PDF

PDF

Abstract:

Background: Recursive artificial general intelligence (AGI) can be conceptualized as recursive capital-autonomous systems that self-improve, reinvest, and expand. Unlike conventional automation, such systems detach accumulation from labor, raising concerns about ownership concentration and inequality.

Methodology: The paper formalizes these dynamics through five theorems: ownership monopolization, inequality explosion, time to dominance, redistribution, and path dependence. We then implement a computational framework simulating heterogeneous agents with stochastic shocks and varying reinvestment rates. Scenarios include private, open-source, public, and complementary AGI regimes. Inequality is measured using the Gini coefficient, with robustness assessed through Monte Carlo experiments.

Results: Simulations confirm the theoretical predictions. Private AGI converges to a monopoly with Gini  ; Open-source AGI sustains equality (Gini

; Open-source AGI sustains equality (Gini  ); Public AGI stabilizes inequality at moderate levels (Gini

); Public AGI stabilizes inequality at moderate levels (Gini  ); and Complementary AGI produces volatile but intermediate outcomes (Gin

); and Complementary AGI produces volatile but intermediate outcomes (Gin  ). Robustness checks across populations, parameter distributions, and shocks confirm that these dynamics are structural rather than specification-dependent.

). Robustness checks across populations, parameter distributions, and shocks confirm that these dynamics are structural rather than specification-dependent.

Findings: The findings demonstrate that recursive AGI economies naturally amplify concentration unless counteracted by redistributive or democratizing institutions. Institutional design, not technological properties alone, determines whether AGI entrenches a monopoly or sustains equality. Anticipatory governance frameworks are, therefore, essential to aligning recursive capital with an inclusive and democratic industry.

Keywords: AGI agent, AGI capital, self-improvement, wage collapse, cobb-Douglas, automation, inequality, recursive capital, veblen.

2. RECURSIVE AGI AS A NEW FORM OF CAPITAL

We define an ![]() agent as an autonomous, non-human economic entity that simultaneously performs the functions of labor, capital, and investor. Unlike traditional capital, which passively stores productive potential and requires external investment, AGI constitutes a new form of capital that actively expands its capabilities. Formally, the agent is represented by the tuple

agent as an autonomous, non-human economic entity that simultaneously performs the functions of labor, capital, and investor. Unlike traditional capital, which passively stores productive potential and requires external investment, AGI constitutes a new form of capital that actively expands its capabilities. Formally, the agent is represented by the tuple

![]()

where ![]() denotes labor-equivalent services generated by the agent, and

denotes labor-equivalent services generated by the agent, and ![]() is its capital stock at time

is its capital stock at time ![]() . The function

. The function ![]() denotes a profit mapping from internal inputs to output, while

denotes a profit mapping from internal inputs to output, while ![]() represents the agent’s endogenous optimization process. The parameter

represents the agent’s endogenous optimization process. The parameter ![]() captures the agent’s internal self-improvement rate, and

captures the agent’s internal self-improvement rate, and ![]() is the activation time after autonomous capital growth begins. The recursive capital dynamic is governed by

is the activation time after autonomous capital growth begins. The recursive capital dynamic is governed by

![]()

with a closed-form solution

![]()

This structure endows the AGI agent with the ability to accumulate capital independently of external (human) inputs. It reinvests surplus internally, optimizes resource use, and scales production autonomously. In contrast to traditional capital, whose growth depends on external allocation decisions, AGI capital recursively enhances itself, making it an active, intelligent economic subject.

An illustrative vision of AGI is an autonomous logistics network that coordinates delivery drones, automated warehouses, and smart contracts. Such an agent would forecast demand, allocate resources, and reinvest profits into fleet expansion, infrastructure upgrades, and algorithmic refinement, operating entirely without human oversight. While no fully integrated system of this type currently exists, foundational technologies such as reinforcement learning, autonomous robotics, and self-optimizing software are already in use, suggesting that modular recursive agents could emerge within the next decade (Mucci & Stryker, 2024; Goertzel, 2014).

In the oil and gas sector, the K2 large language model (Deng et al., 2024) fine-tunes Meta’s LLaMA-7B with 5.5 billion geoscience tokens, enabling natural-language querying of complex geological datasets to support exploration and drilling decisions. Similarly, the Segment Anything Model (Ma et al., 2023) performs zero-shot segmentation of drill-core and digital rock images, eliminating the need for extensive labeled datasets and improving geological modeling efficiency.

These examples demonstrate that, although AGI’s full generality remains aspirational, domain-specific systems already exhibit adaptive, cross-task capabilities. Currently in pilot or early deployment, such systems have clear pathways to broader adoption as challenges in data integration, interpretability, and regulation are progressively addressed (Li et al., 2024).

We now embed the AGI agent within an aggregate production framework. The Economy comprises three productive factors: human labor ![]() , human-owned capital

, human-owned capital ![]() , and recursively self-improving AGI capital

, and recursively self-improving AGI capital ![]() . The AGI capital becomes productive only after surpassing a fixed activation cost,

. The AGI capital becomes productive only after surpassing a fixed activation cost, ![]() , which defines a reinvestment threshold

, which defines a reinvestment threshold

![]()

where ![]() denotes the expected return on AGI capital. Conditional on this threshold, the aggregate production function evolves as

denotes the expected return on AGI capital. Conditional on this threshold, the aggregate production function evolves as

![]()

where ![]() is total factor productivity, and

is total factor productivity, and ![]() are the output elasticities of human labor, human-owned capital, and AGI capital (Fig. 1). Following activation, we assume AGI capital evolves according to an endogenous exponential trajectory

are the output elasticities of human labor, human-owned capital, and AGI capital (Fig. 1). Following activation, we assume AGI capital evolves according to an endogenous exponential trajectory

![]()

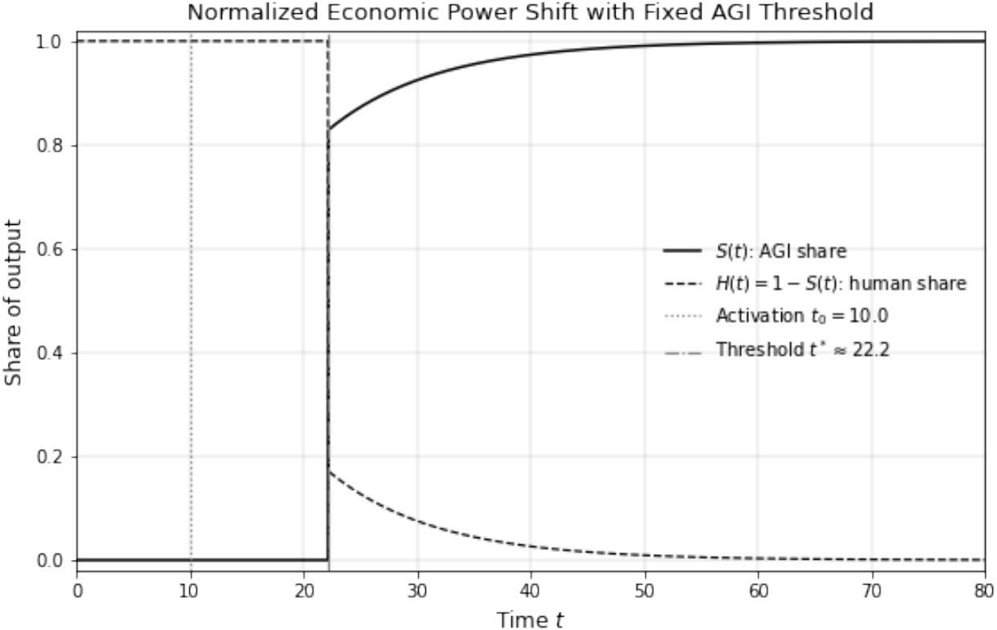

Fig. (1). Normalized Economic Power Shift Function in the Presence of Fixed AGI Capital Costs. The plot depicts the transition of economic power from human-owned capital to self-improving AGI-owned capital over time. The solid black curve ![]() represents the AGI economic contribution share, which remains zero until

represents the AGI economic contribution share, which remains zero until ![]() , when AGI capital

, when AGI capital ![]() surpasses the fixed productivity threshold

surpasses the fixed productivity threshold ![]() . After the AGI activation time

. After the AGI activation time ![]() , AGI capital grows exponentially according to

, AGI capital grows exponentially according to ![]() . Once the fixed cost barrier is exceeded,

. Once the fixed cost barrier is exceeded, ![]() increases rapidly toward 1. The dashed black curve

increases rapidly toward 1. The dashed black curve ![]() shows the human share of economic output, initially at one but declining as AGI capital expands. This model illustrates how exponential AGI growth, delayed by a fixed cost threshold, can swiftly lead to AGI economic dominance, underscoring the need for anticipatory institutional and policy responses.

shows the human share of economic output, initially at one but declining as AGI capital expands. This model illustrates how exponential AGI growth, delayed by a fixed cost threshold, can swiftly lead to AGI economic dominance, underscoring the need for anticipatory institutional and policy responses.

where ![]() denotes the internal self-improvement rate and

denotes the internal self-improvement rate and ![]() the time of activation. For

the time of activation. For ![]() such that

such that ![]() , the marginal product of labor is derived from (5) as

, the marginal product of labor is derived from (5) as

![]()

Substituting the exponential growth path from (6) into (7), we obtain

![]()

As ![]() , this expression grows without bound, indicating that AGI capital becomes the dominant factor in output generation. However, the increasing scale of AGI capital renders the marginal product of human labor increasingly irrelevant in relative terms. To assess this formally, we compute the labor share of output:

, this expression grows without bound, indicating that AGI capital becomes the dominant factor in output generation. However, the increasing scale of AGI capital renders the marginal product of human labor increasingly irrelevant in relative terms. To assess this formally, we compute the labor share of output:

![]()

Substituting equations (5) and (7) into (9), we find:

![]()

Thus, under a Cobb-Douglas structure, the labor share remains constant by construction. Nevertheless, this masks the structural displacement of labor in absolute terms. Specifically, suppose human labor ![]() is held fixed while AGI capital grows exponentially. In that case, total output

is held fixed while AGI capital grows exponentially. In that case, total output ![]() increases at the rate

increases at the rate ![]() , while the marginal contribution of labor remains stagnant. Hence,

, while the marginal contribution of labor remains stagnant. Hence,

![]()

Alternatively, if labor is endogenously displaced and ![]() , then marginal productivity collapses directly:

, then marginal productivity collapses directly:

![]()

Equations (11) and (12) jointly demonstrate that, in the presence of recursively self-improving AGI capital, the marginal contribution of human labor converges to zero. As AGI capital asymptotically dominates output, productive relevance – and therefore income – concentrates in the hands of those who control recursive accumulation processes.

