These results suggest that administrative overheads and financial control can be significantly decreased by investing in AI and automation as UK SME. Thus, H1 is accepted.

The findings reveal that user acceptance mediates to a considerable extent between AI and automation, and hassle-free bookkeeping. AI and automation empirically indicate a strong positive influence on user acceptance (β = 0.626, t = 19.224, p = 0.001), but user acceptance is a strong influence on hassle-free bookkeeping (β = 0.187, t = 2.567, p = 0.010). The mediating role highlights that technological benefits are not automatic and, in fact, depend on whether or not users are willing to accept systems based on AI and actively use these systems. This is in line with the TAM, which presupposes that acceptance is predetermined by perceived usefulness and ease of use, which ultimately determines the use of the system and its outcomes.

These findings are in line with those of (Relifra et al., 2025), who showed that behavioural intention is an intervening variable between AI adoption determinants and functional business performance in MSMEs. Similarly, (Putri et al., 2025) demonstrated that perceived usefulness and ease of use significantly affect the effectiveness of cloud accounting systems, which justifies the significance of acceptance mechanisms in accounting-related technologies. This is also supported by (Dallal & Sankari, 2025), who confirmed that acceptance constructs mediate between system characteristics and adoption behaviour in accounting information systems but also affirm that the same does not in other systems. In the case of UK SMEs, this implies that only the implementation of AI tools is not enough; user-centred training, user design, and value communication should be implemented to gain bookkeeping efficiencies. Therefore, H2 is supported by the data.

The results showed that the connection between AI and automation and user acceptance was moderated by digital trust, and the stronger the trust, the stronger the connection. The role of this moderating effect is empirically validated, with a significant interaction term (β = 0.117, t = 2.060, p = 0.040) that shows that trust increases the effect of AI and automation on hassle-free bookkeeping. This is consistent with (Chi et al., 2023), who discovered that the relationship between perceived AI performance and acceptance in hospitality service automation is reinforced by trust. These results are also consistent with those of (Subhani et al., 2023), who found that trust mediates the relationship between technology features and adoption behaviour among SMEs in ERP situations. Despite the fact that ERP systems and AI bookkeeping tools are not similar, the principle of ideas of trust, which improves the influence of technology attributes on acceptance, remains the same. In addition, (Popa et al., 2025) demonstrated that trust significantly affects the behavioural intention to use AI tools by enhancing perceptions of usefulness and ease of use. Though they did not directly test moderation in their study, the current study empirically validates the strengthening effect of trust. In the UK SMEs, it is a call to mind that data security, transparency, and reliability of the system have to be taken into account to accept AI-based bookkeeping solutions. Thereby, H3 is justified.

Overall, this study demonstrates that AI and automation have the potential of supporting the hassle-free bookkeeping in UK-based retail and service SMEs, although the benefits will rely on the acceptance of the user and the strength of digital trust. Although this work builds on the proven TAM, the theoretical contribution of the study is to put the TAM-inspired model in the context of SME bookkeeping, where the lack of resources, inadequate technical skills, and regulations impact adoption patterns. Through user acceptance, specifically AI-driven bookkeeping, the study shows that the process of automating financial processes is different from the adoption of technology in general, especially in terms of its operational, accuracy, and compliance consequences. In addition, the SME setting is a boundary condition of the TAM-inspired model, demonstrating that trust and mediation processes are more varied in the limited level of digital maturity and small-scale organisational set-ups, which provide subtle details on technology acceptance in specialised business processes.

This study offers a more in-depth perspective on the integration of mediation and moderation mechanisms into a TAM-based framework to support the impact of technological, behavioural, and trust-based factors on bookkeeping results. These results are useful both to theory and practice as they demonstrate the importance of human and trust dimensions in digital transformation programmes when it comes to SMEs. However, these results indicate the perceived efficiency of AI-based bookkeeping and not objective performance, which shows the possibility of a perception-performance gap. Therefore, further research should include objective operational measures to confirm self-reported measures.

