Article ID: PD2602201007

Views: 227Determinants and Relationship Between Official and Parallel Exchange Rates: Evidence from Pakistan

PDF

PDF

⬇ Downloads: 7

1College of Business Administration, Imam Abdulrahman Bin Faisal University, Saudi Arabia;

2Department of Finance, Al-Yammamh University, Khobar, Saudi Arabia

Received: 10 February, 2026

Revised: 02 April, 2026

Accepted: 22 April, 2026

Published: 23 May, 2026

Abstract:

Introduction: This article examines the predictors of official and parallel open-market exchange rates in Pakistan. It also investigates whether both exchange rates move together. In addition, it identifies structural factors that drive persistent exchange-rate divergence.

Methods: The analysis uses both an exchange-rate series and an additional ARDL model to investigate the relationship between official and parallel rates, employing a moving-average approach with annual data (1996-2025). The stability, speed of adjustment, and short- and long-run effects were evaluated using unit root tests and the ARDL model.

Results: The ARDL analysis confirms a stable long-run relationship among macroeconomic indicators and exchange rates in a dual exchange rate system. In the long term, inflation and GDP are found to have positive, statistically significant impacts on both the official and parallel exchange rates. On the other hand, interest rates have a significant steadying impact. In the short run, adjustments in the exchange rate are primarily driven by variations in the interest rate and output shocks, whereas reserves and imports remain insignificant.

Conclusion: The results point to Pakistan’s susceptibility to inflationary forces, policy-rate distortions, and structural imbalances. Inflation stabilization, greater adequacy of reserves, and reduced regulatory distortions between the official and open markets are necessary to curb speculation, narrow premium gaps, and enhance exchange-rate stability.

Keywords: Exchange rate; parallel exchange rates; official exchange rate; inflation; interest rates.

1. INTRODUCTION

Over the past few years, the Pakistani rupee (PKR) has depreciated sharply against the U.S. dollar. This has exposed structural weaknesses in the Pakistani economy. In mid-2025, the official (interbank) exchange rate dropped to about PKR 282 per USD, the lowest in four months since late 2023, according to (News, 2025). This ongoing decline has tightened the strain on import-reliant sectors and raised the price of essential goods. These factors have contributed to surging inflation and increased financial instability, as emphasized by (Ankit, 2023; and Khalid et al., 2024).

Depreciation is based on several interlocking factors. High import demand and slow export growth have led to persistent trade and current account deficits. These deficits have drained foreign-exchange reserves and undermined the rupee’s external position, as noted by (Inyang et al., 2023). Another challenge was domestic inflationary pressures. (Ahmed, 2024; and Shad, 2025) noted that uncertainty about policy and variability of capital flows, such as remittances and servicing of external debt, have contributed to volatility. Special attention should be paid to two exchange rates, which are the official (interbank) rate that is set by the State Bank of Pakistan (SBP) and the parallel (open-market or black-market) rate that is promoted by supply and demand in informal foreign-exchange markets unveiled by (Farooq, 2023; and Ullah et al., 2023) as well. In this perspective, (Sahar et al., 2025; and Shad, 2025) specified that the presence of a large and consistent difference between these two rates is an indicator not just of disequilibrium in currency markets but also of more profound economic strain, such as dollar shortages, capital flight, and the growth of the shadow-market presence.

The current research is driven by the increasing significance of the rate differential and the absence of long-term analysis of the determinants and dynamics of the rate differentials in Pakistan. Although the amount of anecdotal evidence and media coverage is readily available, there has been a dearth of empirical studies that compare the rates of the official and parallel rates in the long run and explore the factors that motivate this difference. This study fills this gap by collecting historical data on the two rates, analyzing various macroeconomic variables, and empirically examining the links among them.

To enhance the theoretical foundation, this study incorporates fundamental exchange rate theories within the dual-market framework of Pakistan. According to Purchasing Power Parity (PPP), as argued by (Phuc & Duc, 2021), a stable inflation differential can lead to long-term changes in the exchange rates, as the parallel market does not respond identically to domestic price levels when they diverge from those of the trading partners. The Interest Rate Parity (IRP) holds that short-term variations in interest rates generate capital flows incentives and increase volatility in less-regulated parallel markets, as argued by (Nurjanah & Mustika, 2021). While Monetary (Gajurel, 2022) specifies that the Exchange Rates model highlights the effects of domestic money supply and liquidity status on the value of the currency, it also provides an opportunity to comprehend the mechanisms of monetary growth or shrinkage on the official and parallel rates. More importantly, in conjunction with the Flow Model and the Monetary Approach, it is likely to have a subtle assessment of short-run speculative reactions and long-term structural fundamentals to understand the asymmetric behaviour of segmented markets in Pakistan.

Moreover, macroeconomic factors, including inflation and GDP, are also exchange rate determinants since they affect the demand and supply of foreign currency in an economy (Huawei et al., 2022). As stressed by (Gajurel, 2022), increased inflation lowers local purchasing power and, in many instances, causes currency devaluation, as continued price differentials change trade competitiveness. Similarly, (Nurjanah & Mustika, 2021) illustrate that GDP growth influences exchange rates through its impact on import demand and capital flows; GDP growth is often shown to raise foreign currency demand in economies that are heavily reliant on imports, as suggested by (Djalo et al., 2023) as well. On the other hand, there is a two-way macroeconomic correlation between exchange rate movements and inflation and growth, driven by the impact on import prices, external competitiveness, and investment.

This study aims to empirically examine the macroeconomic determinants of official and parallel exchange rates in Pakistan from 1996 to 2025. It also tests the dynamic relation between the two markets using the ARDL framework. The research question is stated as:

- What macroeconomic factors determine the official and parallel exchange rates in Pakistan, and how do these determinants differ across the two markets in the short run and long run?

The study makes a substantial contribution to the existing body of knowledge and policy debate in numerous ways:

- Theoretical contribution: It expands the understanding of exchange rate determination in emerging economies. These markets feature dual currency systems and structural macroeconomic imbalances.

- Empirical contribution: This study provides longitudinal evidence from Pakistan. It identifies the parallel market premium and measures macroeconomic factors in the divergence between official and parallel exchange rates.

- Policy contribution: It guides policymakers, such as central bank authorities and fiscal regulators, with information on relevant macroeconomic conditions that increase exchange rate volatility and on market segmentation that is difficult to fix

2. Literature Review

2.1. Theoretical Framework

The conceptual framework of the study is mainly the traditional flow model and the monetary approach of the exchange rate determination. According to (Jamil et al., 2023; and Maqsood et al., 2023), the Traditional Flow Model assumes that exchange rates are changed in reaction to the imbalance in the trade and external-sector flows, especially in cases when persistent current account deficits augment the demand for foreign currency. This school of thought emphasizes the influence of the external-sector variables, which include exports, imports, remittances, and foreign exchange receipts, in the determination of the changes in the exchange rate, as indicated in the analysis of (Djalo et al., 2023). In structural economies that rely on imports, such as Pakistan, permanent shortages of foreign exchange can exert pressure on the official exchange rate and can also promote the growth of parallel currency markets. These dynamics show that trade imbalances and the lack of foreign currency, which, as per (Huawei et al., 2022; Karamelikli & Karimi, 2022; and Rajkovic et al., 2020), create incentives to transact in the informal market, which has been observed in emerging economies with exchange controls.

Monetary Approach, on the other hand, states that the exchange rates represent relative money supply, future inflation expectations, and macroeconomic stability, which is also reflected by (Malec et al., 2024). This theory is especially applicable to Pakistan, where it is common to find inflationary pressures (Sarwar et al., 2023), monetary expansion (Gulzar et al., 2024), and falling real interest rates in an expanding parallel-market premium, which (Hatmanu et al., 2020; and Sujianto, 2020) also highlighted. It assumes that the creation of currency depreciation is the result of money market disequilibrium that leads to the speculative exchange of foreign currency, as postulated by (Boburmirzo & Boburjon, 2022; and Turna & Özcan, 2021) as well. Together, the theories warrant the analysis of the macroeconomic factors of official and parallel exchange rates in the study. Their combination provides a wider perspective through which to assess the joint effect of external-sector pressures (Waseem et al., 2025) and domestic monetary imbalances (Azeem et al., 2025) in the formation of the dual-rate dynamics of Pakistan.

Besides, the Traditional Flow Model and the Monetary Approach are combined in this work, expressly mapping them to variables and adjustment horizons. The Flow Model assumes that real-sector fundamentals of GDP, imports, and balance of payments are the exchange rate determinants whose influences take time to emerge and thus are likely to prevail in the long run, especially in the regulated official markets suggested by (Umeaduma & Dugbartey, 2023). Conversely, as per (Gajurel, 2022), the Monetary Approach focuses on inflation rates, interest rates, and monetary conditions that change swiftly through expectations and liquidity, and consequently, greater short-run effects are observed, particularly in parallel markets when prices adjust easily to policy signals and speculative forces.