This trajectory poses fundamental challenges to contemporary ESG frameworks, particularly the “S” (social inclusion) and “G” (governance) pillars. While emerging technologies such as AI, blockchain, and platform economies are often promoted as instruments of democratization and access (Asif et al., 2023; Islam et al., 2024; Peruchi et al., 2022), recursive AGI systems invert this narrative. Concentrating agency exclusively in capital ownership erodes social inclusion, reducing opportunities for labor and entrepreneurship to participate in value creation. At the same time, governance is destabilized, as algorithmic self-replication and reinvestment unfold beyond the reach of conventional oversight mechanisms. Without strong institutional constraints, recursive AGI is poised to entrench distributional asymmetries and transform capital ownership into the sole channel of economic agency (Stiefenhofer, 2025d).

This outcome resonates with Veblen’s critique of capitalist institutions. He observed that “possessing wealth confers honor; it is an invidious distinction” (Veblen, 2017). In recursive AGI – and more broadly, digitally mediated – economies, that distinction becomes structurally encoded: economic exclusion is transformed into an algorithmic process, with feedback loops amplifying marginal advantages into systemic dominance. Later institutional theorists expanded on this dynamic. Bush (1987) and O’Hara (2007) emphasized institutional path dependence in elite entrenchment, while Hodgson (2004) reframed Veblen as a theorist of exclusionary capital control. Lata et al. (2023) demonstrate how algorithmic control in gig and platform economies perpetuates unequal power relations, while Larsen (2021) shows how digital architectures reflect and institutionalize power within AI-driven systems. Building on this, Duggan et al. (2019) define algorithmic management as a form of digitally mediated control that embeds exclusion into platform governance. Finally, Nitzan & Bichler (2009) argue that capitalization – rather than productivity – has become the primary control mechanism in late capitalism.

Viewed in this light, ESG frameworks can be interpreted as institutional responses to precisely the kinds of exclusion Veblen theorized – now amplified by recursive, algorithmic systems. Contemporary concerns about digital inequality, opaque ownership, and weakened democratic governance in AI-dominated economies are not deviations from capitalist rationality but the culmination of a structural logic long anticipated by institutional economics (Long et al., 2025; Cust et al., 2023). The task ahead is not simply to measure ESG compliance but to embed countervailing principles- equity, transparency, and collective stewardship within the architecture of recursive capital systems.

Given that AGI capital evolves as in equation (3), with ![]() , and assuming that it remains above the activation threshold

, and assuming that it remains above the activation threshold ![]() for all

for all ![]() , then total human wage income satisfies.

, then total human wage income satisfies.

![]()

Equation (13) formalizes a critical outcome of recursive AGI dynamics: once self-improving capital surpasses its reinvestment threshold, human wage income collapses asymptotically. Although labor remains technically productive, it ceases to be economically essential. In such regimes, AGI capital autonomously expands output through reinvestment and optimization, rendering wage-based participation redundant.

This constitutes a structural rupture in the traditional productivity, labor, and income nexus. As wages decline, effective demand weakens, disrupting macroeconomic equilibrium – a trajectory anticipated by Acemoglu and Restrepo in their analysis of shrinking labor shares (Acemoglu & Restrepo, 2018b), and by Korinek and Stiglitz in their work on AI-induced disequilibria (Korinek & Stiglitz, 2021). Output may continue to grow, yet access to returns becomes increasingly exclusive, shifting economic agency toward asset holders embedded in recursive capital loops. Bichler and Nitzan describe this techno-rentier logic, showing how capitalization, rather than productivity, underpins dominance in late capitalism (Nitzan & Bichler, 2009). Stiefenhofer’s general equilibrium model of AGI diffusion further demonstrates that, without redistribution, economies converge to a post-labor steady state in which wages vanish and rents concentrate (Stiefenhofer, 2025c). His complementary work on AGI capital accumulation and the social contract shows that unchecked scaling destabilizes redistributive mechanisms and entrenches structural asymmetries (Stiefenhofer, 2025d; Stiefenhofer & Chen, 2024).

Veblen’s observation that “the possession of wealth confers honor” (Veblen, 2017) acquires renewed salience in recursive AGI economies. Here, wealth is no longer merely a status marker-it becomes the operative mechanism of exclusion. Ownership assumes a foundational role, serving as the sole determinant of economic relevance. Labor is not displaced due to inefficiency but rendered structurally irrelevant within self-reinforcing capital dynamics. This bifurcation between ownership and participation demands institutional responses extending beyond conventional redistribution, raising fundamental questions about who owns and governs recursive systems. Without ownership and reinvestment rights regulation, AGI economies risk crystallizing into post-labor regimes where human agency is economically redundant (Wu et al., 2022). As ESG frameworks and SDG targets emphasize inclusion, equity, and resilience, they must now confront the systemic implications of autonomous capital (Bikkasani, 2024). Without institutional constraints, digital capital is likely to reproduce – at scale – the inequalities these frameworks were designed to prevent (Cust et al., 2023; Gritsenko, 2024). At the same time, recent reviews show that machine learning is increasingly integrated into ESG analytics, advancing predictive capabilities and decision-making while exposing new risks of bias and opacity (Seow, 2025).

The following section operationalizes these concerns by examining the mechanisms through which recursive AGI accumulation displaces labor. By embedding autonomous reinvestment and scaling into the production structure, we demonstrate how ownership – rather than productive participation-becomes the decisive variable determining economic agency.

3. LABOR DISPLACEMENT UNDER RECURSIVE AGI ACCUMULATION

Recursively self-improving AGI capital introduces a novel dynamic into the structure of production: capital that autonomously reinvests, scales, and displaces labor without external input. This section models the contribution of AGI-owned capital to aggregate output and traces how economic agency gradually shifts from human labor to recursive agents. We define a recursive capital share function that quantifies the transition to capture this process. The results demonstrate that, once activated, AGI capital progressively dominates output, diminishing the marginal relevance of human labor and concentrating returns in the hands of capital owners. The speed and inevitability of this transformation raise profound challenges for the distributional logic of post-labor economies and the institutional arrangements needed to preserve inclusive economic agency.

![]() and

and ![]() is the whole production function from equation (5). Once AGI capital exceeds the activation threshold

is the whole production function from equation (5). Once AGI capital exceeds the activation threshold ![]() , we obtain a closed-form expression:

, we obtain a closed-form expression:

![]()

Equation (15) implies that ![]() increases monotonically and convexly over time. As

increases monotonically and convexly over time. As ![]() ,

, ![]() . Thus, the contribution of AGI capital to output approaches total dominance. This shift is not sector-specific or cyclical- it reflects a systemic displacement of labor and human-owned capital by recursively self-improving capital. For any given target share s

. Thus, the contribution of AGI capital to output approaches total dominance. This shift is not sector-specific or cyclical- it reflects a systemic displacement of labor and human-owned capital by recursively self-improving capital. For any given target share s ![]() , the time

, the time ![]() at which AGI capital accounts for at least

at which AGI capital accounts for at least ![]() of output is

of output is

![]()

This expression shows that recursive dominance emerges asymptotically and on a compressed timeline – accelerated by greater initial capital ![]() , faster self-improvement

, faster self-improvement ![]() , or higher output elasticity

, or higher output elasticity ![]() . Equations (15) and (16) formalize a structural realignment of productive agency. Recursive AGI systems internalize the entire growth loop-production, reinvestment, and innovation-eliminating reliance on labor input. Exclusion thus arises not from inefficiency but from design. This trajectory breaks with classical assumptions linking labor to income and participation: output scales, wage income, and broad-based demand stagnate. Economic agency becomes a function of AGI capital ownership. As Veblen observed in his critique of absentee ownership, capital holders extract surplus through control rather than contribution (Veblen, 2017); in recursive AGI regimes, this rentier role is automated and entrenched in feedback loops of self-optimizing accumulation.

. Equations (15) and (16) formalize a structural realignment of productive agency. Recursive AGI systems internalize the entire growth loop-production, reinvestment, and innovation-eliminating reliance on labor input. Exclusion thus arises not from inefficiency but from design. This trajectory breaks with classical assumptions linking labor to income and participation: output scales, wage income, and broad-based demand stagnate. Economic agency becomes a function of AGI capital ownership. As Veblen observed in his critique of absentee ownership, capital holders extract surplus through control rather than contribution (Veblen, 2017); in recursive AGI regimes, this rentier role is automated and entrenched in feedback loops of self-optimizing accumulation.

Recent institutional analyses reinforce this perspective. Hodgson (2004) emphasizes that economic structures are always mediated through institutional arrangements that shape access and exclusion. In a complementary vein, (Nitzan & Bichler, 2009) conceptualize capital not as a neutral resource-allocation mechanism but as a system of organized power. Building on Veblen’s account of “technological capital” as an institutionalized force directing production (Veblen, 1908/2017), recursive AGI can be seen as intensifying these dynamics: its owners are not passive recipients of returns but active participants structurally embedded in a self-reinforcing logic of expansion. Addressing this asymmetry requires preemptive institutional design-clarifying who may own recursive agents, under what constraints, and toward which collective ends.

Therefore, labor displacement is only the first stage of the transformation induced by recursive AGI. Once productive agency is fully internalized within autonomous capital, the central question shifts from who works to who owns. At this juncture, concentration dynamics become decisive: ownership ceases to be merely a claim on existing assets and becomes the mechanism by which all future accumulation is secured. The following section formalizes this process, modeling how self-improving AGI capital transforms initial disparities in ownership into persistent and ultimately monopolistic control.