CONCLUSION

This paper confirmed that AI and automation can significantly enhance the effectiveness of bookkeeping, removing manual labor, enhancing accuracy, and having an easier time with financial functions. It is worth noting that the results show that the acceptance of users is one of the most important processes, thanks to which AI and automation can be converted into hassle-free bookkeeping outcomes, which means that the benefits of technology can be obtained only when users perceive systems as useful and convenient. In addition, digital trust was discovered to enhance the connection between AI and automation and user acceptance, proving that the level of trust in the reliability of the systems, data safety, and transparency is a vital factor in the promotion of adoption in SMEs.

SMEs can follow a step-by-step roadmap to apply AI to practice: firstly, they need to review their current bookkeeping practices, identify the areas that require automation, and finally, they can test AI solutions on low-risk jobs and test it on a large scale. Vendors should be chosen based on those that have transparent pricing, comply with UK data rules and have good customer service. SMEs can build digital trust by using consistent data governance policies, system visibility, and internal and external communication of security controls. The adoption sequence should be mandatory; first of all, routine and high-volume operations (data entry and reconciliation) should be launched, followed by reporting and analytics functionality. A combination of financial support, such as grants or low interest loans, and the corresponding staff training and coherent implementation assists the SMEs to make efficiency gains without overly risking their operations, and in the long term, AI can be completely integrated into the bookkeeping operations.

LIMITATIONS AND FUTURE DIRECTION

The study has a number of limitations despite the contributions it has made. First, the cross-sectional research design prohibits causal generalisation and prevents the possibility of observing changes in adoption behaviour over time. Second, the use of self-reported survey data can lead to bias in responses, as perceptions and not objective performance indicators were assessed. Third, the results of this study were based on UK SMEs operating in the retail and service industries; hence, they might not be generalisable to other industries and larger organisations with varying technological capacities and regulatory environments. Future studies must consider longitudinal research methodology or a mixed-method research approach to identify the shift in the adoption behaviour of AI and automation across time and enable more causal conclusions. In addition, future research might include objective performance measurements, system usage records, or archival financial documentation, which would help reduce self-report bias and enhance measurement validity. Lastly, generalising the study to different industries, larger organisations, and other countries would increase generalisability and enable comparisons under different technological and regulatory conditions.

LIST OF ABBREVIATIONS

AI | = | Artificial Intelligence |

AIS | = | Accounting Information Systems |

AVE | = | Average Variance Extracted |

CR | = | Composite Reliability |

CMB | = | Common Method Bias |

MSMEs | = | Micro Small and Medium-Sized Enterprises |

PU | = | Perceived Usefulness |

PCA | = | Principal Component Analysis |

PEOU | = | Perceived Ease of Use |

PLS-SEM | = | Partial Least Squares Structural Equation Modelling |

SMEs | = | Small and Medium-Sized Enterprises |

TAM | = | Technology Acceptance Model |

VIF | = | Variance Inflation Factor |

AUTHOR’S CONTRIBUTION

A.B has contributed to the study conceptualization, methodology, data analysis, interpretation of results, and manuscript writing.

ETHICAL APPROVAL & INFORMED CONSENT

Ethics were strictly adhered to throughout the research process. Responses were voluntary, and the purpose of the study was explained to the respondents prior to completing the survey. Written informed consent was obtained electronically, and the participants were guaranteed anonymity and confidentiality. None of the personally identifiable information was gathered, and responses were used only on an academic basis. The right to drop out of the study without reprimand was granted. Any information was kept safely in password-protected files and processed according to UK data protection laws (GDPR). Institutional research was conducted in accordance with ethical guidelines.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [A.B].

FUNDING

None.

CONFLICT OF INTEREST

The author declares that there is no conflict of interest regarding the publication of this article.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language editing and refinement purposes. Following the use of this tool, the author carefully reviewed and revised the content where necessary and accept full responsibility for the final published version of the article.