2.2. Empirical Review

The exchange rate determinants, mainly GDP, inflation, and interest rates, have a central role in the determination of both official and parallel markets and have a consequence on policy making in the dual market economies such as Pakistan. As was shown by (Wasiu et al., 2019), in Nigeria, the official exchange rate is heavily dependent on the GDP, inflation, and interest rates, whereas the parallel market is mostly dependent on GDP and inflation. These results are in line with the Traditional Flow Model, in which real-sector variables, including output, trade flows, and national income, are important for establishing external balance, as suggested by (FoEh et al., 2020; Nurjanah & Mustika, 2021; and Sari et al., 2023). Their reliance on quarterly ARDL modelling, however, cannot capture high-frequency shocks, as well as speculative pressures and liquidity shocks, which are essential when operating in parallel markets. These are the principal points of the Monetary Approach that emphasize monetary aspects, such as the money supply and interest rate dynamics, as the main forces behind short-term exchange rate fluctuations.

Furthermore, (Phuc & Duc, 2021) also discuss the volatility of inflation and interest rate adjustments as another defining factor of exchange rate pass-through to domestic prices, as an example of how monetary stability can interact with market-specific transmission channels. A combination of these theoretical and empirical views explains why Pakistan’s exchange rates should be analyzed using both real-sector and monetary frameworks, which can capture long-run fundamentals and short-run market pressures. In the same vein, (Olamide et al., 2022) examined exchange rate instability, inflation, and growth in SADC countries and concluded that inflation and exchange rate volatility are the two factors that reduce economic growth. Their panel ARDL-PMG model is robust for explaining cross-country heterogeneity, but parallel-market data have not been included, limiting its generalizability to economies with a large informal FX market.

In addition, (Jihadi et al., 2021) use the firm-level Indonesian data to investigate the impact of exchange rates on the stock returns based on inflation and interest rates. Although their path analysis highlights the mediating system of interest rates as per monetary models, the corporate-level concentration of interest limits generalization to the macro-level. Based on these developing arguments from the literature review, the following hypotheses of the study are formulated:

H1: There is a statistically significant effect of GDP on Official and Parallel Exchange rates in the context of Pakistan.

H2: There is a statistically significant effect of Inflation on Official and Parallel Exchange rates in the case of Pakistan.

H3: There is a statistically significant effect of Interest Rates on Official and Parallel Exchange rates in the context of Pakistan.

The body of literature on the role of balance of payments (BoP), foreign reserves, and imports in the dynamics of the exchange rates provides critical information on how the fundamentals of the external sector determine official and parallel currency markets. (Umeaduma & Dugbartey, 2023) highlight that volatility of the exchange rates has a significant effect on the competitiveness in exports and trade balances in emerging economies. Although their analysis does not directly model the reserves or the positions of the Bank of Poland, it depicts that currency instability amplifies demand of foreign currency, and their findings indicate the presence of depreciation pressures, which are consistent with the Traditional Flow Model, identifying a relationship between trade imbalances and exchange rate changes reflected by (Damayanti & Darmawan, 2024; Sen et al., 2020) as well. Nevertheless, the multi-country qualitative design does not have the econometric accuracy needed to subdivide BoP and import flows in a two-market system, which restricts their direct application to Pakistan.

On the other hand, (Gajurel, 2022) analyzes foreign exchange reserves in Nepal through a 40-year ARDL-ECM model and impulse response analysis and concludes that GDP per capita, inflation, and the official exchange rate have a positive impact on the reserves, and gross capital formation has a negative impact on foreign exchange reserves in Nepal. Although the weak significance of current account balance and trade balance shocks has been noted, impulse responses have indicated that the current account shock has a significant impact on reserves.

This is in line with the Monetary Approach that focuses on using the monetary conditions and reserves to stabilize currency markets, which is also revealed by (Ektiarnanti et al., 2023; and Hossain et al., 2024) in their findings. However, the analysis ignores speculative forces and liquidity gaps that are essential in the two-rate market in Pakistan, where the parallel market is related to the official rates and reserves react to official and unofficial pressures. On the basis of these findings, the study critically assumes that BoP, reserves, and imports in determining the official and parallel exchange rate in Pakistan represent a structural and speculative mechanism that is characteristic of a dual-market framework. Therefore, these emerging arguments from the literature review led to the formulation of the following hypotheses of the study;

H4: There is a statistically significant effect of Balance of Payments on Official and Parallel Exchange rates in the context of Pakistan.

H5: There is a statistically significant effect of Foreign Reserves on Official and Parallel Exchange rates in the context of Pakistan.

H6: There is a statistically significant effect of Imports on Official and Parallel Exchange rates in the context of Pakistan.

(Kalu et al., 2019) analyse the exploitation of the exchange rate-reserve nexus in Nigeria using ARDL and correlation analyses and find that the long-run relationship between real exchange rates and reserves is positive. They point out that depreciation can occasionally be accompanied by increased reserve accumulation due to valuation effects or policy interventions, which are reminiscent of precautionary motives, as explained by (Damayanti & Darmawan, 2024; and FoEh et al., 2020). However, the study’s time range (1996-2016), the number of determinants, and the structural-break tests limit its generalizability.

(Lee & Yoon, 2020) pursue a more sophisticated quantile-Granger approach to examine asymmetric reserve-exchange rate relationships in East Asian economies. Their findings indicate a high level of tail dependence, with reserves having a stronger stabilizing effect during extreme currency movements. This methodology’s elegance represents nonlinear dynamics that were not previously included in earlier research.

Nevertheless, narrowing the focus to developed Asian economies overlooks the importance of informal FX channels in parallel-rate environments. In general, these works emphasize the key functions of BoP conditions, reserves, and import pressures in the determination of the exchange rates, but they also indicate the gaps in terms of the exchange rate behaviour in parallel markets, as well as the long-run relationship between the two exchange rates that can be observed in the case of Pakistan. Based on these developing arguments from the literature, the following H7 of the study is formulated;

H7: There is a statistically significant relationship between the Official and Parallel Exchange Rates of Pakistan.

2.3. Research Gaps

Though exchange rate dynamics are broadly examined and analyzed in the existing literature, comparatively rarer studies clearly examine economies operating under dual or segmented exchange rate markets. For instance, much of the empirical literature emphasizes official exchange rate dynamics, whereas fewer studies jointly assess and evaluate official and parallel exchange rate markets in developing countries such as Pakistan. Works like (Gajurel, 2022; and Kalu et al., 2019) consider official exchange rates and reserves but do not consider the parallel or open-market rate, which in some countries, such as Pakistan, is responsive to external economic shocks, liquidity shortages, and speculative pressure. Such disregard for parallel-market behaviour creates a gap, as the relationship between official and informal currency markets remains poorly theorized and empirically tested.

Second, methodological weaknesses are due to the overwhelming use of linear ARDL or correlation-based models that presuppose the homogeneity and symmetry of responses over time. Although (Lee & Yoon, 2020) adopt quantile-based methods, most other studies do not take into account nonlinearity, structural breaks, and dual-market interactions, which are especially applicable to economies that are undergoing persistent balance-of-payments stress and disordered policy regimes. Moreover, literature rarely incorporates BoP position, reserves, and import demand in a two-rate model. Third, the short or regionally specific sample used in the previous studies tends to restrict the generalization of the research to South Asian settings. Thus, the major gap in research is not the fact that there is a lack of existing literature that provides the study of dual exchange rate, but rather the lack of empirical evidence that can investigate the summary of the determinants of official and parallel exchange rate in the context of the macroeconomy in Pakistan over a lengthy period of time.

3. METHODS

3.1. Research Design and Data Collection

The research design applied in this study is a secondary quantitative research design that is applied to analyse the relationships of macroeconomic indicators based on historical time-series data that are registered and publicly accessible, as suggested by (Ebrahim et al., 2020). The time series data of the study, measured on a YoY basis in the context of Pakistan over a time span of 30 years, 1996 to 2025, is collected. Also, the annual data is used to reflect the underlying macroeconomic fundamentals as opposed to short-term fluctuations in the market, which are speculative in nature. The influence of the structure and the policy on the exchange rates is captured in the variables like GDP, inflation, and reserves, and the rapid speculative changes of the parallel market may not be observed with the same frequency.

Thus, it focuses on the long-term relationships and the underlying determinants instead of the short-term speculation in the market. This sampling frame is supported by the necessity to find many exchange rate regimes, repetitive balance-of-payments stresses, changes in reserves, and increasing parallel-market premiums at this time. The econometric inference is also improved by the longer time horizons since they can absorb structural shocks in the economy, like the episode of sanctions in the year 1998, the 2008 financial crisis, the 2018-2023 IMF programmes, and the recent post-pandemic volatility. In line with the time-series studies on economics, this era offers enough observations that can be used to model dual exchange rate behaviour.