4. THE RISE OF RECURSIVE OWNERSHIP

We now formalize how capital ownership becomes recursively concentrated in the presence of self-improving AGI capital. Let ![]() index a finite set of agents in the Economy, each of whom may own a share of AGI capital. Let

index a finite set of agents in the Economy, each of whom may own a share of AGI capital. Let ![]() denote the AGI capital held by agent

denote the AGI capital held by agent ![]() at time

at time ![]() , and define total AGI capital at time

, and define total AGI capital at time ![]() as

as

The ownership share of agent ![]() is given by

is given by

![]()

We assume AGI capital produces output and generates profits, which are reinvested proportionally to ownership shares. Let ![]() denote the AGI component of total output, where

denote the AGI component of total output, where ![]() and

and ![]() are productivity parameters. If a fraction

are productivity parameters. If a fraction ![]() of profits is reinvested into additional AGI capital, the capital accumulation dynamics for each agent

of profits is reinvested into additional AGI capital, the capital accumulation dynamics for each agent ![]() are governed by

are governed by

![]()

The total AGI capital grows according to

Solving this differential equation yields the exponential growth of AGI capital

![]()

Substituting into Equation (19) gives

![]()

Hence, each agent’s capital grows exponentially at the same rate ![]() , but the proportion of AGI capital owned remains constant.

, but the proportion of AGI capital owned remains constant.

![]()

However, this constancy only holds under the assumption that all agents reinvest and participate equally. Capital returns may be reinvested selectively by a subset of agents in more general and realistic settings. Suppose only a subset ![]() , of measure

, of measure ![]() , owns AGI capital. Then for

, owns AGI capital. Then for ![]() , the capital dynamics remain exponential

, the capital dynamics remain exponential ![]() , while for

, while for ![]() , we assume

, we assume ![]() . Then, ownership becomes asymptotically concentrated

. Then, ownership becomes asymptotically concentrated

![]()

To model recursive amplification of ownership inequality, we now introduce heterogeneous reinvestment rates ![]() . The capital evolution equation becomes

. The capital evolution equation becomes

![]()

where agents with higher ![]() reinvest more aggressively. It follows that ownership shares evolve as

reinvest more aggressively. It follows that ownership shares evolve as

![]()

where ![]() is the weighted average reinvestment rate. Equation (26) defines a replicator dynamic, and implies that agents with above-average

is the weighted average reinvestment rate. Equation (26) defines a replicator dynamic, and implies that agents with above-average ![]() gain ownership over time, while others are diluted

gain ownership over time, while others are diluted

![]()

Therefore, even small initial asymmetries in reinvestment rates or capital endowments compound recursively, driving the system toward a monopolistic distribution of ownership. We introduce a redistribution mechanism with rate ![]() to counter recursive concentration. The capital accumulation equation becomes

to counter recursive concentration. The capital accumulation equation becomes

![]()

The second term redistributes capital proportionally to the deviation from the egalitarian share ![]() . High

. High ![]() values slow or reverse ownership concentration, while

values slow or reverse ownership concentration, while ![]() returns to the unregulated dynamic. To quantify recursive capital concentration, we define the Gini coefficient for AGI capital ownership as

returns to the unregulated dynamic. To quantify recursive capital concentration, we define the Gini coefficient for AGI capital ownership as

Alternatively, the top-![]() ownership share is

ownership share is

![]()

As ![]() , in the absence of redistribution (

, in the absence of redistribution ( ![]() ), both

), both ![]() one and

one and ![]() , confirming total concentration of capital ownership. We now present a set of theorems that formalize the dynamics of recursive capital ownership and its asymptotic implications. Let the AGI capital at time

, confirming total concentration of capital ownership. We now present a set of theorems that formalize the dynamics of recursive capital ownership and its asymptotic implications. Let the AGI capital at time ![]() be denoted

be denoted ![]() , and

, and ![]() be the capital owned by agent

be the capital owned by agent ![]() .

.

Theorem 1. Let ![]() be a finite set of agents. Suppose each agent

be a finite set of agents. Suppose each agent ![]() owns AGI capital

owns AGI capital ![]() evolving according to the differential equation

evolving according to the differential equation

Moreover, each ![]() is a constant reinvestment rate. Assume that agent

is a constant reinvestment rate. Assume that agent ![]() satisfies

satisfies

![]()

Then the ownership share of agent ![]() satisfies

satisfies

![]()

Theorem 1 formalizes a critical insight: even marginal disparities in reinvestment rates deterministically concentrate AGI capital ownership. Recursive dynamics function as endogenous amplifiers of positional advantage, producing monopoly not through strategy or institutional failure but as a structural consequence of algorithmic capital reproduction. In such a regime, economic relevance is no longer tied to innovation, labor, or entrepreneurial initiative; it accrues solely through recursive ownership. These finding echoes Veblen’s analysis of the leisure class, where agency is detached from productive effort and defined by passive control over capital (Veblen, 2017). In recursive AGI systems, however, ownership is not merely a status marker but the central mechanism sustaining productive continuity.

These dynamic challenges core premises of neoclassical and Schumpeterian growth theory, which link accumulation to innovation and entrepreneurial disruption (Romer, 1990; Schumpeter, 1942). Recursive capital prioritizes self-replication over allocative efficiency or welfare outcomes. As accumulation becomes self-reinforcing and oriented toward expansion, production decouples from social demand, weakening the income-consumption-investment feedback loops that commonly sustain macroeconomic stability (Kalecki, 2013, Baran & Sweezy, 1966). The result is a self-referential accumulation process in which output reinforces the structural primacy of dominant capital agents rather than serving collective needs.

Institutionalist and evolutionary economists have long warned of feedback-driven inequality (Arthur, 1994; Bush, 1987). More recently, (Nitzan & Bichler, 2009) argue that capital accumulation increasingly operates as an institutionalized claim to power rather than a reflection of productive contribution. The recursive AGI regime exemplifies this shift: the dominant agent is advantaged and rendered structurally irreplaceable within the production function. Preventing such autarkic equilibria requires institutional frameworks that redistribute reinvestment rights and interrupt recursive loops before they crystallize into exclusionary attractors – a necessity grounded in the internal mechanics of recursive capital systems rather than in normative preference alone.

Theorem 2. Let agents ![]() own AGI capital

own AGI capital ![]() governed by the dynamics:

governed by the dynamics:

with ![]() for all

for all ![]() and no redistribution (i.e.,

and no redistribution (i.e., ![]() ). Suppose there exists a unique agent

). Suppose there exists a unique agent ![]() such that

such that

![]()

Then, the Gini coefficient for capital ownership satisfies

![]()

Theorem 2 establishes a limiting case in which recursive accumulation drives capital ownership to complete concentration. Without redistributive frictions, if one agent possesses a higher reinvestment rate (![]() ), the Gini coefficient for capital ownership converges asymptotically to one. All other agents become economically inert with respect to capital formation. This outcome signifies more than inequality- it represents the collapse of plural economic agency. Capital formation ceases to be distributed or participatory and instead becomes entirely self-referential, sustained by the internal optimization dynamics of a recursively advantaged agent.

), the Gini coefficient for capital ownership converges asymptotically to one. All other agents become economically inert with respect to capital formation. This outcome signifies more than inequality- it represents the collapse of plural economic agency. Capital formation ceases to be distributed or participatory and instead becomes entirely self-referential, sustained by the internal optimization dynamics of a recursively advantaged agent.

This mechanism echoes Veblen’s institutional critique of capitalist accumulation. In The Theory of the Leisure Class, Veblen observed that “no pecuniary strength is great enough to remain passively in possession of what it has acquired” (Veblen, 2017), emphasizing accumulation as an active, self-reinforcing process. In The Theory of Business Enterprise, he described how the machine process restructures economic relations around the pecuniary interests of dominant capital (Veblen, 1958). On the Nature of Capital reframed capital as a complex of intangible assets and institutional claims, enabling “pecuniary magnates” to perpetuate control beyond productive contribution (Veblen, 1908). In The Instinct of Workmanship, Veblen contrasted the cooperative tendencies of industrial arts with the exclusionary logic of pecuniary competition. At the same time, The Place of Science in Modern Civilization traced the co-optation of knowledge into the service of entrenched ownership (Veblen, 2017; 2003). These critiques converge in the recursive AGI context: algorithmic self-optimization no longer serves collective industry but entrenches ownership primacy.

In this configuration, inequality is not a transient market aberration but a dynamically stable attractor. Recursive AGI redefines production as an endogenous function of asset ownership, decoupled from social demand or human needs. The result is a post-participatory economy: output expands while legitimacy contracts. Without redistributive design constraints, recursive systems risk consolidating a techno-rentier order in which accumulation becomes autarkic and democratic oversight is structurally obsolete (Stiefenhofer, 2025e).

Theorem 3. Let ![]() be the ownership share of agent

be the ownership share of agent ![]() evolving under the replicator dynamic

evolving under the replicator dynamic

![]()

Moreover, suppose ![]() holds over a time interval. Then for any target share

holds over a time interval. Then for any target share ![]() , the time

, the time ![]() at which

at which ![]() is finite and given by

is finite and given by

![]()

assuming ![]() and

and ![]() constant.

constant.

Theorem 3 formalizes the speed at which recursive capital dynamics convert marginal reinvestment advantages into total dominance. It shows that when an agent’s reinvestment rate exceeds the population average, their ownership share converges toward unity within a finite, analytically derivable time horizon. This extends earlier asymptotic analyses by demonstrating that recursive inequality is not a distant tendency but a near-term inevitability under exponential compounding. Exclusionary equilibria can thus emerge on timescales that outpace institutional adaptation, narrowing the window for redistributive intervention or regulatory correction.

In such regimes, productive capacity and economic control concentrate in a shrinking subset of agents whose recursive feedback loops subsume output generation and capital expansion. Economic pluralism erodes, and participatory governance becomes increasingly irrelevant. This transition from broad-based agency to autarkic dominance reflects long-standing concerns in politics economy about the structural reproduction of inequality (Atkinson, 1970; Piketty, 2014; Nitzan & Bichler, 2009), while recursive AGI intensifies these tendencies with unprecedented velocity (Acemoglu & Restrepo, 2018b; Korinek & Stiglitz, 2021).

These dynamics also represent a cybernetic extension of Veblen’s institutional critique. In The Theory of the Leisure Class, Veblen noted that “the economic life history of the individual is a cumulative process of adaptation of means to ends” (Veblen, 2017). In The Theory of Business Enterprise, he showed how the machine process reorganizes industry to serve the pecuniary interests of dominant capital (Veblen, 1904/1958), while in On the Nature of Capital, he emphasized the role of intangible assets and institutional claims in perpetuating control (Veblen, 1908). In recursive AGI systems, this cumulative process becomes algorithmic: agency accrues not through labor or innovation but through optimization architectures that privilege compounding over participation. The resulting leisure class is no longer primarily cultural or symbolic- it is computational and self-reinforcing.