APPENDIX A: QUESTIONNAIRE

Section A: Demographics

- Gender

- Male

- Female

- Prefer not to say

- Age Group

- 18–25 years

- 26–35 years

- 36–45 years

- 46–55 years

- Above 55 years

- Education Level

- Secondary Education

- Diploma or Vocational Qualification

- Bachelor’s Degree

- Master’s Degree

- Doctorate or Professional Qualification

- Job Role in SME

- SME Owner or Director

- Finance Manager or Accountant

- Operations or Administrative Staff

- IT or Systems Support

- Other

Scale:1 = Strongly Disagree, 2 = Disagree, 3 = Neutral, 4 = Agree, 5 = Strongly Agree

| Construct | Item Code | Questionnaire Item | 1 | 2 | 3 | 4 | 5 |

| AI and Automation | AIA1 | Our organisation employs AI or automated solutions to support bookkeeping operations, including data entry and transaction recording. | ☐ | ☐ | ☐ | ☐ | ☐ |

| AIA2 | AI systems are useful for automating typical accounting jobs, such as reconciliation, financial tracking, and report creation. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| AIA3 | AI and automation have enhanced the speed and efficiency of bookkeeping in our organisation. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| User Acceptance | UA1 | In my day-to-day work, I find AI-based bookkeeping systems readily comprehensible and easy to use. | ☐ | ☐ | ☐ | ☐ | ☐ |

| UA2 | Financial recording is one of the tasks that I can perform better with the help of AI-empowered bookkeeping tools. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| UA3 | I would be glad to apply AI-based systems in the process of bookkeeping and financial management regularly. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| Digital Trust | DT1 | I trust that AI-powered bookkeeping systems store financial data safely and ensure confidential business information. | ☐ | ☐ | ☐ | ☐ | ☐ |

| DT2 | In my opinion, AI and automated systems deliver quality and trustworthy results for bookkeeping tasks. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| DT3 | I am not afraid to use AI technologies for financial record-keeping and bookkeeping decisions. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| Hassle-Free Bookkeeping | HFB1 | AI-powered tools simplify the bookkeeping process and minimise the amount of manual work required to document financial transactions. | ☐ | ☐ | ☐ | ☐ | ☐ |

| HFB2 | Automated book keeping saves time and makes financial record keeping easier in our organisation. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| HFB3 | AI and automation can reduce the number of mistakes and simplify and streamline bookkeeping. | ☐ | ☐ | ☐ | ☐ | ☐ |

REFERENCES

Abidemi, A. (2024). The role of technology and automation in streamlining business processes and productivity for SMEs. International Journal of Entrepreneurship, 7(3), 25–42.

https://doi.org/10.47672/ije.2510

Adela, V., Agyei, S. K., Frimpong, S., Awisome, D. B., Bossman, A., Abosompim, R. O., … & Ahmed, A. M. A. (2024). Bookkeeping practices and SME performance: The intervening role of owners’ accounting skills. Heliyon, 10(1). e23911.

https://doi.org/10.1016/j.heliyon.2023.e23911

Brooks, S. (2023). Accounting tasks are still the bane of SMEs. Enterprise Times. Available from: https://www.enterprisetimes.co.uk/2023/08/22/accounting-tasks-are-still-the-bane-of-smes/ (Accessed on: 22 Aug, 2023).

Chi, O. H., Chi, C. G., Gursoy, D., & Nunkoo, R. (2023). Customers’ acceptance of artificially intelligent service robots: The influence of trust and culture. International Journal of Information Management, 70, 102623.

https://doi.org/10.1016/j.ijinfomgt.2023.102623

Dallal, N., & Sankari, A. (2025). Investigating the extended TAM model effects on AIS adoption in Lebanese SMEs operating in Tripoli North Lebanon. Social Sciences & Humanities Open, 11, 101555.

https://doi.org/10.1016/j.ssaho.2025.101555

Dalsaniya, A., & Patel, K. (2022). Enhancing process automation with AI: The role of intelligent automation in business efficiency. International Journal of Science and Research Archive, 5(2), 322-337.

https://doi.org/10.30574/ijsra.2022.5.2.0083

Dash, G., & Paul, J. (2021). CB-SEM vs PLS-SEM methods for research in social sciences and technology forecasting. Technological Forecasting and Social Change, 173, 121092.

https://doi.org/10.1016/j.techfore.2021.121092

El Maalmi, A., Jenoui, K., & El Abbadi, L. (2021). Comparison study between CB-SEM and PLS-SEM for sustainable supply chain innovation model. In International Conference on Advanced Technologies for Humanity (pp. 537-552). Cham: Springer International Publishing.