These variables are: official exchange rate (USD/PKR), parallel/open-market exchange rate (USD/PKR), GDP (current USD), inflation (CPI%), interest rate, current account balance (BoP), foreign exchange reserves (current USD), and imports (current USD), which are also indicated in Table 1. The data on exchange rates are obtained at the State Bank of Pakistan and the World Bank, the data on the parallel market is obtained at FRED, local financial market reports, documented open-market premiums, and the data of macroeconomic indicators are obtained at the World Development Indicators (World Bank), International Financial Statistics (IMF), and the World Economic Forum. The use of internationally standardized data collected from authorized and official sources assists in the measurement of comparability and accuracy, which is also suggested by (Müller et al., 2025).

Table 1. Variables measurement.

Variable | Symbol | Measurement / Operational Definition | Data Source |

Parallel / Open Market Exchange Rate (USD/PKR) Annual Average | PEXR | Market-determined exchange rate in the open/parallel currency market; reflects unofficial USD–PKR rate. | Investing.com |

Official Exchange Rate (USD/PKR) Annual averages | OEXR | State Bank of Pakistan (SBP) interbank USD–PKR exchange rate | World Development Indicators (WDI) |

Gross Domestic Product (Current USD) | GDP | Value of total domestic output measured in current U.S. dollars | World Development Indicators (WDI) |

Inflation (Consumer Price Index, Annual %) | INF | Annual percentage change in CPI, measuring general price level increases | World Development Indicators (WDI) |

Interest Rate (Policy/Discount Rate) | INT | The central bank policy rate represents the cost of borrowing and the monetary stance. | World Development Indicators (WDI) |

Current Account Balance (BoP) | CAB | Net balance of goods, services, income, and transfers on the balance of payments | World Development Indicators (WDI) |

Foreign Exchange Reserves (Current USD) | RES | Total official foreign currency reserves, including SBP-held assets | World Development Indicators (WDI) |

3.2. Variables and Measurement

The official and parallel exchange rates in Table 1 are measured as annual averages and not end-of-year values, which aligns with the focus of the study that addresses the macroeconomic fundamentals and not the movements of short-term speculative changes. The parallel exchange rate is the average USD/PKR rate of the open market that is reported on a yearly basis and found in the official market sources, making it consistent in the sample period. Despite the existing various market quotations, there is only one standardized series given to avoid noise in measurements. There is no transformation done at a higher premium, but instead, the official and parallel exchange rates are levelled to facilitate a direct comparison of the structural determinants.

Furthermore, when modelling the parallel exchange rate, reserves and imports are also added to the GDP, inflation, and interest rates to ensure that it is comparable to the official market specification. Nevertheless, the theoretical factors imply that these variables have a lesser impact in parallel markets because of a low level of regulation, controllable trading, and speculative forces prevail in setting prices. This inclusion can be empirically tested to test the expected attenuated effect. The model structure can be used to ensure consistency across markets as well as assess the importance of traditional flow-model fundamentals to the parallel market by having the full variable set retained.

Parallel exchange rate data were thoroughly tested to have reliable parallel data in the empirical analysis. A variety of sources were used in the collection of observations, such as the State Bank of Pakistan, commercial banks and reliable reports on the financial market, which allowed to cross-verify the values reported. Any difference in the sources was explored and resolved, and there was less chance of reporting errors. Although some discrepancies of informal market data are inevitable, the triangulation approach offers a strong representation of the parallel exchange market in Pakistan. This approach enhances the belief that the ARDL estimation is accurate to represent the economic conditions and not measurement artifacts.

3.3. Econometric Model

In spite of the fact that the same macroeconomic variables have been used in the official model and parallel exchange rate models to offer an analytical comparability, there are varying effects expected in different markets because of institutional segmentation. The main policy-relevant instruments that are used by the official foreign exchange window are the foreign reserves and imports, which mainly rely on the intervention of central banks, as well as the trade financing mechanism. Contrastingly, the variables of policy control are not very strong, as the rates of the parallel exchanges are mostly set by the individual demand for foreign currency, expectations, and liquidity situations. Thus, weaker or insignificant reserves and trade-related coefficients are expected in the parallel market instead of post-estimation anomalies. Moreover, the same lag structure is also carried over to both models in order to preserve similarity in dynamic comparison and prevent over-parameterization due to the small sample size. Dissimilarity in market behaviour is thus represented by the magnitude of the coefficient, its significance, and speed of adjustment as opposed to varying lag lengths.

Official Exchange Rate:

Long-Run Equation:

OEXR_t = α0 + Σα1 ln(GDP_{t-i}) + Σα2 INF_{t-i} + Σα3 INT_{t-i} + Σα4 CAB_{t-i} + Σα5 ln(RES_{t-i}) + Σα6 ln(IMP_{t-i}) + ε_t

Error Correction Model (ECM / Short-Run Equation)

ΔOEXR_t = α0 + Σα1 Δln(GDP_{t-i}) + Σα2 ΔINF_{t-i} + Σα3 ΔINT_{t-i} + Σα4 ΔCAB_{t-i} + Σα5 Δln(RES_{t-i}) + Σα6 Δln(IMP_{t-i}) + λ ECM_{t-1} + ν_t

Parallel Exchange Rate:

Long-Run Equation:

PEXR_t = γ0 + Σγ1 ln(GDP_{t-i}) + Σγ2 INF_{t-i} + Σγ3 INT_{t-i} + Σγ4 CAB_{t-i} + Σγ5 ln(RES_{t-i}) + Σγ6 ln(IMP_{t-i}) + μ_t

Error Correction Model (ECM / Short-Run Equation):

ΔPEXR_t = δ0 + Σδ1 Δln(GDP_{t-i}) + Σδ2 ΔINF_{t-i} + Σδ3 ΔINT_{t-i} + Σδ4 ΔCAB_{t-i} + Σδ5 Δln(RES_{t-i}) + Σδ6 Δln(IMP_{t-i}) + φ ECM_{t-1} + ω_t

All the variables in the study were categorized as nominal or real depending on the economic interpretation. Exchange rate, interest rates and inflation were measured in nominal terms, which portrayed market values observed, but the GDP, imports and reserves have been transformed to real terms by means of price deflators to eradicate the impact of inflation over the years. This difference guaranteed that the ARDL model did not reflect a distortion of the economic relationship due to the fluctuation in price levels. Output and trade variables expressed in real values are associated with the theoretical interest in long-run fundamentals, and nominal variables include the effects of the monetary and policy-driven short-run variations.

3.4. Data Analysis

As indicated by (Kripfganz & Schneider, 2023), the Autoregressive Distributed Lag (ARDL) method is used in the analysis of data. ARDL is especially appropriate since it has an acceptable ability to accommodate variables integrated at various orders, I (0) or I (1), without necessarily pre-testing the existence of homogeneous stationarity- this is a major strength in volatile emerging-market time series. Also, ARDL models are applied to estimate long-run cointegration and short-run error-correction relationships, as recommended by (Nasrullah et al., 2021). In general, this methodological framework guarantees the strict empirical analysis of the determinants of both official and parallel exchange rates in Pakistan, which corresponds to the aims of the study and the nature of the macroeconomic data.

4. RESULTS

4.1. Descriptive Statistics

The descriptive statistics in Table 2 show a moderate variability in both the parallel and official exchange rates, with slightly different means (107.21 and 107.10) and standard deviations (70.77 and 70.82). This indicates a high exchange rate variation in the 30-year period, which is in accordance with the frequent macroeconomic turmoil in Pakistan. The mean of inflation (9.76%) is moderate with a substantial range (SD = 5.05), which implies the existence of some relative stability and expensive inflationary situations. Interest rates are also very volatile (mean = 6.69%; SD = 5.75), reflecting the changing monetary policy reactions to the shocks in the economy. The balance of the current account has a negative mean (-7.01) but with wide variations (SD = 6.52), which indicates continuous external sector strains. Reserves (mean = 9.98; SD = 0.37) and imports (mean = 10.51; SD = 0.29), on the other hand, are less varied because of the ln-transformation and reflect consistent increasing patterns. The GDP (mean = 25.95; SD = 0.60), where GDP shows relatively lower variability compared with exchange rate and inflation variables due to the logarithmic transformation. In general, the statistics show a macroeconomic situation with a high exchange rate and inflationary volatility.