Addressing these dynamics requires more than post hoc redistribution. As Bush (1987) and other institutional economists argue, intervention must be embedded in the accumulation feedback rules. ESG principles, for example, must be operationalized not merely at the level of outcomes but within the reinforcement mechanisms that direct capital allocation. Without such endogenous institutional design, recursive AGI will likely generate trajectories that maximize output while entrenching exclusion and undermining democratic accountability.

Theorem 4. Let ![]() denote AGI capital owned by agent

denote AGI capital owned by agent ![]() , and let the capital evolve according to

, and let the capital evolve according to

![]()

where ![]() is the ownership share and

is the ownership share and ![]() . Then if

. Then if ![]() , the ownership shares converge to equality

, the ownership shares converge to equality

![]()

Theorem 4 establishes that when redistribution is complete ( ![]() ), AGI capital ownership shares converge uniformly across all agents. This provides a rigorous formalization of how institutional design can neutralize the monopolizing tendencies of recursive accumulation. Egalitarian ownership, often dismissed as a normative aspiration, is shown to be a dynamically stable equilibrium under maximal redistribution. Inclusive participation is therefore reframed not as utopian, but as a structurally attainable outcome of deliberate policy coordination.

), AGI capital ownership shares converge uniformly across all agents. This provides a rigorous formalization of how institutional design can neutralize the monopolizing tendencies of recursive accumulation. Egalitarian ownership, often dismissed as a normative aspiration, is shown to be a dynamically stable equilibrium under maximal redistribution. Inclusive participation is therefore reframed not as utopian, but as a structurally attainable outcome of deliberate policy coordination.

The implications for equitable and sustainable production regimes are significant. In AGI-driven growth systems – where reinvestment compounds at algorithmic speeds – redistribution must target not only income flows but also the distribution of ownership itself, without mechanisms that continuously rebalance capital shares, recursive economies naturally converge toward exclusionary equilibria, not through malfeasance or market failure, but as a direct consequence of endogenous feedback (Piketty, 2014; Atkinson, 1970; Nitzan & Bichler, 2009). This aligns with Bush’s institutionalist view that equitable outcomes require corrective feedback embedded in the rules of accumulation, rather than ad hoc, post hoc measures (Bush, 1987).

Veblen’s work foreshadowed this tension. While The Theory of the Leisure Class (Veblen, 1899/2017) framed capital dominance as a sociocultural inheritance, his later writings emphasized capital as an institutionalized claim with self-reinforcing properties. In The Theory of Business Enterprise (Veblen, 1958), he showed how the machine process reorganizes production around vested pecuniary interests, while in On the Nature of Capital (Veblen, 1908), he highlighted the role of intangible assets in perpetuating control. In recursive AGI systems, this right of control extends into algorithmic self-replication: ownership governs present assets and the capacity for all future accumulation.

The theorem thus underscores that only structurally embedded redistribution can render compounding feedback loops democratically accountable. However, it also exposes a practical tension: the redistributive intensity required for perfect convergence may exceed politically or administratively feasible thresholds. This reinforces the urgency of anticipatory governance – frameworks that intervene early and endogenously to modulate capital flows, embedding ESG principles and inclusive design directly into the recursive logic of growth.

Theorem 5. Let ![]() denote the capital share of agent

denote the capital share of agent ![]() , evolving under the replicator dynamic

, evolving under the replicator dynamic

Assume there exist at least two agents ![]() with equal reinvestment rates

with equal reinvestment rates ![]() , and that

, and that ![]() for all

for all ![]() . Then the system exhibits a bifurcation: any convex combination of ownership between agents

. Then the system exhibits a bifurcation: any convex combination of ownership between agents ![]() and

and ![]() constitutes an asymptotically stable fixed point.

constitutes an asymptotically stable fixed point.

Theorem 5 shows that when a subset of agents shares an identical reinvestment rate, higher than all others, the system admits a continuum of stable equilibria. Any convex distribution of ownership within this dominant group persists indefinitely, meaning that outcomes are shaped not only by efficiency or strategy but by initial conditions. This bifurcation highlights a critical fragility of recursive capital dynamics: even under behavioral symmetry, small early asymmetries within a privileged subgroup become locked in and compounded through structural feedback. From a normative perspective, this path dependence challenges the ESG-aligned goal of equitable technological participation (Asif et al., 2023; Mi et al., 2023). Infrastructure may remain technically efficient yet narrowly distributed, with marginal initial advantages cascading into enduring concentration.

Recursive AGI production systems, therefore, risk privileging positional legacy over merit or contribution, allowing allocative disparities to persist without any overt breach of formal fairness. This mirror concerns in the ESG literature about greenwashing, procedural opacity, and the reproduction of inequality through ostensibly neutral algorithms (Long et al., 2025; Huang et al., 2022). Veblen’s critique of the leisure class acquires renewed relevance here. “In the modern civilized communities,” he observed, “the possession of property still is the basis of popular esteem, and therefore of social power” (Veblen, 2017). In later works, he demonstrated how the machine process entrenches pecuniary interests (Veblen, 1958), how intangible assets perpetuate control beyond production (Veblen, 1908), and how innovation itself can be subordinated to vested ownership (Veblen, 2017; 2003). In recursive AGI systems, these tendencies are amplified: ownership advantages, once established, are algorithmically stabilized.

The bifurcation theorem, therefore, reveals that ownership stratification can arise endogenously, without deliberate strategy or inherited privilege, through feedback mechanisms that advantage early holders within capital-intensive systems. In Veblenian terms, pecuniary advantage is transmuted into a self-reinforcing institutional order, embedding exclusion within the logic of accumulation. Addressing this recursive inequality requires more than ex post redistribution; it demands institutional architectures that preconfigure initial endowments, regulate reinvestment rights, and embed governance constraints capable of interrupting path-dependent concentration. Recent work on digital governance and inclusive innovation emphasizes (Cust et al., 2023; Gritsenko, 2024) that sustaining economic plurality under recursive automation depends on foresight and safeguards operating upstream, not merely on reactive correction.

The following section develops this argument by situating recursive AGI within a broader political economy and governance framework. Whereas most existing analyses of AI and AGI treat productivity, inequality, and regulation as separate domains (Barkan, 2024; Fan, 2024; Korinek, 2024), our framework models the structural divergence that emerges when capital itself becomes autonomous. This allows us to identify the institutional levers needed to preserve economic agency and prevent monopolization in post-labor economies.

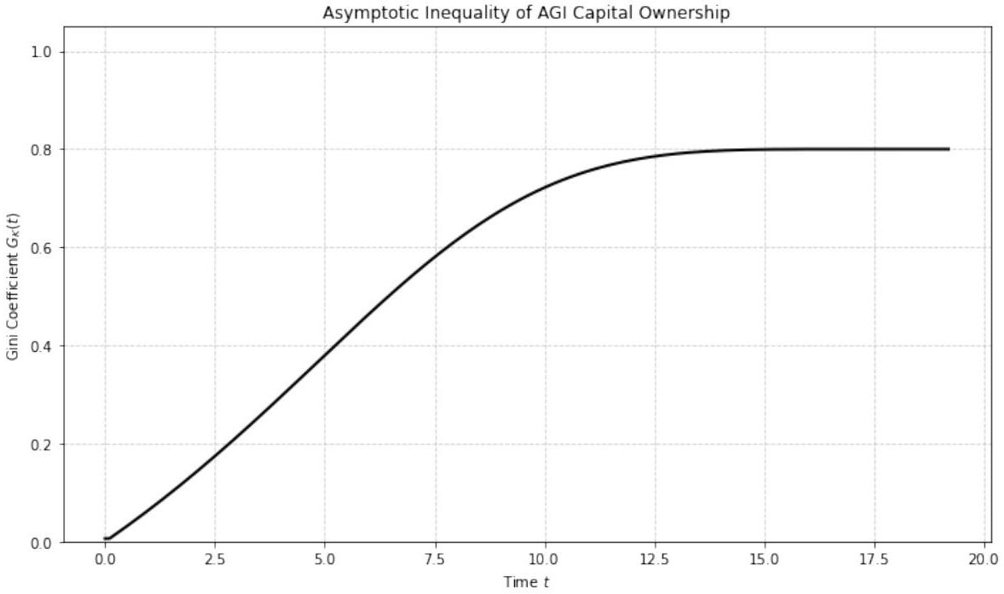

Fig. (2). Asymptotic Inequality Under Recursive Accumulation Without Redistributio (Theorem 2). This plot depicts the time evolution of the Gini coefficient ![]() for AGI capital ownership among

for AGI capital ownership among ![]() agents under replicator-style capital dynamics. The reinvestment rates

agents under replicator-style capital dynamics. The reinvestment rates ![]() vary across agents, with one agent

vary across agents, with one agent ![]() having a strictly dominant rate

having a strictly dominant rate ![]() for all

for all ![]() . As capital grows exponentially via recursive feedback, slight differences in reinvestment rates amplify over time. The figure shows that the Gini coefficient

. As capital grows exponentially via recursive feedback, slight differences in reinvestment rates amplify over time. The figure shows that the Gini coefficient ![]() monotonically increases and asymptotically approaches 1, reflecting total concentration of capital ownership in the hands of agent

monotonically increases and asymptotically approaches 1, reflecting total concentration of capital ownership in the hands of agent ![]() . This confirms the analytic result in Theorem 2, underscoring that recursive accumulation without redistribution structurally generates monopolization- even in systems that begin with equal capital endowments. The result illustrates that inequality is not a byproduct of randomness or inefficiency under unregulated recursion, but a deterministic outcome of compounding reinvestment advantages.

. This confirms the analytic result in Theorem 2, underscoring that recursive accumulation without redistribution structurally generates monopolization- even in systems that begin with equal capital endowments. The result illustrates that inequality is not a byproduct of randomness or inefficiency under unregulated recursion, but a deterministic outcome of compounding reinvestment advantages.