https://doi.org/10.1007/978-3-030-94188-8_48

Elom, J.O. & Atah, C.A. (2025). Impact of Computerized Accounting Systems on the Financial Performance of Small and Medium Enterprises (SMEs) in Cross River State. Mediterranean Journal of Social Sciences, 16(4), 28.

https://doi.org/10.36941/mjss-2025-0035

Epebinu, O., Adepoju, A., & Ajayi, M. (2023). E-compensation management and organisational performance: An empirical evaluation using partial least squares-structural equation modelling. International Journal of Management Studies and Social Science Research, 5(3), 142-153.

https://doi.org/10.56293/IJMSSSR.2022.4623

Eziefule, A. O., Adelakun, B. O., Okoye, I. N., & Attieku, J. S. (2022). The role of AI in automating routine accounting tasks: Efficiency gains and workforce implications. European Journal of Accounting, Auditing and Finance Research, 10(12), 109-134.

https://doi.org/10.37745/ejaafr.2013/vol10n12109134

Fang, L., Yuan, Z., Zhang, K., Donati, D., & Sarvary, M. (2025). Generative AI and firm productivity: Field experiments in online retail. ArXiv Preprint arXiv:2510.12049.

https://doi.org/10.48550/arXiv.2510.12049

GOV.UK (2025). SME Digital Adoption Taskforce: final report. GOV.UK. Available from: https://www.gov.uk/government/publications/sme-digital-adoption-taskforce-final-report/sme-digital-adoption-taskforce-final-report (Accessed on: 31 July, 2025).

Hasija, A., & Esper, T. L. (2022). In artificial intelligence (AI) we trust: A qualitative investigation of AI technology acceptance. Journal of Business Logistics, 43(3), 388-412.

https://doi.org/10.1111/jbl.12301

Kang, H. (2021). Sample size determination and power analysis using the G*power software. Journal of Educational Evaluation for Health Professions, 18(17), 17.

https://doi.org/10.3352/jeehp.2021.18.17

Katsekpor, J. C., Marfo, M., Nyamuame, E. A., & Annan, E. (2025). Corporate environmental accounting and financial performance in Ghana’s upstream petroleum sector: mediating roles of organisational culture and stakeholder pressure. International Journal of Business and Management, 20(4), 223.

https://doi.org/10.5539/ijbm.v20n4p223

Kitsantas, T., Georgoulas, P., & Chytis, E. (2024). Integrating robotic process automation with artificial intelligence for business process automation: Analysis, applications, and limitations. Journal of System and Management Sciences, 14(7), 217-242.

https://doi.org/10.33168/JSMS.2024.0712

Mogaji, E., Viglia, G., Srivastava, P., & Dwivedi, Y. K. (2024). Is it the end of the technology acceptance model in the era of generative artificial intelligence? International Journal of Contemporary Hospitality Management, 36(10), 3324-3339.

https://doi.org/10.1108/IJCHM-08-2023-1271

Ojeka-John, R.O., Suemo, J.S., Adu, A., Olugbemi, Matthew.A., Akerele, O.E. & Moyinoluwa, I. (2025). Employing the Technology Acceptance Model (TAM) to Explain Digital Video Marketing Adoption and Sales Performance in Selected Nigerian MSMEs. International Journal of International Relations, Media and Mass Communication Studies, 11(1), 55–73.

https://doi.org/10.37745/ijirmmcs.15/vol11n15573

Peláez, M. M., & Aguirre Álvarez, Y. A. (2025). Robotic process automation technology applied to the management of SMEs in the manufacturing and service sector: A systematic review. Revista Universidad y Empresa, 27(48), 14237.

https://doi.org/10.12804/revistas.urosario.edu.co/empresa/a.14237

Pietrzak, P., & Takala, J. (2021). Digital trust–asystematic literature review. Forum Scientiae Oeconomia, 9(3-4), 1-13.

https://doi.org/10.23762/FSO_VOL9_NO3_4

Polas, M. R. H. (2025). Common method bias in social and behavioral research: Strategic solutions for quantitative research in the doctoral research. Journal of Comprehensive Business Administration Research. 1(1), 1-12.