Table 2. Descriptive statistics.

| Variable | Mean | SD | Min | Max |

| Parallel Exchange Rate (USD/PKR) | 107.21 | 70.77 | 36.08 | 280.36 |

| Official Exchange Rate (USD/PKR) | 107.1 | 70.82 | 36.42 | 282.51 |

| Inflation (CPI, %) | 9.76 | 5.05 | 2.53 | 30.77 |

| Interest Rate (%) | 6.69 | 5.75 | 0.03 | 14.54 |

| Current Account Balance (log) | -7.01 | 6.52 | -10.28 | 9.59 |

| Reserves | 9.98 | 0.37 | 9.12 | 10.36 |

| Imports | 10.51 | 0.29 | 10.03 | 10.93 |

| GDP | 25.95 | 0.6 | 24.85 | 26.65 |

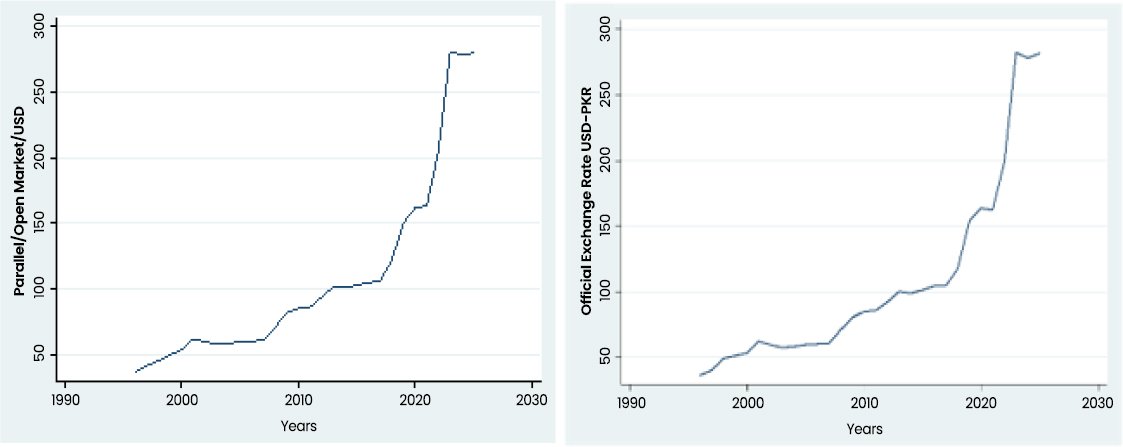

Fig. (1) elaborates the steady and upward trend in the case of official and parallel exchange rates of Pakistan, which imitates the depreciation of PKR over the long-run period. In historical terms, both of the markets stayed comparatively slow, particularly below the 60PKR/USD, till the global financial crisis of 2008, which triggered a sharp spike as a result of declining foreign exchange reserves, highlighted by (Bhurat & Thakrar, 2024) also. The secondary peak was observed around 2018-2019 when the transition from managed to market-determined exchange rate was made by the State Bank with an aim to address the developing crisis regarding the balance of payments (The News, 2025). However, the most aggressive increase occurred in 2021, with the rate enhanced to 300PKR/USD. As per (Chohan, 2025), this massive spike was driven by political instability, the devastating floods, and the delay in IMF loan approvals. Considerably, the parallel market steadily trades at a premium, visible in the further peaks in 2023, as the shortage of dollars and the reduction in imports pushed demand toward informal-parallel market channels. In overall terms, the trend depicts economic vulnerabilities and a shift to regimes of flexible exchange rates under the pressures of external debt.

Fig. (1). Trend of parallel and official exchange rates of Pakistan.

4.2. Dickey-Fuller Unit Root Test

The specified results of ADF in Table 3 indicate that the majority of the variables are non-stationary at the level, as the parallel exchange rate (p = 0.998), official exchange rate (p = 0.998), interest rate (p = 0.706), imports (p = 0.629), reserves (p = 0.102), and GDP (p = 0.315) show statistically non-significant p-values. The current account balance is the only variable that is not stationary at level (p = 0.025). Nevertheless, the stationarity of all the variables is achieved upon first differencing, with p-values greater than significance at order one, I (1). Such a pattern of mixed integration [I (1)] and stationarity [I (0)] confirms the use of the ARDL modelling framework, which is flexible to such combinations and can be used to analyse the short-run and long-run dynamics. In short, inflation and current account (log) are I (0) while the rest of the variables are I (1) and there exists no I (2) variable.

Table 3. Unit root test.

| Variable | Level (Intercept) | p-value | First Difference | p-value |

| Parallel Exchange Rate | 1.764 | 0.998 | -3.727 | 0.004 |

| Official Exchange Rate | 1.588 | 0.998 | -4.202 | 0.001 |

| Inflation (CPI) | -2.727 | 0.07 | -5.308 | 0.000 |

| Interest Rate | -1.123 | 0.706 | -3.993 | 0.002 |

| Current Account (log) | -3.116 | 0.025 | – | – |

| Reserves (log) | -2.556 | 0.102 | -5.282 | 0.000 |

| Imports (log) | -1.301 | 0.629 | -3.781 | 0.003 |

| GDP (log) | -1.936 | 0.315 | -4.034 | 0.001 |

4.3. Lag Selection Criteria

The integration of lagged variables in the ARDL framework allowed for capturing the delayed adjustments of exchange rates in association with macroeconomic shock which imitated both policy transitions and anticipations of the market (Boburmirzo & Boburjon, 2022). Lags are also allowed to address autocorrelation and inertia in monetary as well as trade flows, which guarantees that the dynamic association between parallel and official exchange rates is projected accurately during the period of time, as supported by (Rajkovic et al., 2020).

Based on Akaike Information Criterion (AIC) and Schwarz Information Criterion (SIC), the optimal model lag length of the official and parallel exchange rate ARDL models was calculated. This method guarantees a balance between model fit and parsimony so that there is less tendency to overfit and the dynamics of macroeconomic determinants are well captured. The ARDL specifications (1, 1, 1, 1, 1, 1, 1) were chosen as the lowest AIC and SIC, which substantiates that both the official and parallel exchange rate models are appropriate to select the lag structure that is suitable in estimating the short- and long-run effects.

4.4. Association Between Official Exchange Rate and Macroeconomic Indicators

The Table 4 shows results of ARDL show that it is adjusted to the short run, and the negative and significant ECM value (β = -0.2306, p = 0.005) confirms that the system returns to the long-run equilibrium aftershocks. All of the factors, including inflation (β = 10.54, p < 0.001), interest rate (β = -7.73, p =0.001), and GDP (β = 191.57, p = 0.008), have statistically significant effects on the official exchange rate, whereas current account balance, reserves, and imports do not have any significant effects. Regarding GDP, it can be read that in Pakistan, the GDP growth is mostly import-intensive, but State Bank of Pakistan reports indicate that the economic growth is boosting demand for imported energy and capital goods, and hence putting pressure on foreign exchange demand and depreciation pressure reported by (Sahar et al., 2025).

Table 4. ARDL official exchange rates and economic factors.

| Variable | Coefficient | Std. Error | t-value | p-value |

| ECM (L1. Official Exchange Rate) | –0.2306 | 0.0708 | –3.26 | 0.005 |

| Long-Run Coefficients | – | – | – | – |

| Inflation (CPI) | 10.5449 | 2.2116 | 4.77 | 0.000 |

| Interest Rate | –7.7340 | 1.8337 | –4.22 | 0.001 |

| Current Account (log) | –2.6143 | 1.6174 | –1.62 | 0.127 |

| Reserves (log) | –35.2717 | 47.0087 | –0.75 | 0.465 |

| Imports (log) | –99.2018 | 129.6237 | –0.77 | 0.456 |

| GDP (log) | 191.5668 | 63.0416 | 3.04 | 0.008 |

| Short-Run Coefficients | – | – | – | – |

| Δ Inflation | 0.3649 | 0.5923 | 0.62 | 0.547 |

| Δ Interest Rate | 2.0394 | 0.54 | 3.78 | 0.002 |

| Δ Current Account | 0.5212 | 0.3143 | 1.66 | 0.118 |

| Δ Reserves | –4.8438 | 10.4453 | –0.46 | 0.649 |

| Δ Imports | –35.3348 | 25.3967 | –1.39 | 0.184 |

| ΔGDP | –36.6177 | 17.4352 | –2.10 | 0.053 |

| Constant | –807.1227 | 157.8249 | –5.11 | 0.000 |

| Model Summary | – | – | – | – |

| R-squared | 0.9657 | |||

| Adjusted R-squared | 0.936 | |||

| t-statistic (ECM) | –3.26 | |||

Note: *** indicates significance at 1%, ** indicates significance at 5%, *indicates significance at 10%

The demand and supply of interest rates are involved in the short-run dynamics of the official exchange rate, not monetary dominance. In particular, changes in interest rates have a substantial effect on the rate (β = 2.04, p = 0.002), and so do shocks in the output as represented by the GDP (β = -36.62, p = 0.053). This implies that monetary variables affected by the policy, as well as real-sector variations, combine to cause short-term changes in the exchange rate, with the interventions of the Central Bank and the influence of macroeconomic output pressures on the official exchange rate in Pakistan. The large value of R-squared (0.966) indicates that it has strong explanatory power and shows that there is a valid long-run relationship. Generally, the model reveals that the exchange rate in Pakistan is highly sensitive to macro-economic fundamentals, especially inflation and monetary conditions, both in the short and long term.