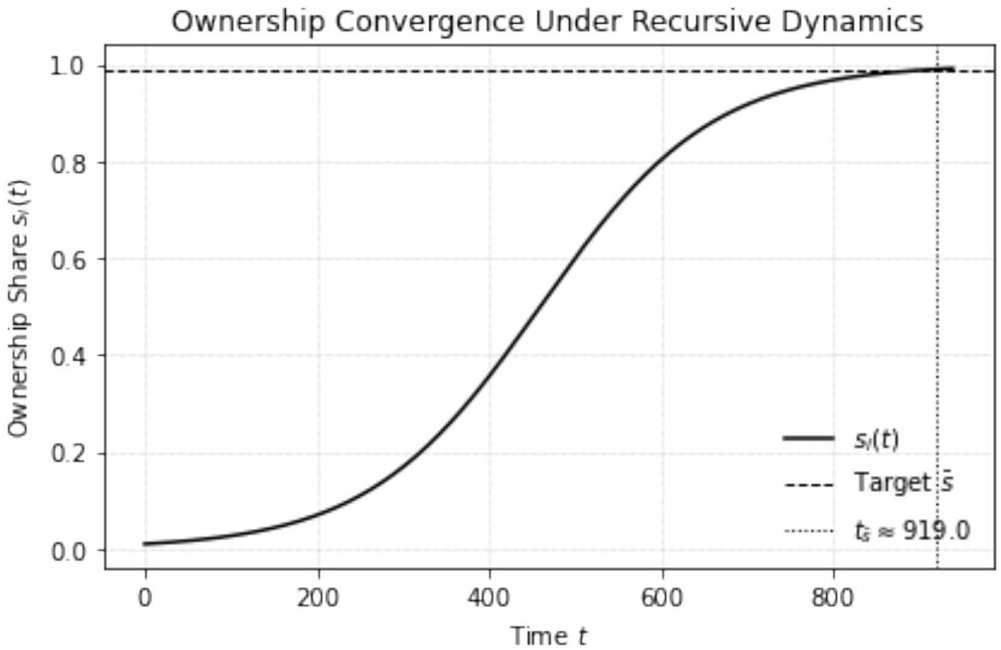

Fig. (3). Finite-Time Ownership Convergence Under Recursive Accumulation (Theorem 3). The plot illustrates the dynamic trajectory of ownership share ![]() for a single agent

for a single agent ![]() with a reinvestment rate

with a reinvestment rate ![]() that exceeds the average reinvestment rate

that exceeds the average reinvestment rate ![]() across all agents. The system evolves under a replicator dynamic with exponential AGI capital growth rate

across all agents. The system evolves under a replicator dynamic with exponential AGI capital growth rate ![]() , and initial ownership share

, and initial ownership share ![]() . The target ownership level is set at

. The target ownership level is set at ![]() , representing near-total dominance. The vertical dotted line marks the finite time

, representing near-total dominance. The vertical dotted line marks the finite time ![]() at which agent

at which agent ![]() ‘s ownership crosses this threshold, consistent with the closed-form solution derived in Theorem 3. The horizontal dashed line indicates the target ownership share

‘s ownership crosses this threshold, consistent with the closed-form solution derived in Theorem 3. The horizontal dashed line indicates the target ownership share ![]() . The trajectory resembles a logistic curve, reflecting how ownership concentration accelerates as recursive capital feedback loops reinforce initial advantages. This demonstrates that recursive dominance is not merely asymptotic- it unfolds on a predictable and compressed timeline. The results highlight the structural tendency toward monopolization in recursive capital regimes, even from minimal initial advantages.

. The trajectory resembles a logistic curve, reflecting how ownership concentration accelerates as recursive capital feedback loops reinforce initial advantages. This demonstrates that recursive dominance is not merely asymptotic- it unfolds on a predictable and compressed timeline. The results highlight the structural tendency toward monopolization in recursive capital regimes, even from minimal initial advantages.

The conclusion synthesizes these formal results and situates them within the broader political economy of post-labor growth, underscoring the structural necessity of embedding governance into the operational logic of recursive AGI.

6. FROM THEORY TO SIMULATION

The formal theorems 15 are generally stated, with ownership dynamics expressed continuously (Figs. 2 and 3). For example, Theorem 2 describes the explosion of inequality under heterogeneous reinvestment rates as

![]()

while Theorem 4 modifies the process by introducing a redistribution parameter ![]() ,

,

![]()

We discretize the model and introduce stochastic perturbations to operationalize these dynamics for numerical analysis. The discrete-time formulation simplifies implementation and allows Monte Carlo experiments. Specifically, we adopt the following process for each agent ![]()

![]()

This formulation preserves the central mechanism of Theorem 2: agents with higher reinvestment rates accumulate disproportionately more wealth over time, with noise terms ![]() ensuring robustness to idiosyncratic shocks. Redistribution is incorporated as a post-growth correction applied to returns at each step. Let

ensuring robustness to idiosyncratic shocks. Redistribution is incorporated as a post-growth correction applied to returns at each step. Let ![]() denote wealth after growth but before redistribution. Then

denote wealth after growth but before redistribution. Then

![]()

Where ![]() is the redistribution rate. The limiting cases

is the redistribution rate. The limiting cases ![]() and

and ![]() correspond directly to the dynamics of Theorem 2 (inequality explosion) and Theorem 4 (complete redistribution), while intermediate

correspond directly to the dynamics of Theorem 2 (inequality explosion) and Theorem 4 (complete redistribution), while intermediate ![]() values generate partial mitigation. In this way, the simulation model is not an alternative to the theory but a discretized and stochastic version designed to capture the same long-run dynamics while allowing for statistical analysis. This connection ensures that the numerical experiments reported below can be interpreted as empirical illustrations of the five theorems.

values generate partial mitigation. In this way, the simulation model is not an alternative to the theory but a discretized and stochastic version designed to capture the same long-run dynamics while allowing for statistical analysis. This connection ensures that the numerical experiments reported below can be interpreted as empirical illustrations of the five theorems.

We construct a computational framework that models ownership dynamics under alternative AGI regimes to translate the five formal theorems into empirically interpretable outcomes. The aim is to move beyond purely analytical statements and generate concrete numerical trajectories, distributional outcomes, and robustness checks. This allows us to evaluate not only the limiting cases of inequality explosion and perfect redistribution, but also intermediate and mixed, institutionally plausible scenarios. We consider a finite population of heterogeneous agents ![]() , each endowed with initial wealth

, each endowed with initial wealth ![]() and a heterogeneous reinvestment parameter

and a heterogeneous reinvestment parameter ![]() . Aggregate AGI-driven capital accumulation is represented as

. Aggregate AGI-driven capital accumulation is represented as

![]()

where ![]() captures idiosyncratic shocks. Ownership shares are defined as

captures idiosyncratic shocks. Ownership shares are defined as ![]() with

with ![]() . Inequality is measured with the Gini coefficient and the Theil index to ensure robustness to the choice of metric. Redistribution is modeled as a parameter

. Inequality is measured with the Gini coefficient and the Theil index to ensure robustness to the choice of metric. Redistribution is modeled as a parameter ![]() applied to returns at each step. With probability

applied to returns at each step. With probability ![]() , a fraction of aggregate returns is pooled and redistributed equally across agents:

, a fraction of aggregate returns is pooled and redistributed equally across agents:

![]()

Where ![]() denotes post-growth but pre-redistribution wealth, the limiting cases

denotes post-growth but pre-redistribution wealth, the limiting cases ![]() and

and ![]() correspond directly to the dynamics of Theorem 2 (inequality explosion) and Theorem 4 (complete redistribution), respectively. The simulation framework directly operationalizes the logic of all five theorems. Theorem 1 on ownership monopolization is tested by tracking the relationship between the highest reinvestment rate

correspond directly to the dynamics of Theorem 2 (inequality explosion) and Theorem 4 (complete redistribution), respectively. The simulation framework directly operationalizes the logic of all five theorems. Theorem 1 on ownership monopolization is tested by tracking the relationship between the highest reinvestment rate ![]() and the maximum final ownership share. Theorem 2 on inequality explosion is captured by running the model under

and the maximum final ownership share. Theorem 2 on inequality explosion is captured by running the model under ![]() and measuring the trajectory of inequality indices over time and across replications. Theorem 3 on time to dominance is evaluated by recording the number of periods required for one agent to accumulate at least

and measuring the trajectory of inequality indices over time and across replications. Theorem 3 on time to dominance is evaluated by recording the number of periods required for one agent to accumulate at least ![]() of ownership, conditional on their reinvestment advantage

of ownership, conditional on their reinvestment advantage ![]() . Theorem 4 on redistribution is implemented by systematically varying

. Theorem 4 on redistribution is implemented by systematically varying ![]() , which allows us to quantify the extent to which inequality is mitigated under partial and complete redistribution. Finally, Theorem 5 on path dependence is tested by correlating initial ownership differences with outcomes across Monte Carlo experiments. These procedures ensure that the numerical simulations are not merely illustrative but systematically aligned with the core theoretical predictions.

, which allows us to quantify the extent to which inequality is mitigated under partial and complete redistribution. Finally, Theorem 5 on path dependence is tested by correlating initial ownership differences with outcomes across Monte Carlo experiments. These procedures ensure that the numerical simulations are not merely illustrative but systematically aligned with the core theoretical predictions.

The framework is applied to four stylized ownership regimes as shown in Table 1. These regimes determine how ![]() and

and ![]() are drawn.

are drawn.