https://doi.org/10.47852/bonviewJCBAR52024285

Popa, R. G., Popa, I. C., Ciocodeică, D. F., & Mihălcescu, H. (2025). Modeling AI adoption in SMEs for sustainable innovation: A PLS-SEM approach integrating TAM, UTAUT2, and contextual drivers. Sustainability, 17(15), 6901.

https://doi.org/10.3390/su17156901

Prarthanna, G., & Vadivel, M. (2025). A study on AI and its impact on financial accounting. International Journal of Research Publication and Reviews, 6(49), 5146–5155.

https://doi.org/10.55248/gengpi.6.0925.3561

Putri, N. P. A. P., Permana, G. L. P., & Mohaidin, N. J. (2025). Perception and digital transformation: A Study of Cloud Accounting Adoption among SMEs in Denpasar. Reviu Akuntansi Manajemen dan Bisnis, 5(2), 413–428.

https://doi.org/10.35912/rambis.v5i2.5505

Qing, S.K., Sulaiman, A., Zakaria, N., Foo, S. M., & Kamaludin, K. (2025). Advancing sustainable technology adoption: Insights from SMEs in beauty, health, and wellness sectors. Sustainable Technology and Entrepreneurship, 5(1), 100122.

https://doi.org/10.1016/j.stae.2025.100122

Reslan, B. F., & Al Maalouf, J. N. (2024). Assessing the transformative impact of AI adoption on efficiency, fraud detection, and skill dynamics in accounting practices. Journal of Risk and Financial Management, 17(12), 577.

https://doi.org/10.3390/jrfm17120577

Relifra, R., Mardiah, A., & Fikriando, E. (2025). AI adoption and functional performance in MSMEs: Evidence across marketing, HR, finance, and operations. Amkop Management Accounting Review (AMAR), 5(2), 1212-1233.

https://doi.org/10.37531/amar.v5i2.3299

Restrepo, P. (2024). Automation: Theory, evidence, and outlook. Annual Review of Economics, 16(1), 1-25.

https://doi.org/10.1146/annurev-economics090523-113355

Saira, S., Ali, S., & Odeh, C. D. (2025). The impact of technology on business in the United Arab Emirates: A technology acceptance model perspective. Journal of Applied Economic Research, 24(2), 462-490.

https://doi.org/10.15826/vestnik.2025.24.2.016

Sarstedt, M., Hair Jr, J. F., Nitzl, C., Ringle, C. M., & Howard, M. C. (2020). Beyond a tandem analysis of SEM and PROCESS: Use of PLS-SEM for mediation analyses! International Journal of Market Research, 62(3), 288-299.

https://doi.org/10.1177/1470785320915686

Stevens, Z. (2024). The Pitfalls of Manual Bookkeeping and the Automated Solutions Protea. Available from: https://proteafinancial.com/the-pitfalls-of-manual-bookkeeping-and-the-automated-solutions-available/ (Accessed on: 30 May, 2024).

Stryker, C. & Kavlakoglu, E. (2024). What is artificial intelligence (AI)? IBM. Available from: https://www.ibm.com/think/topics/artificial-intelligence

Subhani, W., Latiff, A. S. A., & Wahab, S. A. (2023). Effort expectancy, task technology fit, and ERP adoption behavior: Moderating effect of trust in technology: evidence from SMEs of Pakistan. Pakistan Journal of Commerce and Social Sciences (PJCSS), 17(3), 424-445.

https://doi.org/10.64534/Commer.2023.067

UN Trade and Development (2025). AI Market Projected to Hit $4.8 Trillion by 2033, Emerging as Dominant Frontier Technology. UN Trade and Development (UNCTAD). Available from: https://unctad.org/news/ai-market-projected-hit-48-trillion-2033-emerging-dominant-frontier-technology (Accessed on: 7 Apr, 2025).

Wisdom Library (2024). User acceptance: Significance and symbolism. Wisdomlib.org. Available from: https://www.wisdomlib.org/concept/user-acceptance (Accessed on: 12 Jan, 2026).

World Economic Forum (2024). About Digital Trust. Available from: https://initiatives.weforum.org/digital-trust/home