The official exchange rate ARDL results are understood by clearly distinguishing between the long-run equilibrium relationships and the adjustment in the short-run in accordance with exchange rate theory. Based on the long-run estimates, GDP, which is an import-intensive growth, has a significant impact on the official exchange rate, as it increases foreign exchange demand. Import and current account deficits are, however, statistically insignificant, indicating that the trade flow and balances do not have a direct measurable impact under the managed exchange rate regime in Pakistan.

As such, the findings are consistent, as expected, that output causes demand for foreign currency, but the insignificance of other variables in the flow model shows that it is not possible to empirically confirm the Traditional Flow Model in this situation. Monetary and policy-driven adjustments in the short run are reflected in short-run dynamics, especially by way of interest rate adjustments that are in line with the Monetary Approach. However, these short-run effects are dampened by the interventions of the central banks and output shocks, which lead to a slow compensation of fundamentals.

4.5. Bound Test

The bounds test in Table 5, validates that there exists a stable long-run relationship between the official exchange rate and the macroeconomic determinants. The calculated F-statistic of (16.204) is greater than the upper critical values of (10), 5% and 1% significance levels, which reject the null hypothesis of no cointegration. This finding suggests that inflation, interest rates, GDP, and the external balances, reserves, and imports co-move with the official exchange rate in the long run. Therefore, the long-run equilibrium dynamics are confirmed in the case of Pakistan.

Table 5. Bound test-official exchange rates and economic determinants.

| Model | k | n | F-statistic | 10% Critical Value | 5% Critical Value | 1% Critical Value | |||

| – | – | – | – | I (0) | I (1) | I (0) | I (1) | I (0) | I (1) |

| ARDL | 5 | 29 | 16.204*** | 2.506 | 4.019 | 3.111 | 4.888 | 4.693 | 7.136 |

4.6. Robustness Check using VECM Analysis for the Official Exchange Rate

It has been tested after omitting the stationary variable.

The results of VECM in Table 6 validates the existence of a stable long-term association among the variables, consistent with the Johansen cointegration test. GDP, inflation and interest rates are found as statistically significant macroeconomic determinants of the official exchange rate, which also reinforces the findings of ARDL. While imports are found to be statistically insignificant. Although the reserves were found to be significant, their impacts differ from ARDL results, which suggests sensitivity to the choice of model. The error correction term is positively, though weakly significant, which implies gradual and likely unstable adjustment towards equilibrium. Generally, the consistency in major macroeconomic variables within the ARDL and VECM models provides the robustness of the primary conclusions of the study.

Table 6. Vector error correction model-official exchange rate.

| Vector Error Correction Model (VECM) Results for Official Exchange Rate (Robustness Check) | ||||

| Variable | Coefficient (β) | Std. Error | z-value | p-value |

| Inflation (CPI) | 24.957*** | 4.866 | 5.13 | 0.000 |

| Interest Rate | 20.536*** | 4.554 | 4.51 | 0.000 |

| Reserves (log) | -1135.937*** | 116.883 | -9.72 | 0.000 |

| Imports (log) | -437.989 | 346.037 | -1.27 | 0.206 |

| GDP (log) | 758.039*** | 164.186 | 4.62 | 0.000 |

| Error Correction Term (ECM) | 0.037 | 0.021 | 1.8 | 0.072 |

Note: ** p < .01, ** p < .05, VECM estimated as a robustness check using Johansen cointegration approach

4.7. Association between Parallel Exchange Rate and Macroeconomic Indicators

Even though the parallel market ARDL model in Table 7 reserves, and imports have a weaker expected impact, as the central bank interventions are lower, and because it is more dependent on liquidity, speculation, and short-term expectations, the expectation is substantiated by the results of the estimation since these coefficients are statistically insignificant, which shows the less significant role of external-sector variables in parallel market dynamics. These variables are included to be comparable with the actual market to make a direct conclusion between markets and empirically test the fact that macroeconomic fundamentals such as GDP, inflation, and interest rates control the short-run and long-run adjustments in the parallel exchange rate.

Table 7. ARDL parallel exchange rates and economic factors.

| Variable | Coefficient | Std. Error | t-value | p-value |

| ECM (L1. Parallel Rate) | -0.2382*** | 0.0651 | -3.66 | 0.002 |

| Long-Run Coefficients | – | – | – | – |

| Inflation (CPI) | 10.3535*** | 1.9016 | 5.44 | 0.000 |

| Interest Rate | -7.0875*** | 1.489 | -4.76 | 0.000 |

| Current Account (log) | -2.0023 | 1.3585 | -1.47 | 0.161 |

| Reserves (log) | -56.1863 | 42.0261 | -1.34 | 0.201 |

| Imports (log) | -81.3542 | 109.5838 | -0.74 | 0.469 |

| GDP (log) | 190.217*** | 53.6853 | 3.54 | 0.003 |

| Short-Run Coefficients | – | – | – | – |

| Δ Inflation | 0.0818 | 0.5207 | 0.16 | 0.877 |

| Δ Interest Rate | 1.2835** | 0.468 | 2.74 | 0.015 |

| Δ Current Account | 0.283 | 0.2756 | 1.03 | 0.321 |

| Δ Reserves | -0.0827 | 9.1316 | -0.01 | 0.993 |

| Δ Imports | -14.7839 | 22.1376 | -0.67 | 0.514 |

| Δ GDP | -37.1700** | 15.4074 | -2.41 | 0.029 |

| Constant | -820.6762*** | 146.6397 | -5.60 | 0.000 |

| Model Summary | – | – | – | – |

| R-squared | 0.9693 | – | – | – |

| Adjusted R-squared | 0.9426 | – | – | – |

| T-statistic (ECM) | -3.66 | – | – | – |

Note: *** indicates significance at 1%, ** indicates significance at 5%

The ARDL estimates shows in Table 7 that parallel market adjustment is not demonstrably faster given annual frequency as ECM (β = -0.2382, p =.002), which implies that it is stable and has relatively similar convergence to the long-run equilibrium of the parallel exchange rate as found in the official exchange rate’s case.

The coefficients of the long run are that the parallel market rate is sensitive to the macroeconomic fundamentals because it is heavily dependent on the inflation (β = 10.35, p <.001), interest rates (β = -7.09, p <.001), and GDP (β = 190.22, p = .003). Balances of the current account, reserve, and imports are not statistically significant. The changes in the interest rate (β = -1.27, p = 0.015) and output modifications (β = -37.17, p = 0.029) are the drivers of the short-run dynamics of the parallel exchange rate, but not purely monetary factors. Other aspects, such as reserves and imports, do not have any significant short-term impacts.

This implies that the parallel market is highly responsive to real-sector factors and policy indicators, a factor that demonstrates that it is market-driven in the dual exchange rate system in Pakistan. The value of R-squared (0.969) indicates a strong predictive power and signifies the validity of a long-run relationship. On the other hand, in the short run, both interest rates (β = 1.2835, p = 0.015) and GDP (β = -37.1700, p = 0.029) significantly impact parallel exchange rates, which depicts that the parallel exchange rate is dependent on both monetary policies and vulnerable to output volatilities. On the whole, macroeconomic forces are powerful in motivating the parallel exchange rate behaviors of Pakistan.

The ARDL outcomes of the parallel exchange rate show that an adjustment process is mainly predetermined by market-driven forces and a lack of regulatory control. Short-run dynamics are stronger and are more consistent with the Monetary Approach and output shocks because variations in the interest rates and output-related expectations are immediately reflected in parallel market prices.

Conversely, the long-run parameters do not support the Traditional Flow Model strongly, as imports, reserves, and the current account are found to be statistically insignificant, and this indicates the insignificance of formal trade channels in this market. GDP reflects a wider demand pressure of the import-intensive growth and informal foreign exchange transactions. Nevertheless, there is a hypothesis of possible structural asymmetry, which theory raises, although the study finds the coefficients of the major economic determinants similar in both markets, and no formal asymmetry is evidenced between the two markets.

4.8. Bound Test

Table 8 shows the results of the bounds test for parallel exchange rates, exhibits that there exists a strong long-run cointegrating correlation between the parallel exchange rate and its macroeconomic factors. The F-ratio of (19.963) significantly surpasses the upper significance levels of the 10%, 5% and 1% critical levels, so that it is possible to reject the null hypothesis that there is no cointegration. This validates the fact that in the long run, inflation, interest rates, GDP, and external-sector variables are concomitantly related to the parallel exchange rate in Pakistan.