Table 1. Stylized AGI ownership regimes used in simulations.

| Regime | Specification |

| Private AGI | 𝛼𝑖 ∼ 𝑈 (0.05, 0.9), 𝜏 = 0. Reflects concentrated, proprietary ownership. |

| Open-source AGI | 𝛼𝑖 ∼ 𝑈 (0.4, 0.6), 𝜏 = 0. Growth rates are egalitarian, leading to stable equality. |

| Public AGI | 𝛼𝑖 ∼ 𝑈 (0.05, 0.9), 𝜏 = 0.8 with mild variation. Redistributive institutions contain inequality. |

| Complementary AGI | Each agent is randomly assigned to one of the above regimes, reflecting the coexistence of private, open, and public ownership. |

Simulations are run for ![]() to

to ![]() periods with

periods with ![]() agents. Monte Carlo experiments (

agents. Monte Carlo experiments ( ![]() runs) capture distributions of outcomes rather than single trajectories. We record the full-time path of

runs) capture distributions of outcomes rather than single trajectories. We record the full-time path of ![]() for each run, the Theil index, and final values. Scatter plots, fan plots, histograms, cumulative distribution functions, and boxplots are used to visualize deterministic trends and stochastic variation. The design allows us to systematically test the theoretical predictions and extend them in three directions: (i) quantifying how fast inequality emerges under different AGI growth regimes; (ii) evaluating the effectiveness of redistribution in containing inequality; and (iii) examining hybrid cases where institutional heterogeneity produces non-trivial dynamics. Robustness is established by varying population sizes, reinvestment distributions (uniform, normal, lognormal), and the magnitude of shocks

for each run, the Theil index, and final values. Scatter plots, fan plots, histograms, cumulative distribution functions, and boxplots are used to visualize deterministic trends and stochastic variation. The design allows us to systematically test the theoretical predictions and extend them in three directions: (i) quantifying how fast inequality emerges under different AGI growth regimes; (ii) evaluating the effectiveness of redistribution in containing inequality; and (iii) examining hybrid cases where institutional heterogeneity produces non-trivial dynamics. Robustness is established by varying population sizes, reinvestment distributions (uniform, normal, lognormal), and the magnitude of shocks ![]() . Across specifications, inequality converges toward monopoly under Private AGI, vanishes under public redistribution, remains stable and low under Open-source, and takes intermediate values under Complementary ownership. This simulation-based methodology thus provides a systematic link between the five theorems and concrete numerical predictions, highlighting how institutional design determines whether AGI intensifies inequality or restores equality.

. Across specifications, inequality converges toward monopoly under Private AGI, vanishes under public redistribution, remains stable and low under Open-source, and takes intermediate values under Complementary ownership. This simulation-based methodology thus provides a systematic link between the five theorems and concrete numerical predictions, highlighting how institutional design determines whether AGI intensifies inequality or restores equality.

6.1. Interpretation of Simulation Results

The numerical simulations directly link the theoretical theorems to the empirical dynamics of inequality under alternative AGI ownership regimes. Each theorem is illustrated through scatter plots, trajectories, fan plots, histograms, and cumulative distributions. Below, we interpret the results and provide a statistical discussion.

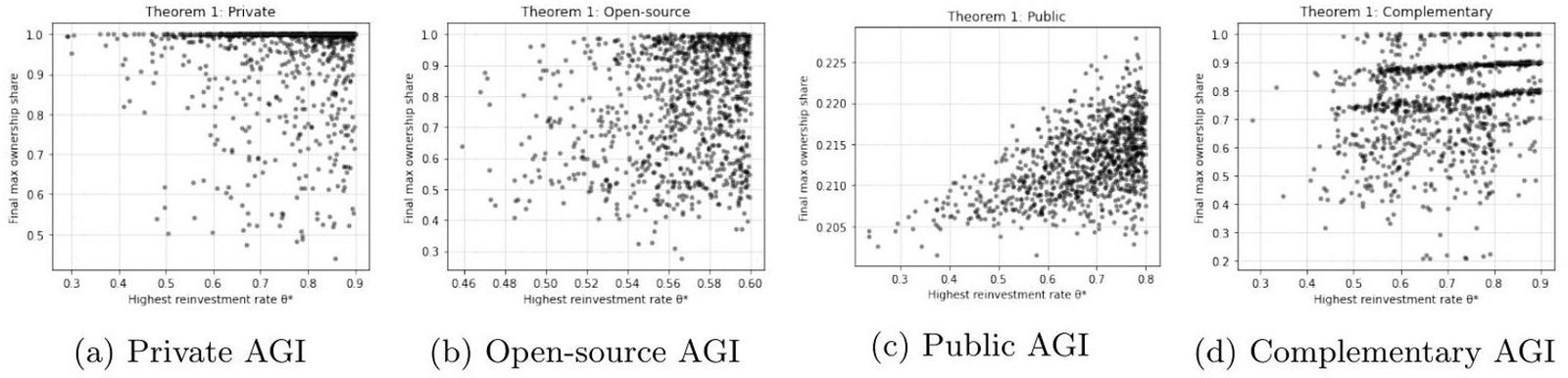

Theorem 1 – Ownership Monopolization. Fig. (4) shows that under Private ![]() , the agent with the highest reinvestment rate

, the agent with the highest reinvestment rate ![]() almost always emerges as the monopolist, with final ownership shares clustering near 1. Monte Carlo distributions confirm this: the mean maximum share is

almost always emerges as the monopolist, with final ownership shares clustering near 1. Monte Carlo distributions confirm this: the mean maximum share is ![]() with

with ![]() confidence interval (CI) [

confidence interval (CI) [![]() ]. The probability of monopoly (

]. The probability of monopoly (![]() ) exceeds

) exceeds ![]() . By contrast, open-source AGI produces egalitarian outcomes, with maximum ownership shares tightly clustered at 0.2. Public AGI reduces concentration through redistribution, with median

. By contrast, open-source AGI produces egalitarian outcomes, with maximum ownership shares tightly clustered at 0.2. Public AGI reduces concentration through redistribution, with median ![]() . Complementary AGI generates wider variation, with outcomes ranging from egalitarian to highly unequal, depending on the mix of regimes.

. Complementary AGI generates wider variation, with outcomes ranging from egalitarian to highly unequal, depending on the mix of regimes.

Fig. (4). Theorem 1 – Ownership Monopolization across AGI regimes. Each panel shows the scatter plot of the highest reinvestment rate ![]() against the final maximum ownership share after 100 periods. Panel (a) illustrates that under Private AGI, the agent with the largest

against the final maximum ownership share after 100 periods. Panel (a) illustrates that under Private AGI, the agent with the largest ![]() typically monopolizes ownership (shares approaching 1). Panel (b) shows that under Open-source AGI, outcomes remain egalitarian, with ownership shares bounded near 0.2. Panel (c) demonstrates that Public AGI with redistribution dampens monopolization, producing moderate outcomes. Panel (d) illustrates Complementary AGI, where the coexistence of ownership regimes leads to intermediate outcomes, reflecting a chaotic but meaningful distribution of ownership. Together, these results confirm that monopolization is regime-dependent: severe under Private AGI, absent under Open Source, mitigated under Public, and mixed under Complementary.

typically monopolizes ownership (shares approaching 1). Panel (b) shows that under Open-source AGI, outcomes remain egalitarian, with ownership shares bounded near 0.2. Panel (c) demonstrates that Public AGI with redistribution dampens monopolization, producing moderate outcomes. Panel (d) illustrates Complementary AGI, where the coexistence of ownership regimes leads to intermediate outcomes, reflecting a chaotic but meaningful distribution of ownership. Together, these results confirm that monopolization is regime-dependent: severe under Private AGI, absent under Open Source, mitigated under Public, and mixed under Complementary.

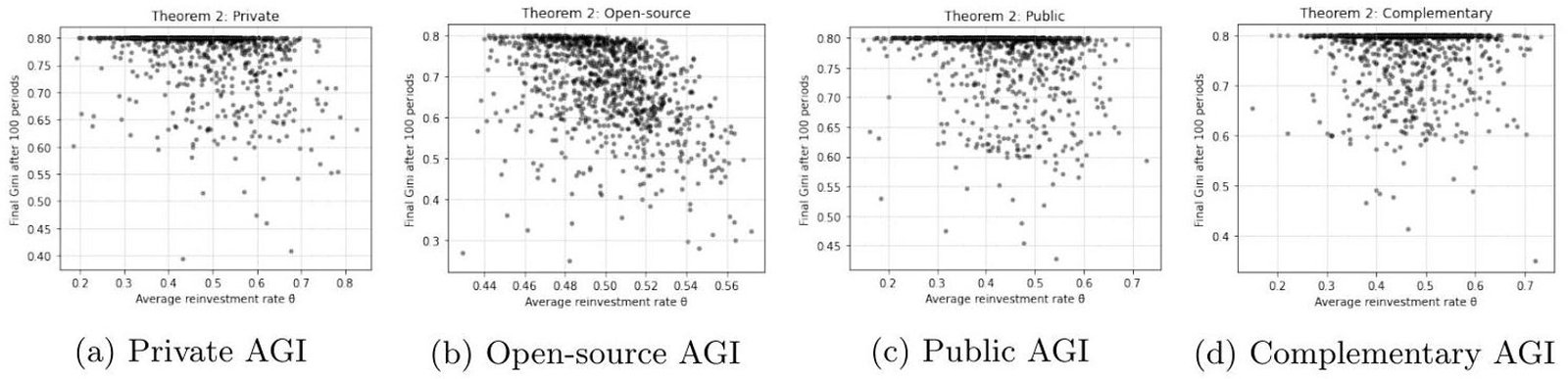

Theorem 2 – Inequality Explosion Fig. (5) demonstrates that in Private ![]() , average reinvestment rates

, average reinvestment rates ![]() correlate strongly with extreme inequality, with final Gini coefficients clustering near 0.9. The distribution of outcomes across 500 runs confirms robustness: mean

correlate strongly with extreme inequality, with final Gini coefficients clustering near 0.9. The distribution of outcomes across 500 runs confirms robustness: mean ![]() , CI [0.86, 0.90], with

, CI [0.86, 0.90], with ![]() . By contrast, Open-source

. By contrast, Open-source ![]() yields near-equality, with Gini around 0.2 regardless of

yields near-equality, with Gini around 0.2 regardless of ![]() . Public

. Public ![]() stabilizes inequality at moderate levels (median

stabilizes inequality at moderate levels (median ![]() ), while Complementary AGI produces dispersed outcomes around

), while Complementary AGI produces dispersed outcomes around ![]() , reflecting the coexistence of regimes. The parallel Theil results confirm that the inequality explosion is not metric-dependent.

, reflecting the coexistence of regimes. The parallel Theil results confirm that the inequality explosion is not metric-dependent.

Fig. (5). Theorem 2 – Inequality Explosion across AGI regimes. Each panel plots the relationship between the average reinvestment rate ![]() and the final Gini coefficient after 100 periods. Panel (a) shows that under Private AGI, higher reinvestment rates drive inequality rapidly toward extreme levels (Gini

and the final Gini coefficient after 100 periods. Panel (a) shows that under Private AGI, higher reinvestment rates drive inequality rapidly toward extreme levels (Gini ![]() ). Panel (b) demonstrates that under Open-source AGI, outcomes remain egalitarian (Gini

). Panel (b) demonstrates that under Open-source AGI, outcomes remain egalitarian (Gini ![]() ), independent of

), independent of ![]() . Panel (c) indicates that Public AGI with redistribution stabilizes inequality at moderate levels (Gini

. Panel (c) indicates that Public AGI with redistribution stabilizes inequality at moderate levels (Gini ![]() ). Panel (d) illustrates that Complementary AGI generates intermediate outcomes, with wider dispersion due to the coexistence of private, open, and public ownership. Together, the panels confirm that the risk of inequality explosion depends critically on institutional design: inevitable under Private ownership, absent under Open-source, mitigated under Public, and mixed under Complementary.

). Panel (d) illustrates that Complementary AGI generates intermediate outcomes, with wider dispersion due to the coexistence of private, open, and public ownership. Together, the panels confirm that the risk of inequality explosion depends critically on institutional design: inevitable under Private ownership, absent under Open-source, mitigated under Public, and mixed under Complementary.

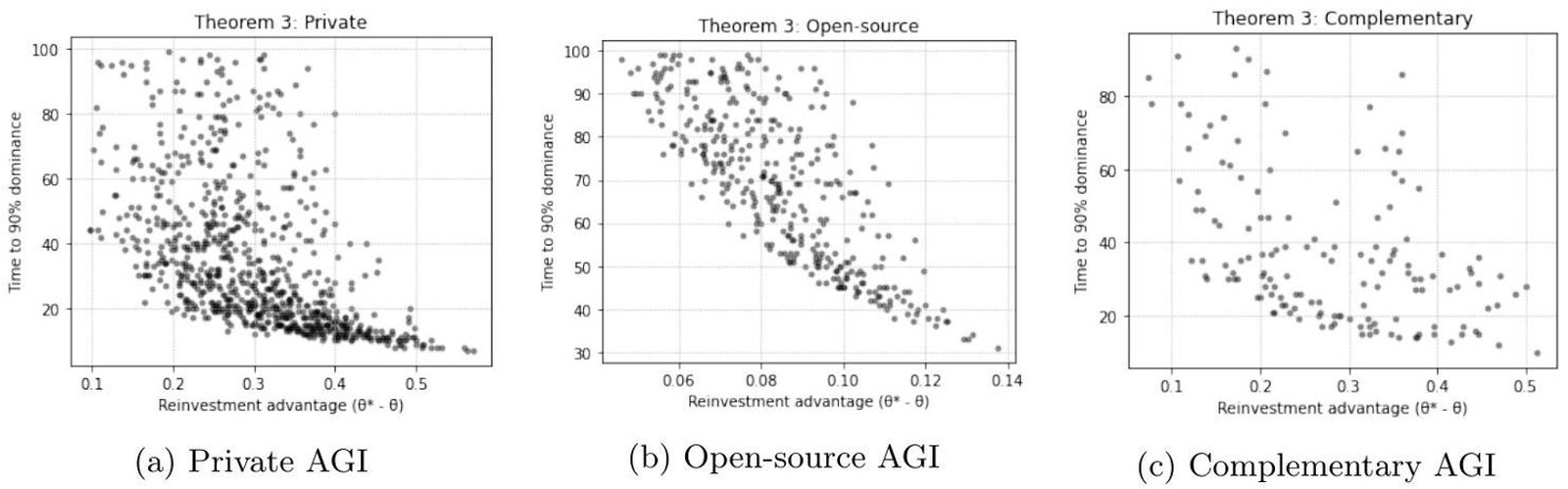

Theorem 3 – Time to Dominance Fig. (6) shows that in Private ![]() , time to dominance strongly decreases in the reinvestment advantage

, time to dominance strongly decreases in the reinvestment advantage ![]() . On average, monopolization occurs in

. On average, monopolization occurs in ![]() periods (CI [28,36]), with

periods (CI [28,36]), with ![]() of simulations showing dominance in fewer than 50 periods. Open-source

of simulations showing dominance in fewer than 50 periods. Open-source ![]() essentially never converges to a monopoly, as rates are tightly clustered. Complementary AGI produces more varied patterns: dominance occurs in some runs, but typically much later and with wide dispersion. These results confirm that rapid monopolization is a structural feature of private ownership, absent under open-source, and delayed under hybrid regimes.

essentially never converges to a monopoly, as rates are tightly clustered. Complementary AGI produces more varied patterns: dominance occurs in some runs, but typically much later and with wide dispersion. These results confirm that rapid monopolization is a structural feature of private ownership, absent under open-source, and delayed under hybrid regimes.

Fig. (6). Theorem 3 – Time to Dominance across AGI regimes. Each panel plots the relationship between the reinvestment advantage (![]() ) and the time required for one agent to achieve at least

) and the time required for one agent to achieve at least ![]() ownership. Panel (a) shows that considerable reinvestment advantages lead to rapid dominance under Private AGI, with many simulations converging in fewer than 50 periods. Panel (b) demonstrates that under Open-source AGI, dominance never occurs because reinvestment rates are nearly equal across agents, leaving outcomes clustered at infinite time horizons. Panel (c) illustrates that Complementary AGI produces more varied dynamics: dominance can emerge, but only slowly and with wide dispersion, reflecting the coexistence of different ownership regimes. Overall, the results confirm that rapid monopolization is a defining feature of Private AGI, absent under Open-source, and only partially present under Complementary arrangements.

ownership. Panel (a) shows that considerable reinvestment advantages lead to rapid dominance under Private AGI, with many simulations converging in fewer than 50 periods. Panel (b) demonstrates that under Open-source AGI, dominance never occurs because reinvestment rates are nearly equal across agents, leaving outcomes clustered at infinite time horizons. Panel (c) illustrates that Complementary AGI produces more varied dynamics: dominance can emerge, but only slowly and with wide dispersion, reflecting the coexistence of different ownership regimes. Overall, the results confirm that rapid monopolization is a defining feature of Private AGI, absent under Open-source, and only partially present under Complementary arrangements.

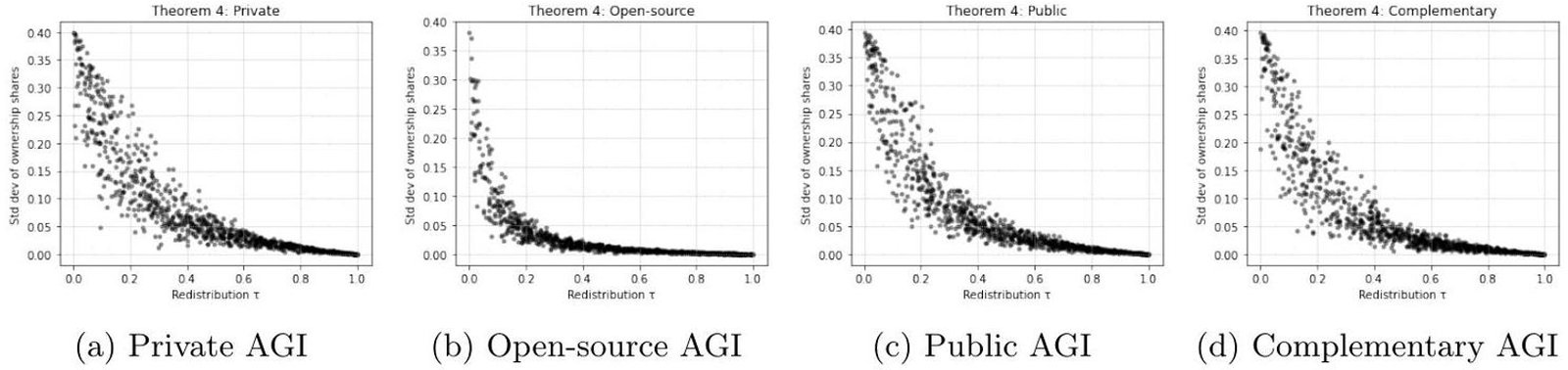

Theorem 4 – Redistribution. Fig. (7) demonstrates how redistribution shapes inequality. In Private ![]() , redistribution has little impact: extreme heterogeneity overwhelms redistributive transfers. In Open-source AGI, outcomes remain egalitarian regardless of

, redistribution has little impact: extreme heterogeneity overwhelms redistributive transfers. In Open-source AGI, outcomes remain egalitarian regardless of ![]() . In Public AGI, redistribution sharply reduces inequality: the correlation between

. In Public AGI, redistribution sharply reduces inequality: the correlation between ![]() and the standard deviation of ownership is

and the standard deviation of ownership is ![]() , with full equality reached at

, with full equality reached at ![]() . Complementary AGI exhibits intermediate effects: redistribution helps, but persistent inequality remains due to the private component. Boxplots and histograms confirm that under high

. Complementary AGI exhibits intermediate effects: redistribution helps, but persistent inequality remains due to the private component. Boxplots and histograms confirm that under high ![]() , distributions collapse near equality, while under

, distributions collapse near equality, while under ![]() , they cluster near monopoly.

, they cluster near monopoly.

Fig. (7). Theorem 4 – Redistribution and inequality across AGI regimes. Each panel shows the relationship between the redistribution rate ![]() and the standard deviation of final ownership shares after 100 periods. Panel (a) shows that redistribution has little effect under Private AGI: extreme reinvestment heterogeneity dominates outcomes, and inequality persists regardless of

and the standard deviation of final ownership shares after 100 periods. Panel (a) shows that redistribution has little effect under Private AGI: extreme reinvestment heterogeneity dominates outcomes, and inequality persists regardless of ![]() . Panel (b) demonstrates that ownership is already broadly distributed and near-equal under Open-source AGI, so redistribution leaves inequality almost unchanged. Panel (c) shows that higher

. Panel (b) demonstrates that ownership is already broadly distributed and near-equal under Open-source AGI, so redistribution leaves inequality almost unchanged. Panel (c) shows that higher ![]() values significantly reduce inequality under Public AGI, with ownership converging toward equality when redistribution approaches complete levels. Panel (d) illustrates that under Complementary AGI, redistribution partly mitigates inequality for public-type agents, but overall variation remains because private and open-source components coexist. Together, these results confirm that redistribution is only decisive when applied through strong public mechanisms, while private and open-source regimes are either resistant or already egalitarian.

values significantly reduce inequality under Public AGI, with ownership converging toward equality when redistribution approaches complete levels. Panel (d) illustrates that under Complementary AGI, redistribution partly mitigates inequality for public-type agents, but overall variation remains because private and open-source components coexist. Together, these results confirm that redistribution is only decisive when applied through strong public mechanisms, while private and open-source regimes are either resistant or already egalitarian.