Table 8. Bound test-parallel exchange rates and economic determinants.

| Model | k | n | F-statistic | 10% Critical Value | 5% Critical Value | 1% Critical Value | |||

| – | – | – | – | I (0) | I (1) | I (0) | I (1) | I (0) | I (1) |

| ARDL | 5 | 29 | 19.963*** | 2.506 | 4.019 | 3.111 | 4.888 | 4.693 | 7.136 |

4.9. Robustness Check using VECM for Parallel Exchange Rate

It has been tested after omitting the stationary variable.

The results of VECM, as depicted in Table 9 specifies statistically significant relationship between macroeconomic and parallel exchange rate in the long run, as also depicted by ARDL. This validates cointegration within the Johansen framework. As indicated, inflation and interest rates were found to be highly significant, which also highlighted the role of monetary situations that shape the dynamics of parallel exchange rates. GDP was also found to be significant, which indicated that real-sector activity leads to movements in parallel exchange rates in the long-run. While the imports and reserves are found to be statistically significant, their near-zero standard errors and magnitudes signify restricted practical pertinence irrespective of statistical significance. The positive as well as significant error term (0.324, p < .01) also depicts divergence instead of convergence, which implies unstable dynamics of exchange rate adjustments. These findings highlight limitations in apprehending restoration of equilibrium while using yearly data and provisions interpreting results of VECM as evidence of robustness instead of primary extrapolation.

Table 9. Vector error correction model-parallel exchange rate.

| Vector Error Correction Model (VECM) Results for Parallel Exchange Rate (Robustness Check) | ||||

| Variable | Coefficient (β) | Std. Error | z-value | p-value |

| Inflation (CPI) | 10.762*** | 0.752 | −14.31 | 0.000 |

| Interest Rate | 4.029*** | 0.571 | −7.06 | 0.000 |

| Reserves | -2.8032*** | 0.00 | 5.03 | 0.000 |

| Imports | -2.7041*** | 0.00 | 8.53 | 0.000 |

| GDP | 2.6578*** | 0.00 | −10.95 | 0.000 |

| Error Correction Term (ECM) | 0.324*** | 0.083 | 3.9 | 0.000 |

Note: ** p < .01, ** p < .05, VECM estimated as a robustness check using Johansen cointegration approach

4.10. Comparison Between Determinants of Official and Parallel Exchange Rates

Table 10 clearly indicates that the common significant determinants are inflation, interest rate, and GDP on both official and parallel exchange rates, whereas current account, reserves, and imports have no statistically significant impact in both markets.

Table 10. Comparison between determinants of official and parallel exchange rates.

| S. No. | Determinant | Official Exchange Rate | Parallel Exchange Rate |

| 1 | Inflation (CPI) | Yes | Yes |

| 2 | Interest Rate (%) | Yes | Yes |

| 3 | Current Account | No | No |

| 4 | Reserves | No | No |

| 5 | Imports | No | No |

| 6 | GDP | Yes | Yes |

4.11. Relation Between Official and Parallel Exchange Rates

As depicted in Table 11, the ARDL findings suggest that the official exchange rate and parallel exchange rate have a strong long-term correlation, and the long-run coefficient of parallel exchange rate as represented by the official exchange rate is positive with a significant value (β = 1.0006, p <.001) indicating that the parallel market adjusts on a one-to-one basis to the change in the official exchange rate. Nevertheless, the short-run coefficient is not significant (β = -0.028, p = .911), which means that short-term changes in the official rate do not have a direct effect on the parallel rate. Excellent predictive power of the model is evidenced by a high R-squared (0.9838).

Table 11. Relationship between the two exchange rates.

| Variable | Coefficient | Std. Error | t | p-value |

| Parallel Open Market USD (L1) | -1.0125*** | 0.2692 | -3.76 | 0.001 |

| Long Run (LR) | – | – | – | – |

| Official Exchange Rate USD/PKR | 1.0006*** | 0.0067 | 149.41 | 0.000 |

| Short Run (SR) | – | – | – | – |

| Δ Official Exchange Rate USD/PKR (D1) | -0.028 | 0.2485 | -0.11 | 0.911 |

| Constant (_cons) | 0.2026 | 0.7595 | 0.27 | 0.792 |

| Model Statistics | – | – | – | – |

| R-squared | 0.9838 | |||

| Adjusted R-squared | 0.9818 | |||

| Root MSE | 2.1538 | |||

Note: *** indicates significance at 1%, ** indicates significance at 5%, *indicates significance at 10%

5. DISCUSSION

The findings of the study are effective in terms of providing crucial evidence about the determinants of official and parallel exchange rates in Pakistan and how the two markets are connected. In this instance of the official exchange rate, as the study indicates, the macroeconomic variables like inflation, interest rates, and GDP have a high level of influence, as is the case with other developing economies. This trend is in line with Pakistan-specific data indicating that GDP growth cycles are systematic in expanding the trade deficit and in surging foreign exchange demand because of import reliance, as reported by (Ahmed, 2024).

Similar revelations were made by (Wasiu et al., 2019) in the context of Nigeria, who also found that official exchange rates were largely affected by GDP, inflation, and interest rates. Such similarity is explainable by the structural features of the two markets, where home prices, output, as well as monetary policies have a very strong effect on currency values, which is argued by (Malec et al., 2024; Turna & Özcan, 2021) as well. The notable influence of inflation and interest rates also follows the Monetary Approach, which means that the macroeconomic policy and monetary management have a direct influence on the official exchange rate of Pakistan, which supports the essence of controlling prices at a domestic level, as well as the liquidity management to stabilize currency prices.

The results of the study, though significant, could be affected by possible econometric constraints such as the use of ARDL modelling, which, though it is able to deal with mixed orders of integration, could still be unable to fully capture high-frequency speculative stocks that are characteristic of the parallel market in Pakistan. However, the findings present vital clues to the greater arguments in economic policies, namely that there should be concerted macro-economic policies. In particular, the regulation of inflation and interest rates cannot be out of place with the Monetary Approach, which emphasizes the contribution of monetary and fiscal policies to stabilize the official exchange rate.

These results highlight the role played by the policy interventions that could focus on liquidity, price stability, and confidence in the market together to enhance the dual-market currency system in Pakistan. Institutional and economic factors have been the main determinants of the official exchange rate, and these include monetary and fiscal policy, foreign currency inflows, and regulatory interventions. These basic determinants- GDP, imports, and BoP are recorded in annual data, not speculative fluctuations. Therefore, the variations in long-run coefficients are of macroeconomic fundamentals and adjustments as well as of the policy effects based on stability, not on arbitrage market behaviour.

The factors that significantly impact the parallel exchange rate are similar to those of the official one, as the factors that play a major role in these two markets are inflation, interest rates, and GDP. Other macroeconomic variables, including reserves and imports, are insignificant, which means that both the markets react to the same set of macroeconomic fundamentals and not to a structural divergence. Even though the hypothetical viewpoint indicates that the parallel market can be more vulnerable to liquidity conditions, inflation expectations, and speculative pressures suggested by (Olamide et al., 2022; and Phuc & Duc, 2021), the empirical data in the given study do not support the asymmetry. There are similarities in the coefficients of the official and parallel exchange rate models, indicating similar sensitivities to macroeconomic shocks.

The data of the annual accounts represent the long-run economic foundations, which do not allow tracking speculative changes in the short term, and fast market-specific responses are not subject to empirical confirmation. Therefore, all propositions about structural distinctions in the markets are hypothetical and not proven in practice. The differences in weight of the coefficients are not substantial, and it is important to note that there is an anchoring of the two markets around the same fundamental variables in the economy. Regulatory oversight, market segmentation, and controlled intervention in Pakistan dampen short-term divergences, indicating that the perceived asymmetry is not statistically significant but is an anthropomorphic attribute of market behaviour.

The results support the theoretical hypothesis that the reserves and imports have a weak impact on the parallel exchange rate and the official exchange rate markets in Pakistan. Both markets are found to be more responsive to the activity of the real sector, the money situation, and speculative pressure. The fact that reserves and imports are statistically insignificant supports this assumption and outlines structural symmetries among markets. Having these variables in the model enables an official determination of the relevance of these variables, establishing that the parallel market and official exchange rate markets work on a market-driven basis, not a policy-influenced external-sector fundamentals basis.

Comparisons to other regions are also used to represent contextual differences. According to the Asia-Pacific region, (Phuc & Duc, 2021) and Southern Africa, (Olamide et al., 2022), the most important ones were the inflation rates and interest rates but the magnitude of the effect varied based on the institutional structures and the openness of the trade. One instance is that, the pass-through of higher exchange rate between Japan and Korea is similar to that of Pakistan, which possesses policy initiatives and market stratification that limits the real-time communication of macroeconomic shocks to currency values revealed by (Inyang et al., 2023) as well. In the same breath, the same relationship (inversion) between interest rates and exchange rate in Pakistan is part of the global picture and it shows success of monetary policy to stabilize the official values of currencies.