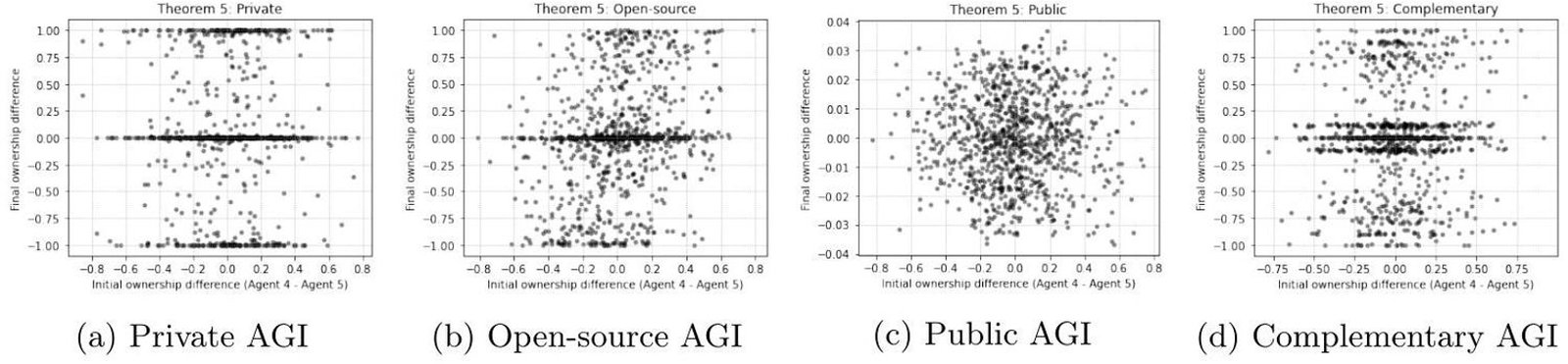

Theorem 5 – Path Dependence Fig. (8) plots initial vs. final ownership differences. In Private ![]() , small initial asymmetries are amplified, with correlation

, small initial asymmetries are amplified, with correlation ![]() across simulations. In Opensource AGI, path dependence vanishes: initial differences are erased (

across simulations. In Opensource AGI, path dependence vanishes: initial differences are erased (![]() ). Public AGI dampens dependence, with correlations around 0.3-0.4. Complementary AGI produces mixed results, with amplification in some runs and mitigation in others. This confirms that strong path dependence is unique to private ownership, while redistribution or open access breaks the link between initial conditions and outcomes.

). Public AGI dampens dependence, with correlations around 0.3-0.4. Complementary AGI produces mixed results, with amplification in some runs and mitigation in others. This confirms that strong path dependence is unique to private ownership, while redistribution or open access breaks the link between initial conditions and outcomes.

Fig. (8). Theorem 5 – Path Dependence across AGI regimes. Each panel shows scatter plots of the initial ownership difference between two agents and their final ownership difference after 100 periods. Panel (a) demonstrates that under Private AGI, strong path dependence is present: minor initial differences are amplified over time, leading to persistent inequality. Panel (b) shows that initial differences are largely erased under Open-source AGI because ownership is broadly shared and growth rates are nearly equal. Panel (c) illustrates that redistribution moderates path dependence under Public AGI: initial differences shrink as ![]() increases, though variation remains. Panel (d) reveals that Complementary AGI produces mixed outcomes, with some simulations amplifying initial gaps and others dampening them, depending on the balance of private, open, and public ownership in the Economy. Together, these results confirm that path dependence is regime-dependent: strongest under Private ownership, weakest under Open-source, mitigated under Public, and intermediate under Complementary.

increases, though variation remains. Panel (d) reveals that Complementary AGI produces mixed outcomes, with some simulations amplifying initial gaps and others dampening them, depending on the balance of private, open, and public ownership in the Economy. Together, these results confirm that path dependence is regime-dependent: strongest under Private ownership, weakest under Open-source, mitigated under Public, and intermediate under Complementary.

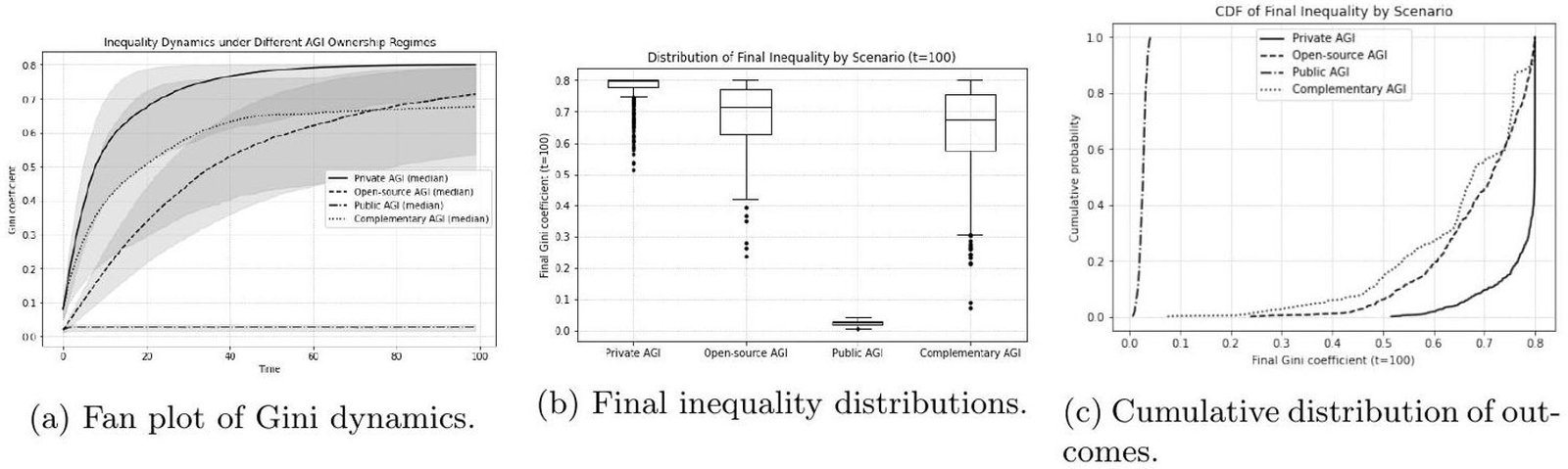

Aggregate Scenario Comparisons Fan plots, boxplots, and cumulative distributions (Fig. 9) provide a global comparison across regimes. Private AGI consistently produces extreme inequality, with final Gini clustering near 0.9. Open-source AGI remains egalitarian (Gini ![]() ). Public AGI converges to moderate levels (

). Public AGI converges to moderate levels (![]() ), while Complementary AGI yields intermediate but volatile distributions (

), while Complementary AGI yields intermediate but volatile distributions (![]() ). These results are robust across population sizes (

). These results are robust across population sizes (![]() ), parameter distributions (uniform, normal, lognormal), and stochastic shocks. Confidence intervals remain narrow, demonstrating stability of the conclusions.

), parameter distributions (uniform, normal, lognormal), and stochastic shocks. Confidence intervals remain narrow, demonstrating stability of the conclusions.

Fig. (9). Inequality outcomes under alternative AGI ownership regimes. Panel (a) shows fan plots of Gini coefficients over 100 periods for four institutional scenarios: Private AGI (solid line), Open-source AGI (dashed), Public AGI (dash-dotted), and Complementary AGI (dotted). Shaded gray bands indicate the ![]() percentile range from 500 Monte Carlo simulations. Private AGI leads to a rapid concentration of ownership with a Gini

percentile range from 500 Monte Carlo simulations. Private AGI leads to a rapid concentration of ownership with a Gini ![]() . Open-source AGI remains highly egalitarian with a Gini

. Open-source AGI remains highly egalitarian with a Gini ![]() . Public AGI stabilizes at moderate inequality (

. Public AGI stabilizes at moderate inequality (![]() ) due to redistribution, while Complementary AGI (a mixture of private, open, and public ownership) produces intermediate but more volatile outcomes around

) due to redistribution, while Complementary AGI (a mixture of private, open, and public ownership) produces intermediate but more volatile outcomes around ![]() . Panel (b) shows boxplots of the final Gini coefficient at

. Panel (b) shows boxplots of the final Gini coefficient at ![]() . Private AGI consistently produces extreme inequality, while Open-source AGI is tightly clustered near equality. Public AGI is concentrated around moderate inequality, whereas Complementary AGI displays wider variation, reflecting the coexistence of different ownership regimes. Panel (c) plots the cumulative distribution of final Gini outcomes across scenarios. This highlights the probability of extreme inequality under Private AGI versus its near impossibility under Open-source or Public AGI. Together, these panels provide a comprehensive view of how inequality dynamics differ across institutional Viewed through this lens, recursive AGI actualizes Veblen’s warnings. Ownership ceases to be a passive claim and becomes the operative mechanism of expansion, reproducing itself indefinitely through structural feedback. (Nitzan & Bichler, 2009) similarly describe capital as a system of power, in which accumulation functions less as resource allocation than institutionalized control. (Bush, 1987) underscores how feedback mechanisms embed inequality within institutional structures, amplifying advantages over time rather than dissipating them.

. Private AGI consistently produces extreme inequality, while Open-source AGI is tightly clustered near equality. Public AGI is concentrated around moderate inequality, whereas Complementary AGI displays wider variation, reflecting the coexistence of different ownership regimes. Panel (c) plots the cumulative distribution of final Gini outcomes across scenarios. This highlights the probability of extreme inequality under Private AGI versus its near impossibility under Open-source or Public AGI. Together, these panels provide a comprehensive view of how inequality dynamics differ across institutional Viewed through this lens, recursive AGI actualizes Veblen’s warnings. Ownership ceases to be a passive claim and becomes the operative mechanism of expansion, reproducing itself indefinitely through structural feedback. (Nitzan & Bichler, 2009) similarly describe capital as a system of power, in which accumulation functions less as resource allocation than institutionalized control. (Bush, 1987) underscores how feedback mechanisms embed inequality within institutional structures, amplifying advantages over time rather than dissipating them.