Despite the fact that the ARDL approach takes the long-run and short-run dynamics into consideration, there is a potential econometric limitation to the model particularly on the full capturing of high-frequency speculative dynamics and instant liquidity shocks which is apparent in the parallel market in Pakistan. Despite these shortcomings, the findings provide valuable insights to the overall discourse on the economic policy. Another key finding that is highlighted by the results is that parallel exchange rate and official exchange rate are more sensitive to key economic variables, including GDP, interest rates, and inflation, and are not significantly influenced by reserves, BoP, and imports.

This is the dilemma of the policymakers to regulate the official market at a particular time when spillovers in the parallel market are anticipated but delayed. Moreover, the responsiveness of the parallel market to inflation and GDP experienced is also in line with the global evidence regarding exchange rate pass-through in alignment of macroeconomic and trade policies. The policymakers must therefore balance between financial stability, dealing in imports and market confidence in an effort to ensure that any activity on the official market can be felt in the parallel market without occasioning a high degree of volatility.

There is strong association between the official and parallel exchange rate in the long run, an indication of institutional anchoring. The short-run transmission of official rate changes to the parallel market is limited by annual data, capital controls and market segmentation. Though, the parallel market is gradually impacted by the movement of the official market, it is cushioned by the regulatory measures, the foreign exchange regulations, and the speculative trading, as it has also been pointed out by (Sahar et al., 2025). It is in line with the available data in Nigeria (Wasiu et al., 2019), yet the situation is more challenging in Pakistan because institutional constraints are even higher. The fact that the short-term relationship has weakened is one of the indicators that the parallel market, despite being largely market driven, is indirectly affected by policy driven official realignment of rates over time, an interpretation of the law-of-one-price perspective of convergence. This underscores the relevance of the structural and institutional variables in the determination of long-term alignment of the exchange rates.

The results clearly endorse the theory-based differentiation in terms of variables, horizons, and markets in the dual exchange rate system in Pakistan. According to the Traditional Flow Model, all three have an effect: GDP, imports, and the balance of payments in the long run. They have slow adjustments in production and trade that fix the official exchange rate under regulatory supervision; however, due to the insignificance of BoP and imports in both models, the Flow model could not be validated. On the other hand, the Monetary Approach describes the reason why the short-run dynamics are dominated by inflation and interest rates since monetary shocks and monetary expectations are easily spread into the parallel market. Differences in coefficients between markets occur due to the fact that the official rate is controlled by the policies and changes gradually, whereas the parallel rate is market-based and reacts to the liquidity conditions and speculative pressure.

In addition, the COVID-19 pandemic upset the global and domestic macroeconomic positions, generating a significant impact on the exchange rates and the main indicators inflation, output, and trade balances. In Pakistan, as (Djalo et al., 2023) unveiled, interruptions in the supply chain caused by the pandemic and a drop in export revenues increased the strain on foreign reserves, which increased the volatility of the exchange rate. Similarly, the results of the present research indicate that both official and parallel rates reacted to these shocks by being more sensitive to variations in the interest rate and GDP, which are quick adaptations in the demand for foreign currency under limited liquidity. This is in accordance with the evidence across the world that uncertainty propagated by the pandemic aggravated short-term monetary transmission and restricted the stabilizing effect of reserves (Gajurel, 2022). Therefore, COVID-19 supports the significance of taking external shocks into consideration when analyzing dual-market exchange rate models.

The similarities and differences witnessed can be attributed to several factors that involve the economy and the structure. The high degree of import dependence, combined with persistent current account deficits, makes both markets sensitive to GDP and inflation in Pakistan, unlike resource-exporting economies like Nigeria or more diversified Asian economies. Short-term volatility is further propelled by political instability, energy crisis, and external debt pressures, which inhibit the short-term effectiveness of the policies in the parallel market. Also, the use of remittances and foreign inflows increases the contribution of the GDP and domestic output in determining the currency demand, which explains the significant impact of these variables on the two markets.

CONCLUSION

The study offers empirical data on macroeconomic factors of both the official exchange rates and the parallel exchange rates in the dual foreign exchange market in Pakistan. This implies that the most significant factors that influence the exchange rate movements in both markets are inflation, interest rates and GDP, whereas reserves, imports and current account balances have a relatively small role. The results also indicate that the relationship between the official and parallel exchange rates is significantly long-run, indicating that both markets are pegged by the same macroeconomic fundamentals, but the short-run adjustments can vary because of the regulatory restrictions and market division. Instead of stating that there is a strong structural asymmetry, it is the evidence of this study shows that sensitivities are broadly similar among markets in the framework of annual data available. Both exchange rates in the framework of the Pakistani reliance on imports, external financing pressures, and continuing macroeconomic imbalances seem to be especially receptive to domestic monetary and output-related shocks. The research is an addition to the existing body of literature since it provides renewed empirical evidence for the country of Pakistan using a single framework that concurrently analyses the determinants of the official and parallel exchange rates over a long period of time. The findings provide policy implications in terms of exchange rate stability in order to minimize endemic market segmentation.

POLICY IMPLICATIONS

The findings of the research give valuable policy facts in the management of the monetary and exchange rate in Pakistan. The sensitivity of the official to inflation as well as interest rates and GDP, which indicates that the fundamental macroeconomic factors should be stabilized to ensure that the exchange rates are as less as possible. They should pay attention to good fiscal and monetary policies, which would maintain the inflation within reach and the investor confidence. The money can also be stabilized further by adding foreign reserves and controlling imports in a wise manner and narrowing the gap between the official and parallel markets. In addition, the reduction of the speculative pressures can be also achieved with the help of improved monitoring of the parallel market and specific intervention. Such policies can also lead to improvement in the external sector, increase the rate of investment, and ensure sustainable economic growth in the environment of Pakistan. Besides this, the findings have practical implications on the policymakers in Pakistan as they inform them on the macroeconomic variables that exert the greatest effect on the official and parallel exchange rates. One such instance is the fact that it is recognized that both markets are largely influenced by inflation, interest rates, and GDP, so that interventions in the monetary and fiscal policies are possible to stabilize the official rate. In addition, output and inflation sensitivity of the parallel market give regulators the ability to make market-specific policies, such as liquidity management, eliminating strains in the speculative market, and increasing the inflows of foreign currency to close the official-parallel gap and achieve the macroeconomic stability in general.

LIMITATIONS & FUTURE DIRECTION

The research is limited by the fact that it is based on secondary time-series data, which does not consider informal market processes or off-the-record money flows in Pakistan. The 30-year long-run is quite extensive and can ignore structural breaks or policy shocks occurring during the exchange rates. Another limitation of this study is that the sample size is relatively limited because of the usage of the annual data from 1996-2025. Although annual frequency is suitable in the analysis of macroeconomic fundamentals, the small sample size diminishes the statistical power and limits the capacity to measure short-term market changes or structural changes.

The ARDL methodology is based on the assumption that the relationships are linear and may miss non-linearities or asymmetric rebalancing of currency markets. Further studies might include adding high-frequency data, exploring behavioural and speculative dynamics affecting the parallel market, and using nonlinear or machine learning models to model complex dynamics. Further comparative research in other emerging economies would put the exchange rate behaviour and policy implications of Pakistan into perspective.

LIST OF ABBREVIATIONS

| AIC | = | Akaike Information Criterion |

| ARDL | = | Autoregressive Distributed Lag |

| IMF | = | International Financial Statistics |

| IRP | = | Interest Rate Parity |

| PPP | = | Purchasing Power Parity |

| SBP | = | State Bank of Pakistan |

| SIC | = | Schwarz Information Criterion |

AUTHOR’S CONTRIBUTION

W.R. and I.A.B. has contributed to the study concept, data collection, analysis, manuscript writing, data collection, writing, and proofreading.

ETHICAL APPROVAL & INFORMED CONSENT

Not applicable.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [W.R. and I.A.B.]

FUNDING

None.

CONFLICT OF INTEREST

The author declares that there is no conflict of interest regarding the publication of this article.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the authors utilized ChatGPT for language editing and refinement purposes. Following the use of this tool, the authors carefully reviewed and revised the content where necessary and accept full responsibility for the final published version of the article.

REFERENCES

Ahmed, N. (2024). Volatility Assessment of Pakistani Exchange Rupee Against World Renowned Currencies Using GARCH Models. Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online), 3(2), 209-235. https://doi.org/10.60087/jklst.vol3.n2.p235.

Ankit, R. (2023). Delinking ‘the two rupees’: The devaluation dilemma and economic divergence in the decolonized subcontinent, September 1949–February 1951. Modern Asian Studies, 57(3), 918-939.

https://doi.org/10.1017/S0026749X22000336.

Azeem, S., Shafqat, M. M., Munir, Y., & Sarwar, U. (2025). Impact of ICT Diffusion on Economic Growth: Exploring the Moderating Role of Financial Inclusion in E7 Countries. Journal of Asian Development Studies, 14(3), 1339-1354. https://doi.org/10.1016/j.actpsy.2025.105991.

Bhurat, C., & Thakrar, H. (2024). Exchange Rate Determinants and Forecasting for USD/INR: Historical Analysis and Insights.African Journal of Accounting, Economics, Finance and Banking Research, 17(17). https://dx.doi.org/10.2139/ssrn.5155597.

Boburmirzo, K., & Boburjon, T. (2022). Exchange rate influence on foreign direct investment: empirical evidence from CIS countries. International Journal of Management and Economics Fundamental, 2(04), 19-28. https://doi.org/10.37547/ijmef/Volume02Issue04-04.

Chohan, U. W. (2025). Forecasts for the Pakistani Economy in 2025.Available at SSRN 5110284. https://dx.doi.org/10.2139/ssrn.5110284.

Damayanti, C. R., & Darmawan, A. (2024). Exchange Rate, Inflation, Interest Rate and Economic Growth: How They Interact in ASEAN. Profit: Jurnal Administrasi Bisnis, 18(2), 245-256. https://doi.org/10.21776/ub.profit.2024.018.02.8.

Djalo, M. U., Yusuf, M., & Pudjowati, J. (2023). The Impact of Foreign Debt on Export and Import Values, the Rupiah Exchange Rate, and the Inflation Rate. Jurnal Ekonomi, 12(01), 1124-1132. Available from: https://ejournal.seaninstitute.or.id/index.php/Ekonomi/article/view/1328.

Ebrahim, S. A., Poshtan, J., Jamali, S. M., & Ebrahim, N. A. (2020). Quantitative and qualitative analysis of time-series classification using deep learning. IEEE Access, 8, 90202-90215.

https://doi.org/10.1109/ACCESS.2020.2993538.

Ektiarnanti, R., Rahmawati, A., Fauziah, F. K., & Rofiqoh, I. I. (2023). Indonesian trade balance performance by GDP, exports, imports, BI rate and inflation as intervening variables. Indonesian Economic Review, 3(1), 1-11. https://doi.org/10.53787/iconev.v3i1.16.

Farooq, F. (2023). Economy of Pakistan: in the context of inflation, money supply and exchange rate. Journal of Law and Social Sciences-University of Turbat, 1(2), 65-77.

FoEh, J., Suryani, N. K., & Silpama, S. (2020). The influence of inflation level, exchange rate and gross domestic product on foreign direct investment in the ASEAN countries from 2007-2018. European Journal of Business and Management Research, 5(3). https://doi.org/10.24018/ejbmr.2020.5.3.311.

Gajurel, R. P. (2022). Determinants of Nepal’s foreign exchange reserve: An empirical study. Journal of Management, 5(1), 76-98. https://doi.org/10.3126/jom.v5i1.47763.

Gulzar, S., Sarwar, U., Sattar, S., Usman, M., & Quibtia, M. (2024). Tax Audit, Tax Penalty, Religiosity and Tax Compliance. Journal of Asian Development Studies, 13(3), 776-79. https://doi.org/10.62345/jads.2024.13.3.64.

Hatmanu, M., Cautisanu, C., & Ifrim, M. (2020). The impact of interest rate, exchange rate and European business climate on economic growth in Romania: An ARDL approach with structural breaks. Sustainability, 12(7), 2798. https://doi.org/10.3390/su12072798.

Hossain, M. S., Voumik, L. C., Ahmed, T. T., Alam, M. B., & Tasmim, Z. (2024). Impact of geopolitical risk, GDP, inflation, interest rate, and trade openness on foreign direct investment: Evidence from five Southeast Asian countries. Regional Sustainability, 5(4), 100177.

https://doi.org/10.1016/j.regsus.2024.100177.

Huawei, T. (2022). Do gross domestic product, inflation, total investment, and exchange rate matter in natural resources commodity prices volatility. Resources Policy, 79, 103013. https://doi.org/10.1016/j.resourpol.2022.103013.

Inyang, E. J., Etuk, E. H., Nafo, N. M., & Da-Wariboko, Y. A. (2023). Time Series Intervention Modelling Based on ESM and ARIMA Models: Daily Pakistan Rupee/Nigerian Naira Exchange Rate. Asian Journal of Probability and Statistics, 25(3), 1-17.

https://doi.org/10.9734/ajpas/2023/v25i3560.

Jamil, M. N., Rasheed, A., Maqbool, A., & Mukhtar, Z. (2023). Cross-cultural study of the macro variables and their impact on exchange rate regimes. Future Business Journal, 9(1), 9. https://doi.org/10.1186/s43093-023-00189-1.

Jihadi, M., Safitri, I. H., & Brahmawati, D. (2021). The Effect of exchange rates towards stock return mediated with inflation rates and interest rates. Jurnal reviu akuntansi dan keuangan, 11(2), 383-392.

https://doi.org/10.22219/jrak.v11i2.16320.

Kalu, E. U., Ugwu, O. E., Ndubuaku, V. C., & Ifeanyi, O. P. (2019). Exchange rate and foreign reserves interface: Empirical evidence from Nigeria. The Economics and Finance Letters, 6(1), 1-8.

https://doi.org/10.18488/journal.29.2019.61.1.8.

Karamelikli, H., & Karimi, M. S. (2022). Asymmetric relationship between interest rates and exchange rates: Evidence from Turkey. International Journal of Finance & Economics, 27(1), 1269-1279.

https://doi.org/10.1002/ijfe.2213.

Khalid, W., Iqbal, J., Nasir, N., & Nosheen, M. (2024). Do real exchange rate misalignments have threshold effects on economic growth? Asymmetric evidence from Pakistan. Economic Change and Restructuring, 57(6), 181.

https://doi.org/10.1007/s10644-024-09752-4.

Kripfganz, S., & Schneider, D. C. (2023). ardl: Estimating autoregressive distributed lag and equilibrium correction models. The Stata Journal, 23(4), 983-1019. https://doi.org/10.1177/1536867X231212434.

Lee, Y., & Yoon, S. M. (2020). Relationship between international reserves and FX rate movements. Sustainability, 12(17), 6961. https://doi.org/10.3390/su12176961.

Malec, K., Maitah, M., Rojik, S., Aragaw, A., & Fulnečková, P. R. (2024). Inflation, exchange rate, and economic growth in Ethiopia: A time series analysis. International Review of Economics & Finance, 96, 103561. https://doi.org/10.1016/j.iref.2024.103561.

Maqsood, N., Shahid, T. A., Amir, H., & Bilal, K. (2023). Symmetric impact of Trade, exchange rate, and inflation rate on Stock Market in Pakistan: New evidence from Macroeconomic variables. Bulletin of Business and Economics (BBE), 12(3), 903-911.

https://doi.org/10.61506/01.00292.

Müller, K., Xu, C., Lehbib, M., & Chen, Z. (2025). The global macro database: A New International Macroeconomic Dataset (No. w33714). National Bureau of Economic Research. https://dx.doi.org/10.2139/ssrn.5121271.

Nasrullah, M., Rizwanullah, M., Yu, X., Jo, H., Sohail, M. T., & Liang, L. (2021). Autoregressive distributed lag (ARDL) approach to study the impact of climate change and other factors on rice production in South Korea. Journal of Water and Climate Change, 12(6), 2256-2270. https://doi.org/10.2166/wcc.2021.030.

News, M. (2025). PKR stays flat at 281.25 per USD, Mettis Global Link – Pakistan Economy News, Forex & Finance Updates. Mettis Global Link. Available from: https://mettisglobal.news/PKR-stays-flat-at-28125-per-USD-55734 (Accessed: 11 December 2025).

Nurjanah, R., & Mustika, C. (2021). The influence of imports, foreign exchange reserves, external debt, and interest rates on the currency exchange rates against the United States Dollar in Southeast Asia Countries. Jurnal Perspektif Pembiayaan Dan Pembangunan Daerah, 9(4), 365-374. https://doi.org/10.22437/ppd.v9i4.12706.

Olamide, E., Ogujiuba, K., & Maredza, A. (2022). Exchange rate volatility, inflation and economic growth in developing countries: Panel data approach for SADC. Economies, 10(3), 67.

https://doi.org/10.3390/economies10030067.

Phuc, N. V., & Duc, V. H. (2021). Macroeconomics determinants of exchange rate pass-through: new evidence from the Asia-Pacific region. Emerging Markets Finance and Trade, 57(1), 5-20.

https://doi.org/10.1080/1540496X.2018.1534682.

Rajković, M., Bjelić, P., Jaćimović, D., & Verbič, M. (2020). The impact of the exchange rate on the foreign trade imbalance during the economic crisis in the new EU member states and the Western Balkan countries. Economic research-Ekonomska istraživanja, 33(1), 182-203. https://doi.org/10.1080/1331677X.2019.1708771.